Samsung Forecasts Record Q4 Operating Profit as AI Memory Demand Surges

Samsung Electronics projected a record fourth-quarter operating profit of about 20 trillion won, driven by a sharp tightening in memory supply and strong AI-related demand that has pushed DRAM and HBM prices higher. The results lift revenue above 90 trillion won for the first time and underscore the outsized impact of the AI infrastructure build-out on South Korea’s largest exporter.

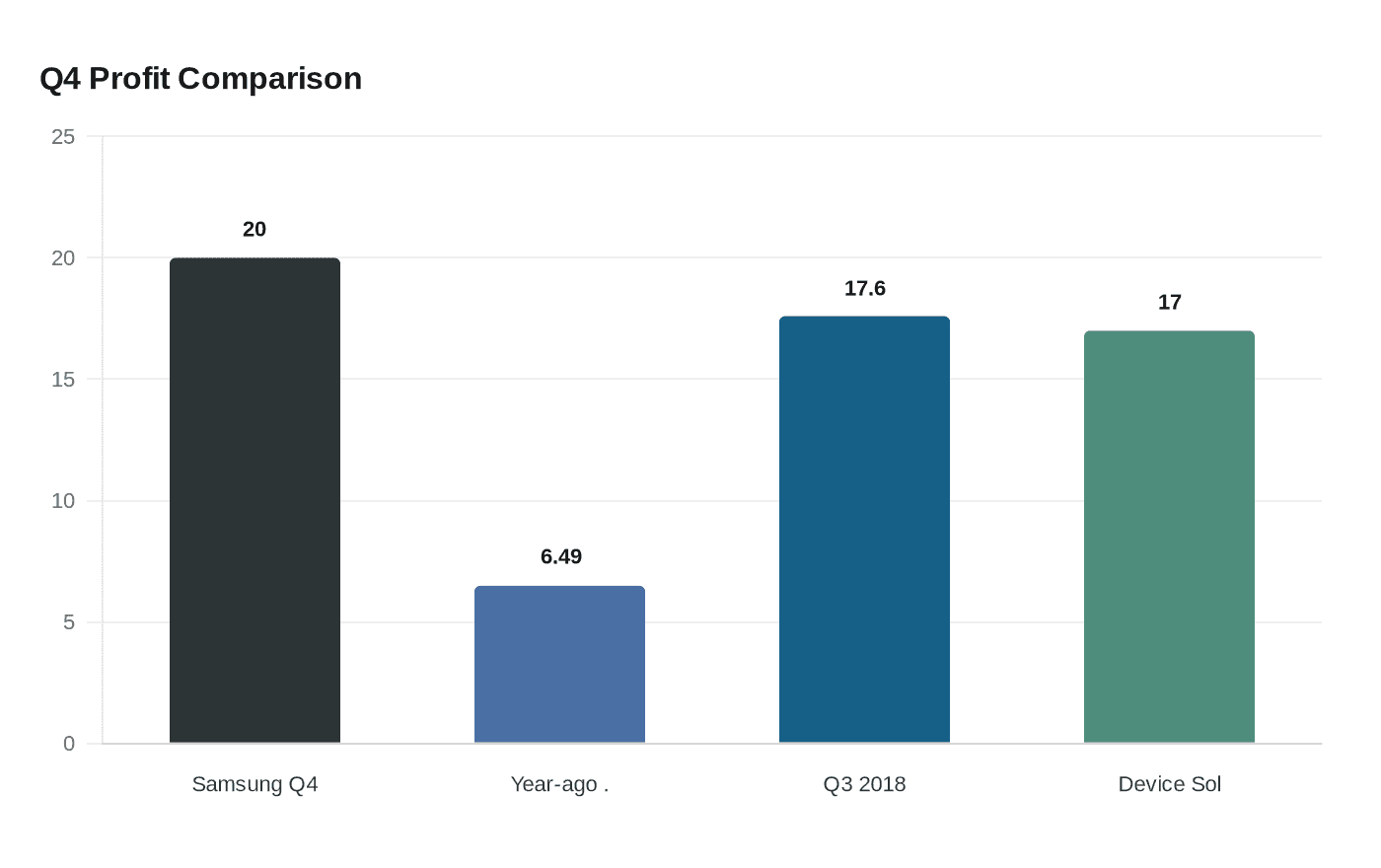

Samsung Electronics projected about 20 trillion won in operating profit for the fourth quarter, a near threefold increase from 6.49 trillion won a year earlier and the highest quarterly profit in the company’s history. The preliminary estimate, given on January 8, put the figure in a narrow band of roughly 19.8 trillion to 20.1 trillion won, or about $13.8 billion, while fourth-quarter revenue was forecast at roughly 93 trillion won, up about 23 percent year-on-year and the first time quarterly sales surpassed 90 trillion won.

The leap in profitability reflects a dramatic change in the memory market. A surge in demand for artificial intelligence infrastructure has pushed orders for conventional DRAM and high-bandwidth memory used in AI accelerators into server procurement cycles, tightening supply and driving contract pricing sharply higher. Market analysis shows conventional DRAM contract prices could rise another 55 to 60 percent in the current quarter from the prior quarter, amplifying margin leverage for producers with sizeable memory operations.

Analysts attribute the bulk of Samsung’s provisional profit to its semiconductor division. Estimates of operating profit for the Device Solutions unit cluster in the 15 trillion to 17 trillion won range, with one senior analyst estimating about 17 trillion won, meaning the memory business alone will likely account for the lion’s share of the company’s quarterly earnings. A consensus tracker that aggregated analyst forecasts had stood near 18 trillion won, so Samsung’s provisional result marginally exceeded that benchmark.

The scale of the windfall eclipses the previous quarterly profit record of 17.6 trillion won set in the third quarter of 2018 and has reverberated through financial markets. Investors have pushed Samsung shares to fresh highs, extending a roughly 155 percent rally over the past year as the company’s exposure to the AI-driven memory cycle has become a central growth narrative for the stock.

For Samsung and South Korea’s export-dependent economy, the boom carries immediate upside and medium-term questions. The stronger revenue and profit will feed corporate cash flow, support capital spending plans and boost tax receipts, potentially widening the current-account surplus tied to semiconductor exports. At the same time, the episode reinforces industry concentration risk: Samsung and a handful of producers capture a disproportionate share of earnings in a memory cycle that can be rapid and volatile.

Looking ahead, order visibility for high-bandwidth memory and server DRAM extends into 2026, providing firms with planning runway for production and investment. Yet analysts caution that duration and downside risks remain; steep price increases can prompt accelerated capacity additions that eventually moderate profitability, and geopolitical or supply-chain disruptions could alter demand patterns. The immediate picture is unequivocal: AI-driven buying has tightened supply and lifted prices, turning Samsung’s memory exposure into a record-setting profit engine for the quarter and reshaping near-term dynamics across the global semiconductor market.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?