NS&I Faces Hundreds of Millions in Compensation for 37,000 Affected Customers

NS&I faces hundreds of millions in compensation payouts to 37,000 customers after bereaved families were denied savings, lost investments, and received letters addressed to dead relatives.

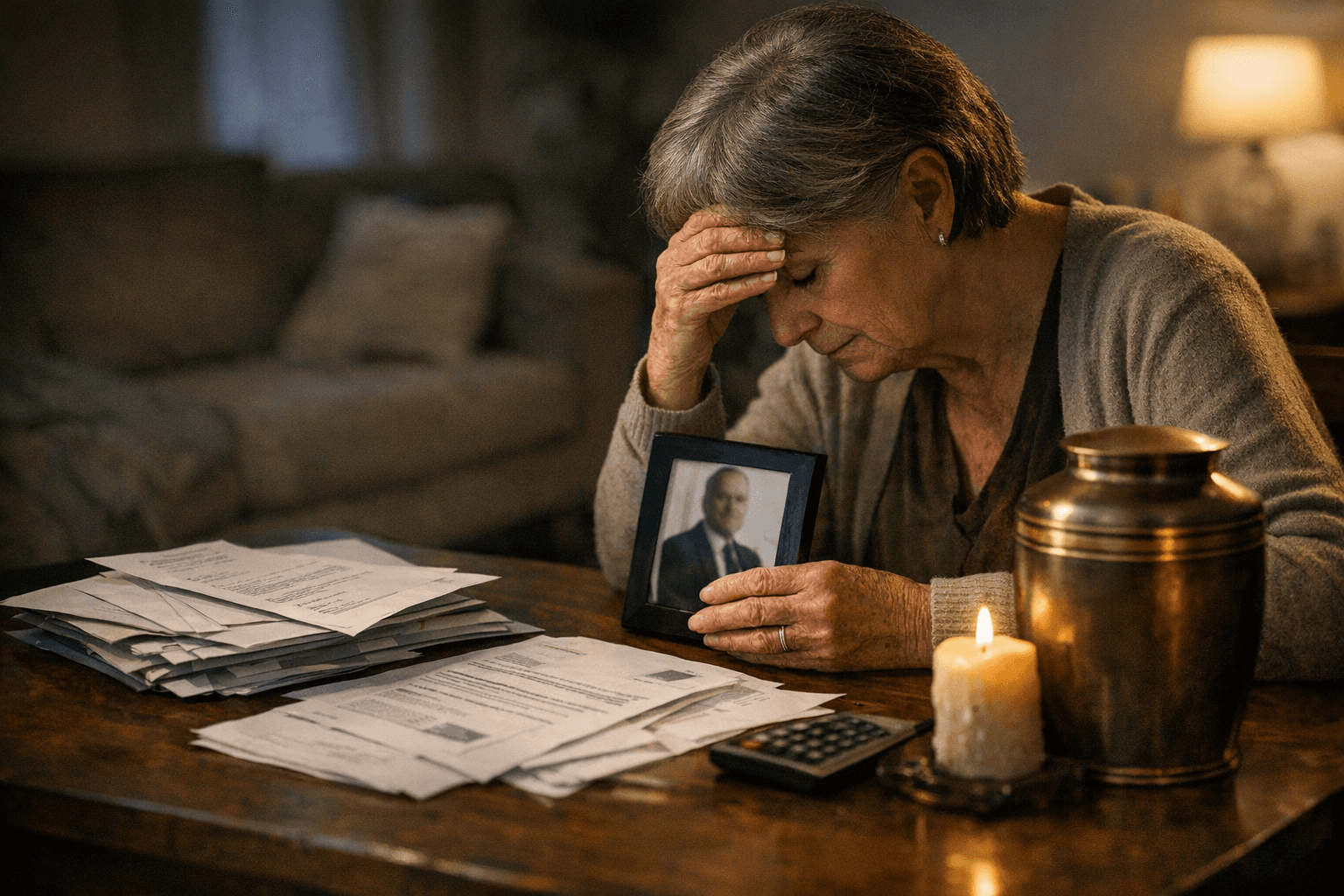

A widower trying to access his late wife's Premium Bonds. A family forced to hire lawyers after NS&I lost track of two accounts in an investment portfolio. Letters sent to people who had already died. These are among the documented failures that have pushed the government-backed bank into a compensation reckoning after a series of errors dating back years, with some bereaved families saying they did not receive money that was rightfully theirs.

National Savings and Investments is expected to pay hundreds of millions of pounds in compensation after errors left bereaved families without money, with claims potentially affecting about 37,000 customers. Treasury officials are understood to be working with NS&I to determine the exact amount to be given to customers.

Families of deceased NS&I savers have accused the bank of losing track of investments, delaying payouts, and withholding Premium Bond prizes, incurring thousands in additional costs in lawyer expenses. Some were made to pay fines to HMRC after receiving incorrect information from NS&I call handlers. Others claim to have lost thousands of pounds in interest because of delays in money being released, or have even missed out on buying homes. Documents seen by The Telegraph reveal families received letters addressed to deceased relatives, adding to their stress and grief.

The scale is striking: NS&I manages around £100 billion for more than 26 million people, and recorded complaints increased from 73,000 in the second half of 2021 to almost 160,000 in the first half of last year, per data from the Financial Ombudsman Service.

Pensions Minister Torsten Bell addressed MPs in the House of Commons on Thursday. Bell was likely to face questions as to whether taxpayers could end up responsible for any compensation bill. Some reports have put the potential figure as high as £400 million.

The failures are inseparable from a broader operational crisis inside NS&I. Programme costs for the bank's digital transformation have ballooned from £1.3 billion to £3 billion with nothing meaningful delivered. By 2024, NS&I had hired 150 additional staff, spent £43 million on consultants, and brought in Capgemini as systems integrator, yet there was still no integrated plan despite persistent over-confidence about delivery. The House of Commons Public Accounts Committee labelled the effort a "full-spectrum disaster."

NS&I said it expects the programme to end when the Atos contract expires in March 2028, four years later than its original schedule of 2024. MPs noted that NS&I has been unable to provide clear information on how much has already been spent, and even HM Treasury has acknowledged that it has struggled at times to understand the programme's costs and progress.

NS&I, originally set up in 1861 as the Post Office Savings Bank, serves more than 24 million people with a range of savings and investment offers. Customers include more than 22 million Premium Bonds holders, who stand to win money from a monthly prize draw.

The bank issued an apology on Wednesday. A spokesperson said: "We recognise that dealing with bereavement can be challenging and would like to apologise to anyone who has not received the customer service from NS&I that they should expect, particularly at such a sensitive time." Zoe Gillespie, investment manager at RBC Brewin Dolphin, noted that the scale of the problem remains unclear, and with Parliament now scrutinising both the compensation liability and a transformation programme that MPs say has "no workable plan," NS&I's leadership faces pressure from every direction simultaneously.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?