New business applications surge, experts share startup tips for entrepreneurs

New business applications are still above 5 million a year, but survival depends on sober first-year choices, not startup enthusiasm alone.

The startup boom is real, but so are the failure points

The number of people filing to start businesses has stayed strikingly high, with the U.S. Chamber of Commerce saying more than 5 million new business applications are filed each year. That surge is proof of ambition, not proof of durability. For anyone thinking about entrepreneurship, the first-year challenge is not simply launching fast, but avoiding the mistakes that drain cash, invite tax trouble, and leave promising ideas without a market.

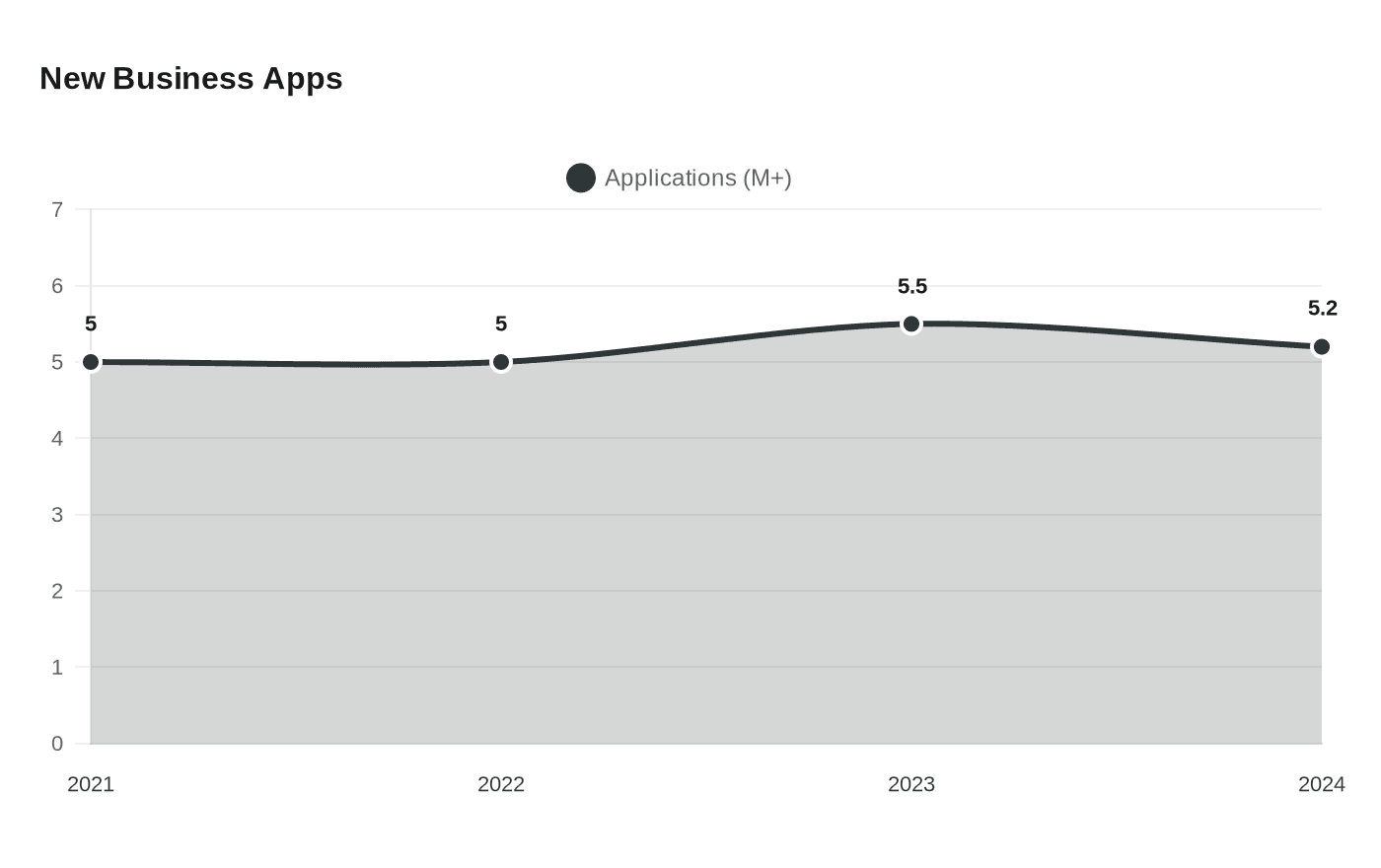

The Chamber says the pace accelerated sharply after the pandemic shock. Applications doubled in 2020 compared with recent years, 2021 and 2022 each topped 5 million, 2023 set a record with 5.5 million new business applications, and 2024 still totaled 5.2 million. Those figures underscore the central reality for new founders: starting a business has become easier to attempt, but survival still depends on disciplined decisions that happen long before the first year ends.

Validate demand before you scale the dream

One of the most common startup failures is building around hope instead of demand. The U.S. Small Business Administration recommends using market research and competitive analysis early in the planning process, because a business idea only matters if customers will pay for it at a price that works. That means testing the size of the market, identifying direct competitors, and figuring out whether your product solves a problem people already care enough about to buy.

The Census Bureau’s Business Formation Statistics are designed to show this kind of entrepreneurial activity in real time, describing the series as high-frequency information on new business applications and formations. The data help show how quickly people enter the market, but they do not reveal who will stay profitable. That gap is where new founders need to be most careful: a wave of applications can signal opportunity, but it can also mask crowded categories and thin margins.

Preserve cash flow from day one

A first-year business can fail even with healthy sales if cash runs out. That is why the SBA’s launch guidance begins with practical setup steps, including opening a business bank account. Separating business and personal money is not just tidy bookkeeping; it helps track runway, measure true operating costs, and avoid using personal funds to cover recurring gaps without a clear plan.

Business insurance is another early expense that is easy to postpone and expensive to ignore. The SBA recommends getting business insurance because a single accident, lawsuit, or property loss can wipe out a young company that has not built reserves. The cash lesson is simple: every early dollar should be assigned a job, whether that is inventory, software, payroll, rent, insurance, or savings for taxes.

Choose the structure that fits the risk

The SBA says one of the first decisions is choosing a business structure because it affects taxes, personal liability, and paperwork. That choice shapes how profits are reported, how much administrative burden falls on the owner, and how exposed personal assets may be if the business runs into legal trouble. In other words, structure is not a formality, it is a financial design decision.

Most businesses also need a tax ID number, licenses and permits, and a registered business structure before they can operate. Skipping those steps can create delays, penalty risk, or costly retrofits later. For first-year founders, the best move is to treat registration and compliance as part of launch strategy, not as paperwork to handle after the business begins making money.

Price for profit, not just for attention

Pricing is often where first-time founders make their biggest mistake. Too many new businesses copy competitors, undercut the market, or set prices based on what feels easy to sell rather than on what the business must earn to survive. A better approach is to work backward from expenses, including insurance, taxes, banking fees, software, labor, and the cost of getting customers in the door.

That matters because the early months rarely resemble a smooth revenue line. Even with strong interest, sales can be uneven, and low prices can lock a business into a volume chase it cannot support. Healthy pricing should leave room for reinvestment, tax obligations, and a cushion for slow months, especially in the first year when every surprise lands harder.

Plan for taxes and benefits before the first paycheck

New founders often underestimate how quickly taxes become a live issue. The SBA’s emphasis on choosing a structure early reflects that reality, because the tax treatment of a business can differ dramatically depending on how it is organized. A business bank account, a tax ID number, and clean records all make it easier to separate income from personal spending and to prepare for filings without scrambling.

Benefits are another first-year pressure point that can strain a small operation. Founders who plan to hire, even on a limited basis, need to think about payroll costs, withholding, and the broader expense of keeping workers attached to the business. Even sole operators should plan as if tax bills and future coverage needs will arrive on time, because they usually do.

Why the data matter for would-be founders

The broader economic signal here is straightforward: entrepreneurship remains active at scale, but the challenge has shifted from creation to endurance. The Census Bureau’s county-level Annual Business Applications data for 2005 through 2024, released on June 11, 2025, give policymakers and analysts a longer view of where startups are forming and how patterns have evolved. The Chamber’s 2024 total of 5.2 million applications shows that the post-pandemic wave has not disappeared, even after the record 2023 peak.

That context makes Jill Schlesinger’s role especially relevant. Schlesinger, CBS News’ Emmy-nominated business analyst and a certified financial planner, is known for her work on the Jill on Money podcast and radio show, and her advice fits the moment: optimism is useful, but only if it is paired with budgeting, pricing discipline, and a hard look at demand. Starting a business may be more common than ever; turning it into a durable enterprise still requires first-year choices that protect cash, lower risk, and build toward profit.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?