Monday.com Q4 Results and Soft 2026 Guidance Spark 14% Selloff

Monday.com shares fell about 14% to roughly $85 after hours as management gave softer 2026 guidance despite $1.232B in 2025 revenue and rapid AI traction.

Shares of Monday.com plunged in the wake of its Q4 and full-year 2025 report, tumbling roughly 14% to about $85 in after-hours trading after management issued softer guidance for 2026 and flagged margin headwinds. Investors reacted to a contrast: solid full-year results paired with a conservative tone on the year ahead.

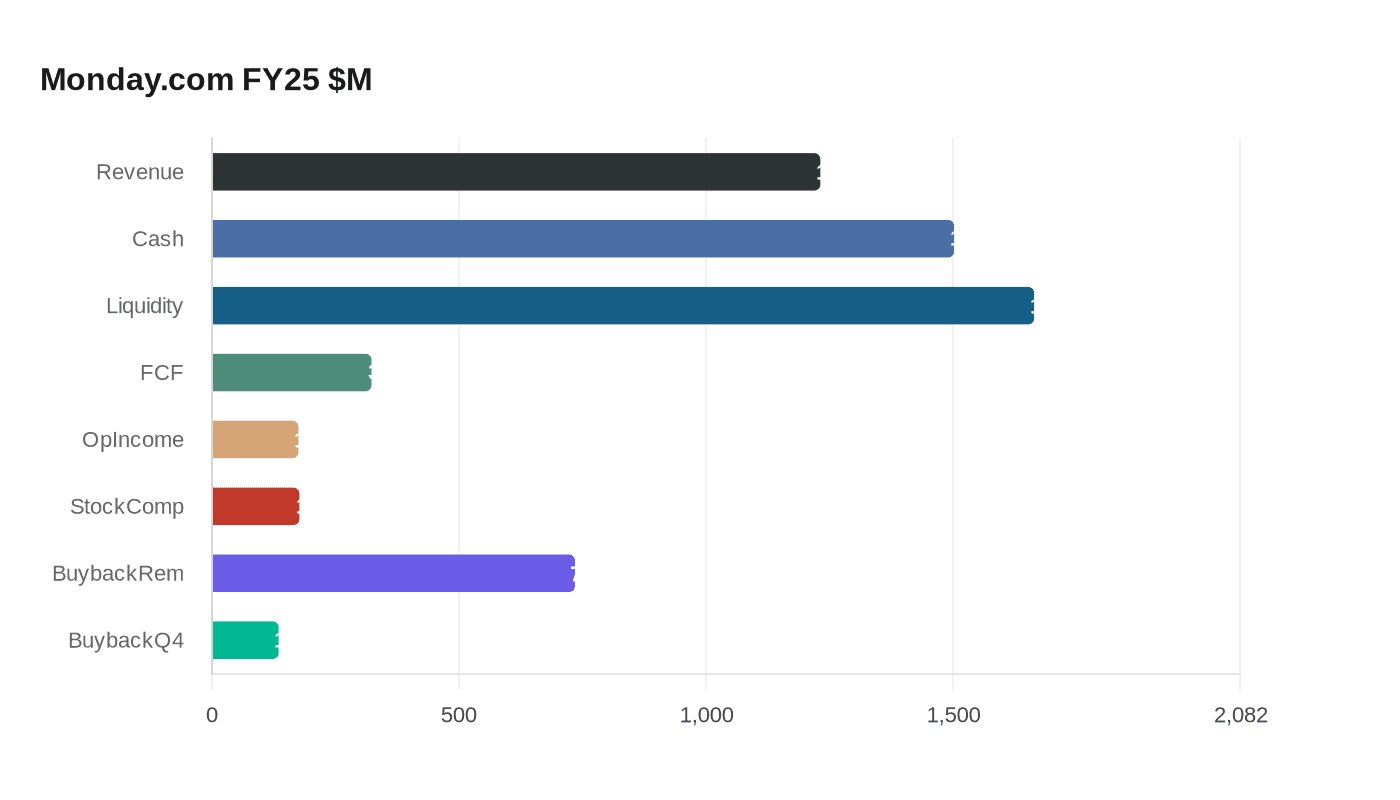

The company posted FY2025 revenue of $1.232 billion, up 27% year over year, with non-GAAP operating income of $175 million and an operating margin of about 14%, essentially flat versus the prior year. Free cash flow was $323 million, a 26% FCF margin, and stock-based compensation totaled $177 million. Net dollar retention for the company was 110%, two percentage points lower than a year earlier.

Operationally Monday.com highlighted clear upmarket momentum. Forty-one percent of revenue now comes from customers with ARR above $50,000, up from 36% a year ago, and the company said large-customer NRR was 116%. Customers with ARR above $100,000 grew by 45% to more than 1,750, and remaining performance obligations rose 37% to $839 million. At the same time management acknowledged persistent weakness in self-serve SMBs; Co-CEO Roy Mann said, “the cost to acquire and expand self-serve customers have increased over the past year, and the returns on those investments have been below historical levels.”

AI product adoption was a central part of the narrative. Management noted rapid traction for products such as monday Vibe and Sidekick, with Vibe described as the fastest product in company history to reach $1 million ARR. Co-CEO Eran Zinman argued the advantage for customers is “the value of deep workflow integration, platform security, and enterprise-grade capabilities.” Analysts including Arjun Bhatia, Scott Berg, Ryan McWilliams, Mark Murphy and D.J. Hynes pressed management on the sustainability of growth, margin compression and Vibe’s competitive positioning. CFO Eliran Glazer attributed margin pressure to FX headwinds, increased investment in sales-led growth and AI, and front-loaded costs that take longer to yield returns.

The market response also reflected a valuation reset. Simply Wall St cited a P/E of 33.4x versus a U.S. software industry average of 25.8x, while a revenue-multiple read by other analysts put Monday.com at about 6x forward revenue at the roughly $85 level versus about 7x pre-earnings. The stock has lost about three quarters of its value over the past year from a 52-week high of $342.64, with a 30-day return down 39.23% and a one-year total shareholder return down 75.02%.

Capital allocation adds a subplot. The company repurchased roughly 884,000 shares in Q4 at an average price near $153, spending about $135 million, and ended the quarter with cash and equivalents of $1,503 million and total liquidity of $1,665 million, leaving $735 million of buyback authorization. With enterprise retention and AI adoption cited as the bull case and SMB recovery and FX exposure raised as the bear case, the next quarters will determine whether Monday.com’s upmarket shift sustains revenue growth or signals a longer term normalization.

Know something we missed? Have a correction or additional information?

Submit a Tip