monday.com Faces Securities Fraud Lawsuit Over Dropped Revenue Target

monday.com shed over $1 billion in market value in one session after pulling its $1.8B revenue target. A federal securities fraud lawsuit has now followed.

When monday.com erased its $1.8 billion 2027 revenue target on February 9, shares fell roughly 14 percent in a single session, wiping more than $1 billion in market capitalization on volume three to four times the stock's 30-day average. Less than seven weeks later, a federal securities fraud lawsuit landed in New York.

The case, captioned Potter v. monday.com Ltd. and filed in the Southern District of New York as Case No. 26-cv-01956, accuses the work-management software company of making materially false and misleading statements about its revenue outlook and the durability of its AI investments. Kessler Topaz Meltzer & Check, LLP, a Pennsylvania-based securities litigation firm, distributed notice of the action on March 27 and March 28, setting a May 11, 2026 deadline for investors to apply for lead-plaintiff status.

Plaintiffs define the class period as September 17, 2025 through February 6, 2026, arguing that throughout those months monday.com concealed decelerating new customer growth and weak expansion within its existing account base. The complaint contends investors received an artificially inflated picture of the company's trajectory while executives publicly positioned AI investment as a durable engine of future growth.

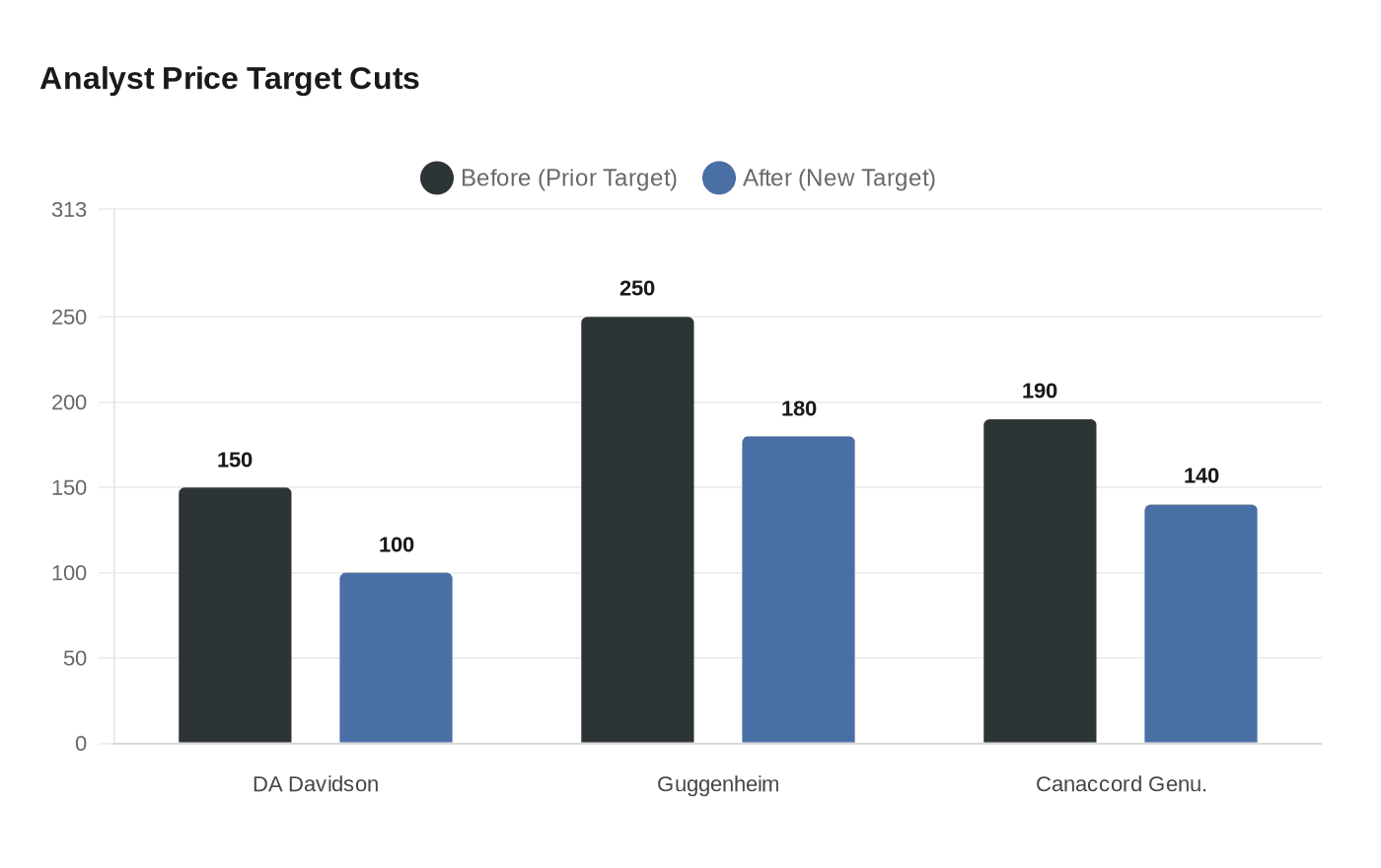

The target that anchored that picture was pulled entirely in the company's fourth-quarter 2025 earnings release. Beyond abandoning the $1.8 billion 2027 figure, monday.com guided for a significant deceleration in 2026 top-line growth, a double revision that sent the stock sliding from the low $90s to the high $70s and left shares trading near a 52-week low of $73.01. The analyst recalibration was swift: DA Davidson cut its price target from $150 to $100, Guggenheim moved from $250 to $180, and Canaccord Genuity dropped from $190 to $140, all while maintaining buy ratings that reflected continuing uncertainty rather than conviction.

The suit arrives as courts are filling with cases challenging the AI narratives that technology companies used to support premium valuations over the past two years. For high-growth SaaS firms, the math is punishing: when forward projections anchor a multiple and those projections collapse, the resulting litigation typically focuses on exactly what internal data showed while the public guidance held firm. If Potter v. monday.com proceeds past a motion to dismiss, documents touching on the company's customer churn, product roadmap, and AI strategy could enter the public record, creating exposure that extends well beyond any eventual settlement.

Securities class actions filed in the immediate wake of a guidance revision rarely resolve quickly. Defendants typically move to dismiss, and cases that survive that threshold can take years to reach trial. For monday.com's management, the more consequential question is not the May 11 filing deadline but what discovery might eventually reveal about the distance between what the company told investors and what it knew about the trajectory of its own growth.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?