Private Equity Roll-Ups Reshape Agency M&A Landscape in 2026

Stand-alone agencies are selling at just 4x EBITDA while PE-backed roll-ups command 8-12x. The gap tells founders exactly what they need to fix.

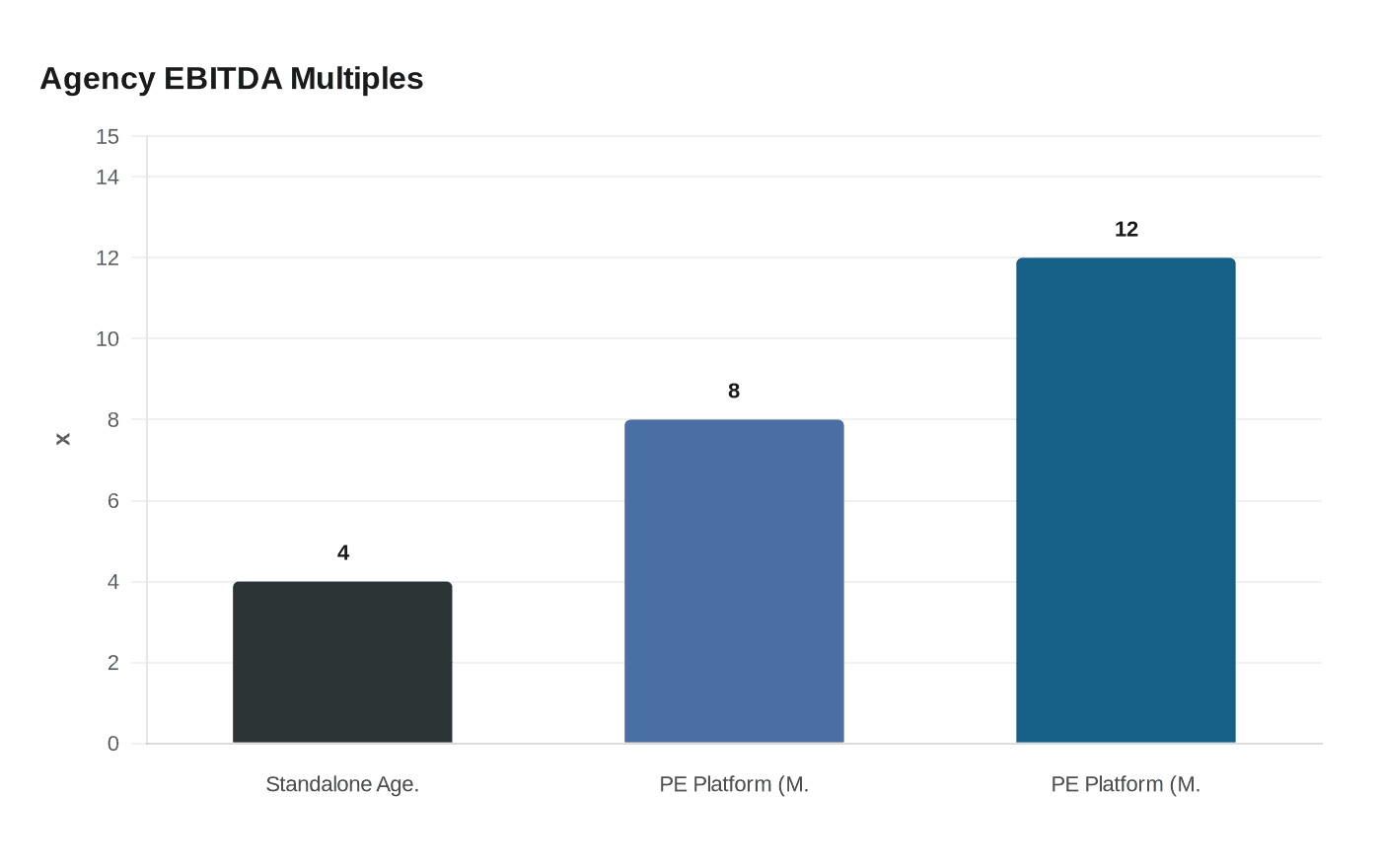

The math driving private equity interest in agency M&A is brutally simple: a stand-alone shop with $2 million in EBITDA gets valued at roughly 4x, while the same revenue folded into a PE-backed platform can command 8 to 12 times earnings. That spread, the engine behind what Agencies.co described in a March 25 analysis as an accelerating roll-up wave across the marketing and digital agency sector, is now reshaping who wins, who sells, and who gets left competing against a better-capitalized version of themselves.

The roll-up playbook PE buyers are running follows a consistent structure. A platform acquisition, typically a firm with $3 million to $10 million in EBITDA and a management team that can survive founder departure, anchors the strategy. Bolt-on acquisitions of smaller agencies, those generating $500,000 to $3 million in EBITDA, fill in vertical or capability gaps. Shared services, finance, HR, and tooling, get centralized to expand margins. Cross-selling then goes to work across the combined client base. The result is a business that looks nothing like the sum of its parts at the point of acquisition.

Agencies with 70% or more of revenue tied to retainers typically command multiples one to two turns higher than project-based agencies with similar EBITDA. That single metric, retainer concentration, functions as a proxy for predictability, which is exactly what PE underwriting demands. Founders running mixed retainer-project books should treat the ratio as a dashboard warning light, not a strategic abstraction.

Agencies where no single client exceeds 10% of revenue are considered low-risk targets, while those with a top client representing 20 to 30% of revenue face discounts of 10 to 20% on their valuation, and concentration above 30% can derail a deal entirely. Client concentration is the operational equivalent of single-point-of-failure infrastructure: buyers price it aggressively because they have seen the post-close consequences.

For agency owners evaluating their position in this environment, the Agencies.co analysis identified five concrete preparation steps: strengthen recurring revenue through retainer and subscription structures; standardize and document SOPs; clean up financials and prepare adjusted EBITDA bridges; reduce single-client concentration; and build talent retention plans that reduce owner-dependency risk. None of these are novel concepts, but the difference between knowing them and executing them is the difference between a $4 million check and a $10 million one.

White-label specialists face a different version of the same pressure. As PE platforms consolidate larger agency buyers, procurement decisions increasingly favor vendors with enterprise-grade compliance and integration capabilities. That creates a fork: become acquisitive, align with a roll-up platform, or carve a differentiated niche in services too specialized for PE buyers to standardize at scale.

The longer-term effect of the consolidation wave is professionalization at the operational level. Agencies that survive it, whether by selling, scaling, or specializing, will be forced into the kind of process discipline that most founder-run shops have historically deferred.

Sources:

Know something we missed? Have a correction or additional information?

Submit a Tip