One year after Trump tax law, benefits and costs split unevenly

One year in, the law’s biggest gains have gone to higher earners, while Medicaid, SNAP and state budgets absorb much of the cost.

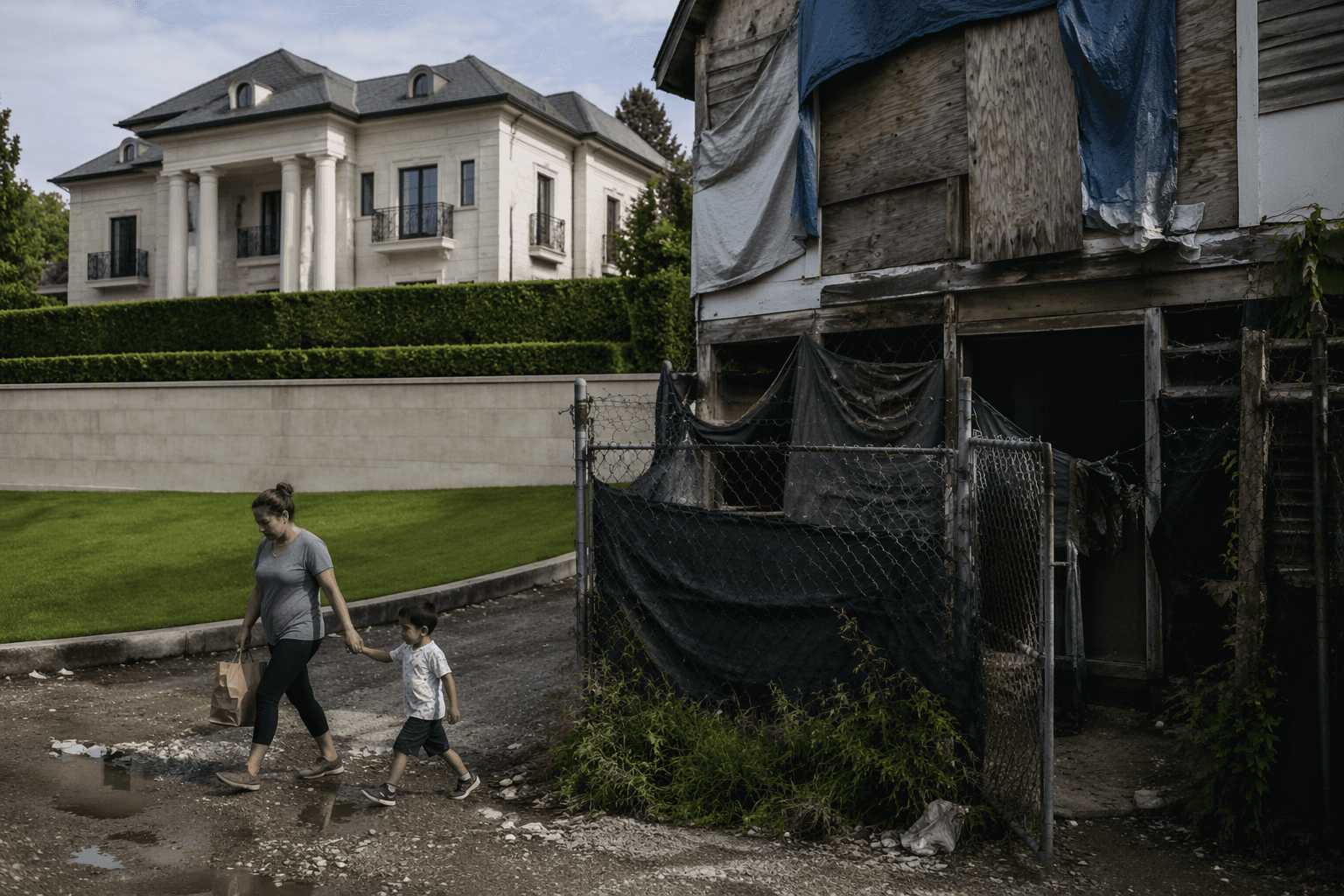

One year after President Donald Trump signed the One Big Beautiful Bill Act, the law’s clearest effects are showing up exactly where supporters and critics said they would, but not in equal measure. The 870-page package locked in and expanded tax breaks for higher-income households while trimming major safety-net programs, leaving households, states and federal agencies to absorb the uneven fallout.

The tax winners are concentrated at the top

The law made the 2017 Trump tax cuts permanent and added a larger state-and-local-tax deduction, a senior bonus and a higher estate and gift tax exemption. Those changes deliver the biggest dollar gains to higher-income households, homeowners, seniors and wealthy families, not evenly across the income ladder.

That distribution matters because a bigger deduction or exemption is worth far more to households with large tax bills or sizable assets than to families living paycheck to paycheck. The law’s design also means the headline promise of broad tax relief has translated into the largest gains for people already best positioned to benefit from itemized deductions, homeownership and estate planning.

The political selling point was permanence. Supporters argued that making the 2017 cuts durable would give households and businesses more certainty after years of temporary extensions and cliff-edge debates in Washington, D.C. One year later, the clearest certainty is who benefited most: households with more income, more wealth and more room to use the new tax preferences.

The federal deficit burden is still front and center

The cost of those tax changes was never small. The Congressional Budget Office and the staff of the Joint Committee on Taxation estimated that the House-passed version of the bill would increase the primary deficit by $2.4 trillion over 2025 to 2034.

That number is more than a budget score. It signals that the law shifts a large share of the bill to future federal finances, even as it immediately delivers tax relief to favored groups. Later analyses described the enacted law as adding substantially to debt, reinforcing the core fiscal tradeoff: lower taxes now, heavier borrowing later.

The law’s supporters framed that as an acceptable price for tax permanence and faster growth. Critics saw a transfer of costs away from the federal government and toward states, families and safety-net programs. One year later, the fiscal pressure is visible not just in Washington, but in the programs the law pulled back.

Medicaid is where the cuts land hardest

The health-policy changes are broad and consequential. They include new Medicaid work and reporting requirements, more frequent eligibility redeterminations, tighter rules for some marketplace coverage and new constraints on state financing mechanisms. In practice, those provisions make enrollment harder to keep and federal spending harder to sustain.

KFF has estimated that the law would reduce federal Medicaid spending by $911 billion over 10 years and increase the number of uninsured people in 2034 by 10 million. In a later cost estimate based on the latest Congressional Budget Office figures, KFF put the Medicaid spending reduction at $793 billion and the uninsured increase at 7.8 million. The estimates differ, but they point in the same direction: less federal support and more people outside coverage.

Medicaid work requirements account for a large share of the projected coverage losses. Nebraska became the first state to implement them under OBBBA on May 1, 2026, and the Centers for Medicare and Medicaid Services followed in June 2026 with an interim final rule spelling out how states verify compliance and exemptions. That sequence matters because it turns a federal policy into a state administrative burden almost immediately, with eligibility checks, reporting systems and exemption reviews now part of day-to-day Medicaid operations.

Hospitals, clinics and state Medicaid agencies are now dealing with the downstream effect. More people losing coverage means more uncompensated care, more pressure on safety-net providers and more strain on state systems already trying to implement the new rules.

SNAP is already shrinking

Food aid is another clear loser. The Center on Budget and Policy Priorities reported that nationwide SNAP participation fell by more than 4 million people, nearly 10 percent, between the law’s July 2025 enactment and March 2026.

That drop is not just a statistic on a spreadsheet. It means fewer households receiving grocery assistance and more pressure on food banks, local charities and state administrators who must navigate the new eligibility and reporting rules. As with Medicaid, the law’s effect is not limited to federal spending totals. It changes who gets help, how quickly they can get it and how much stress lands on local institutions when they do not.

The USDA and other federal implementation agencies have been issuing guidance as the law takes effect, but the participation decline shows that the policy is already reshaping the low-income safety net. For families that were relying on SNAP and Medicaid together, the combined effect can be especially sharp.

States are taking on more of the burden

Supporters promised tax relief and a sturdier federal tax code. What is emerging instead is a larger transfer of administrative and financial pressure to states. Medicaid work requirements, more frequent eligibility checks and tighter financing rules force states to build systems, verify records and absorb errors when eligible people fall through the cracks.

That matters for state budgets because Medicaid and SNAP are not just social programs. They are major pieces of state administrative machinery, and when federal rules tighten, states often pay in staffing, technology and back-office costs even when federal spending falls. Nebraska’s early implementation is a preview of what other states may face as deadlines approach and CMS guidance becomes operational.

The broader reach of the law adds to that pressure. It also affects student loans, Medicare, energy policy, and federal leasing and royalty rules, widening the set of winners and losers beyond households and health programs. The result is a tax law that reaches deep into the budget structure of the United States, not just into annual filing season.

A year later, the promises look narrower than the footprint

The central political promise was simple: protect the 2017 tax cuts, deliver relief and make the code more durable. The reality one year later is more split. Higher-income households, homeowners, seniors and wealthy families are seeing the clearest tax gains. Medicaid recipients, SNAP households, state agencies and safety-net providers are seeing the clearest costs.

That divide is what makes OBBBA more than a partisan trophy. It is a multi-year restructuring of who pays taxes, who qualifies for aid and which level of government absorbs the strain when the numbers stop balancing.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?