Rising prices push more households to borrow for groceries and essentials

Families are putting groceries on credit as household debt hit $18.8 trillion and card balances climbed to $1.28 trillion. Delinquencies are rising too.

Rising prices for gas, groceries and other basics have turned ordinary shopping trips into borrowing decisions. More households are cycling through credit cards, payday loans, savings and buy-now-pay-later loans just to cover recurring essentials, and the pressure is showing up in the balance sheets of American consumers. When the monthly budget is already stretched by food and fuel, the next stop is often revolving debt.

That strain arrived as U.S. household debt reached a record $18.8 trillion in the fourth quarter of 2025, according to the Federal Reserve Bank of New York. Credit card balances rose by $44 billion to $1.28 trillion, up 5.5% from a year earlier, while 4.8% of outstanding debt was in some stage of delinquency at the end of December. The Federal Reserve Board has said credit card delinquency rates, after falling sharply early in the pandemic, returned to pre-pandemic levels by 2023:Q1 and were still rising through 2024:Q3.

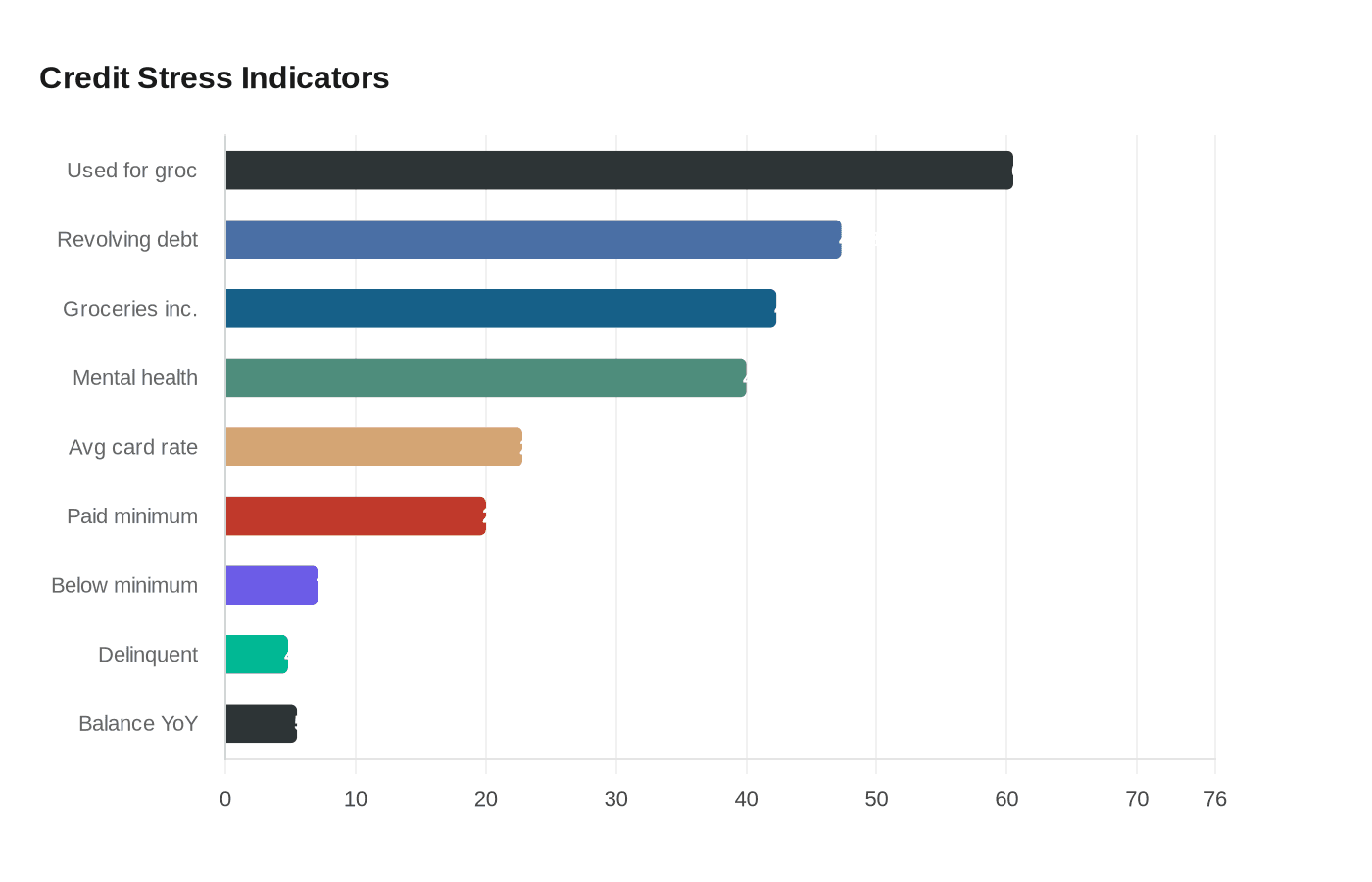

The story is especially stark at the grocery aisle. In an Urban Institute analysis of 2023 survey data, 60.5% of adults ages 18 to 64 said they used credit cards to buy groceries. Of that group, 20% said they did not pay the full balance but made at least the minimum payment, and 7.1% said they did not even meet the minimum payment. The Urban Institute tied that borrowing to high food costs, the end of pandemic-era supports and higher borrowing costs, with low-income families hit hardest because they spend almost a third of their budgets on food.

The cost of carrying that debt has risen with it. The Urban Institute said average credit card interest rates reached a record 22.8% in 2023, making each unpaid grocery bill more expensive to carry into the next month. That helps explain why a temporary fill-in for essentials can quickly become a long-running financial drag, especially when the debt is used for items households need every week rather than one-time purchases.

LendingClub’s November 2024 research found that 47.3% of Americans had accumulated some revolving credit card debt, and 42.3% of respondents said food and groceries were their largest category of increased credit-card spending. The same survey found 40% said credit-card debt was taking a toll on their mental health. The numbers point to a broader squeeze: once wages fail to keep up with essentials, savings get used up, credit limits get tested and delinquency becomes the next risk in line.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?