Mortgage rates ease slightly, but July relief may be limited

The 30-year mortgage rate slipped to 6.47%, but the Fed’s June hold and economists’ forecasts point to only modest July relief for buyers and refinancers.

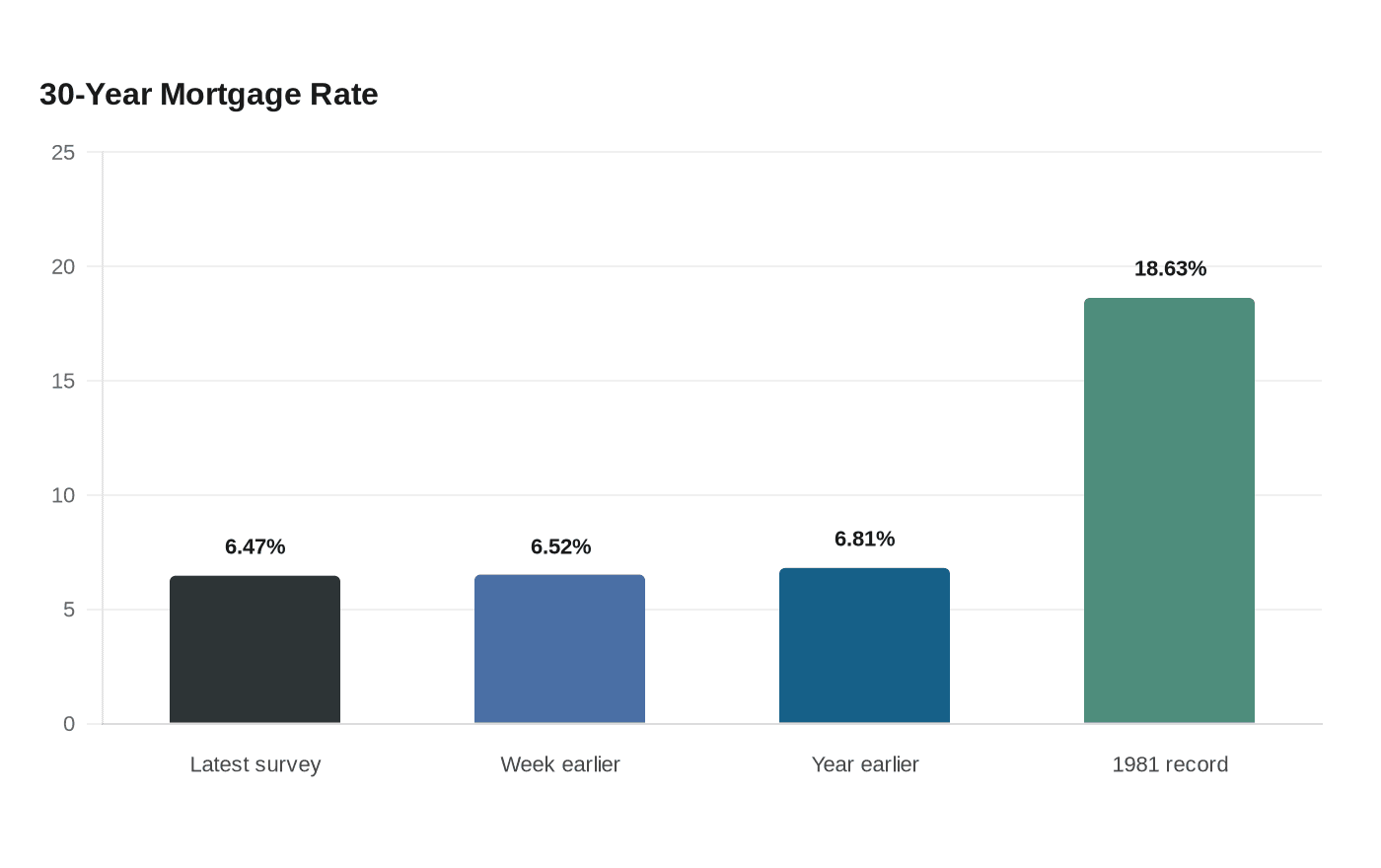

The average 30-year mortgage rate fell to 6.47% in Freddie Mac’s latest survey, but the drop from 6.52% a week earlier is too small to promise meaningful July relief. The Federal Reserve kept its benchmark rate at 3.5% to 3.75% at its June 16-17 meeting, leaving homeowners to watch bond yields, inflation data and their own credit profiles instead of betting on a quick policy pivot.

Freddie Mac’s Primary Mortgage Market Survey is based on thousands of loan applications from lenders nationwide and is released every Thursday at noon ET. The 15-year fixed rate also eased, to 5.81% from 5.84% the prior week. Even with the recent easing, the 30-year mortgage remains well above the 6.81% average from a year earlier, though still far below the 18.63% record high reached in 1981.

The bigger question for households is not whether rates moved a few basis points this week, but whether the broader market has enough momentum to push them much lower in July. Mortgage rates tend to follow bond markets and expectations for future Fed policy more closely than the federal funds rate itself, and the Fed’s June projections showed policymakers still focused on inflation, GDP growth and unemployment before making another move. A June poll of economists pointed to a Fed hold for the rest of 2026, while property specialists expected high mortgage rates to keep housing turnover subdued.

Lawrence Yun, chief economist at the National Association of Realtors, said rates in 2026 were likely to stay in the 6.5% to 6.7% range, not drift down to 6% as he had earlier expected. Freddie Mac chief economist Sam Khater pointed to resilient retail sales and a firmer reading on pending home sales as signs that purchase demand was improving, but only modestly.

That leaves borrowers with a practical decision rather than a market fantasy. A household with a closing date in hand or a refinance that already cuts monthly costs has more reason to lock than to gamble on a small July decline. Buyers with strong credit, a solid down payment and room to wait can keep an eye on inflation and Treasury yields, but the recent pattern suggests any relief is more likely to come in inches than in points. The Mortgage Bankers Association said applications jumped 10.8% in the week ending June 5 after a holiday adjustment, then rose another 1.0% in the week ending June 19, with refinances up 3% and purchases down 1%, a sign that demand is still sensitive to even minor rate moves.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip