Petra Diamonds Reports US$100m H1 Revenue, Cites Tender Timing, Refinancing Progress

Petra posted US$100m in H1 revenue, blamed December-January tender timing for weaker sales and closed the period with US$284m net debt inclusive of fair value adjustments.

Petra Diamonds reported revenue of US$100 million for the six months ended 31 December 2025, saying the timing of December 2025 and January tenders pushed sales into H2 FY2026 and left the group with negative operating cashflow of US$6 million. The company also highlighted a successful refinancing and an enlarged focus on working capital as central to its near-term stability.

“H1 FY 2026 signalled a pivotal period for the Group, with the successful refinancing and extension of our debt facilities, providing greater stability to the Group’s capital structure,” joint CEOs Vivek Gadodia and Juan Kemp said in the company’s interim release. The pair added that Petra had seen an improvement in product mix at Cullinan and noted the recovery of a 41.82 carat Type IIb blue stone in late December 2025 as evidence of ore-body quality.

Financial detail in the interim results shows adjusted EBITDA of US$26 million for H1 FY2026, up from US$15 million in the prior period, driven largely by a US$26 million reduction in adjusted mining and processing costs and partly offset by US$15 million lower revenue and US$2 million other costs. The group recorded a basic loss per share from continuing operations of US$0.70 and an adjusted loss per share of US$0.10 after non-controlling interests. Capital expenditure reached US$34 million, a 13 percent rise year-on-year, with capex guidance weighted towards the second half of the financial year.

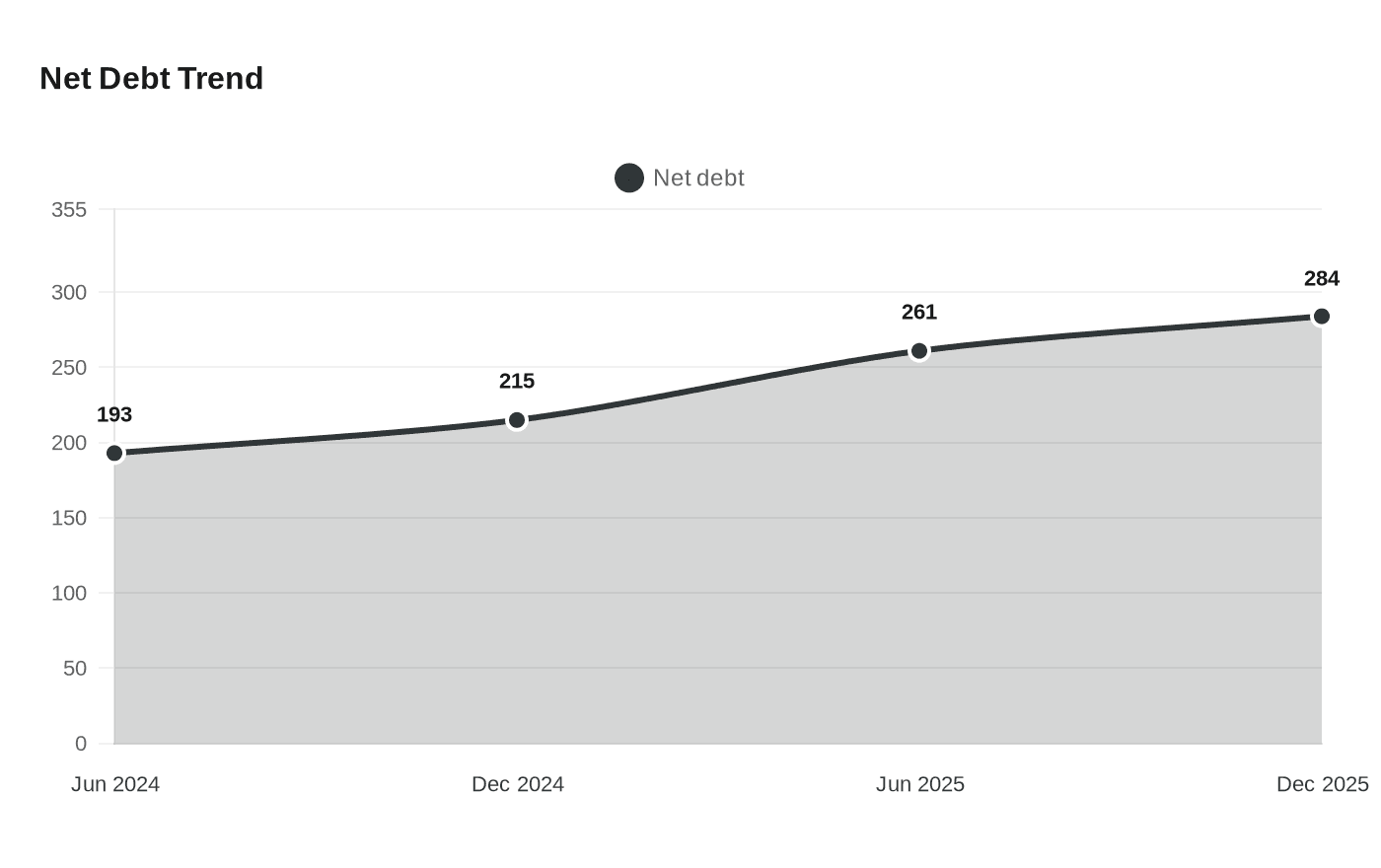

Liquidity and balance-sheet moves were front of mind. Petra closed the half with net debt of US$284 million, “inclusive of fair value adjustments,” compared with US$261 million at 30 June 2025, US$215 million at 31 December 2024 and US$193 million at 30 June 2024. Unrestricted cash balances stood at US$36 million and diamonds on hand increased to 608,217 carats valued at US$46 million from 385,878 carats worth US$40 million a year earlier.

Market dynamics underpinned the numbers. Rapaport reported H1 sales volume of 963,523 carats and an average price of US$104 per carat for the period, noting that average price fell 11 percent in the second quarter versus the first and that like-for-like prices were down about 20 percent in Q2, with product mix partly offsetting the decline. Historical tender data for FY2025 show volatility: Tender 3 (Dec 24) sold 700,803 carats for US$71 million at US$101/ct, while Tender 4 (Feb 25) sold 476,265 carats for US$39 million at US$83/ct, and, as AWS noted, “Average prices decreased 18% over Tender 3 FY 2025, with product mix contributing 12% and a 6% decrease in like-for-like prices.”

Petra also signalled strategic shifts: a partnership with Bonas Group to market rough diamonds in Antwerp and Dubai, and management measures to conserve cash. “The significant appreciation of the Rand against the US Dollar is another major headwind facing the Business. While we partly mitigated the stronger Rand through hedges in H1 FY 2026, the continued strength of the Rand going forward remains a risk to the Business,” the joint CEOs warned. AWS materials additionally treat Williamson as a discontinued operation with a sale to Pink Diamonds expected in Q1 CY2025.

What matters next is execution: whether the refinancing and tighter cost controls can offset tender scheduling into H2 FY2026, how the improved product mix at Cullinan translates into realised prices, and whether working capital optimisation and marketing flexibility via Bonas will convert the enlarged on-hand inventory into cash before currency and pricing pressures deepen.

Know something we missed? Have a correction or additional information?

Submit a Tip