Mortgage rates hold near 6.5% as spring homebuying season heats up

Mortgage rates hovered near 6.5%, but a tiny rate move still changes monthly payments by tens of dollars on typical home loans.

A small move in mortgage rates still changes the monthly bill in a meaningful way. At a 6.51% 30-year fixed purchase rate, a $300,000 loan costs about $1,898 a month in principal and interest, roughly $28 more than at 6.37%, and a $500,000 loan costs about $3,164, about $46 more.

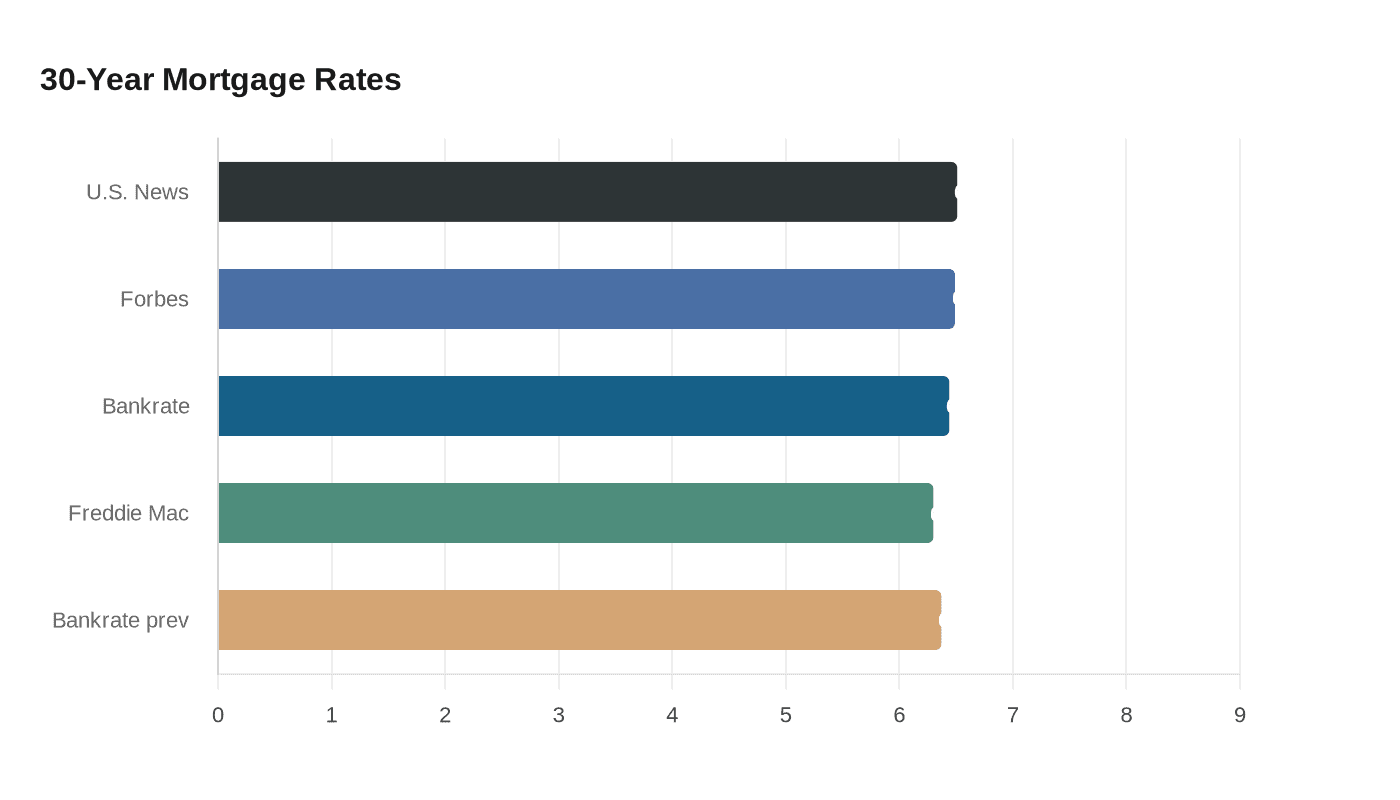

That is the affordability test confronting buyers as the spring homebuying season picks up. U.S. News put the average 30-year fixed purchase mortgage at 6.51% on May 6. Forbes Advisor had it at 6.49%, up from 6.37% a week earlier. Bankrate showed 6.44% for a current average 30-year fixed mortgage and 6.65% for a 30-year fixed refinance, while NerdWallet listed a 30-year fixed APR of 6.34% and a 15-year fixed APR of 5.79% as of 10:20 a.m. EDT.

Refinancers are seeing only limited relief. On a $350,000 balance, a 30-year fixed refinance at 6.65% works out to about $2,247 a month, compared with about $2,199 at 6.44%. Even Forbes Advisor’s 6.55% refinance rate still implies a payment near $2,224 on that same balance. The difference is not dramatic from one quote to the next, but it is enough to affect whether a monthly budget clears underwriting or gets squeezed by taxes, insurance and other housing costs.

The wider picture is a mortgage market that has settled into a narrow range rather than breaking lower. Freddie Mac’s weekly survey, based on thousands of loan applications submitted through Loan Product Advisor, showed 6.30% in its latest reading available by May 1. The Federal Reserve Bank of St. Louis’ FRED series tracked the 30-year fixed average through April 30. Bankrate said its national 30-year average had risen to 6.37% the prior week.

For now, the odds favor stability more than a sharp move. NerdWallet’s May outlook said rates should remain relatively steady unless there are major negative developments in Iran, a reminder that geopolitical shocks can still spill into borrowing costs. For buyers, the main story is not a daily tick up or down, but how quickly even modest shifts in rates alter what homes cost in real monthly dollars.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?