OBR to bake in more persistent inflation in next forecasts

A more persistent inflation path could leave households paying higher borrowing costs and cut Rachel Reeves’ room for tax cuts, as the OBR rethinks its outlook.

Britain’s budget watchdog is preparing to assume inflation lasts longer than it expected just months ago, a shift that could keep mortgages, rents and borrowing costs elevated while narrowing Rachel Reeves’ room for giveaways in the next Budget.

The Office for Budget Responsibility said it will fold in the unexpectedly stubborn inflation that followed the 2022 energy shock when it updates its forecasts later this year, with heightened energy-price volatility and the Iran war now back in focus. The change matters because the OBR’s numbers feed directly into fiscal planning and help ermine how much headroom the chancellor has for tax cuts or new spending commitments.

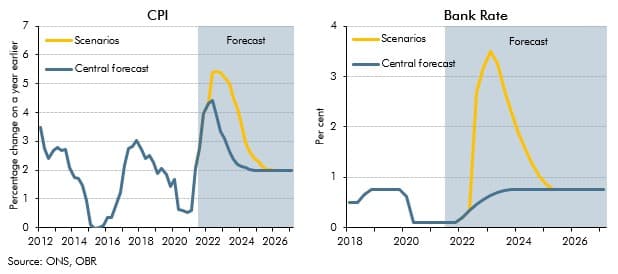

The watchdog’s latest official outlook, published on 3 March 2026, covered the economy and public finances through 2030-31. In that forecast, UK inflation was expected to average 2.3% in 2026 before returning to the Bank of England’s 2% target in 2027. It also gave Reeves about £23.6 billion of fiscal headroom for 2029/30, a buffer that can quickly evaporate if borrowing costs or inflation prove stickier than assumed.

That caution is rooted in the OBR’s own post-mortem on recent forecasts. Its Forecast evaluation report, released on 2 June 2026, said the ongoing impact of unexpected shocks, especially the 2022 energy shock, explained a large portion of the forecast differences seen in 2024-25. The OBR’s inflation data underline how sharp that shock was: UK CPI inflation hit 11.1% in October 2022, the highest in 41 years, before easing back toward target.

The government had already been telling investors and voters in March that inflation, borrowing and debt interest were expected to fall, while investment would rise. It also said measures in the last Budget were expected to reduce inflation by 0.4 percentage points in 2026-27. But if the OBR now bakes in a stickier price path, that reassurance may have to be revised just as the Treasury faces slower growth, higher debt-servicing pressures and a narrower choice between tax cuts and spending promises.

For households, the implications are direct. A more persistent inflation outlook can keep the Bank of England cautious, prolonging pressure on mortgage rates and other borrowing costs. For the government, it means the fiscal arithmetic could become less forgiving, with less scope to absorb shocks or announce politically attractive measures without testing the limits of Reeves’ budget room.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?

%3Amax_bytes(150000)%3Astrip_icc()%2FCertificate-of-deposit-2301f2164ceb4e91b100cb92aa6f868a.jpg&w=1920&q=75)