SpaceX Targets June IPO Roadshow, Seeks $75 Billion at $1.75 Trillion Valuation

SpaceX set a June 8 roadshow date and briefed Wall Street banks on a $75 billion raise that could value the company at a record $1.75 trillion.

SpaceX laid out concrete plans to its banking syndicate for an initial public offering, setting a roadshow start date of the week of June 8 and a prospectus expected to go public in late May. The company is targeting a raise of roughly $75 billion that could value it at $1.75 trillion, a figure that would make it the largest IPO in history by a significant margin.

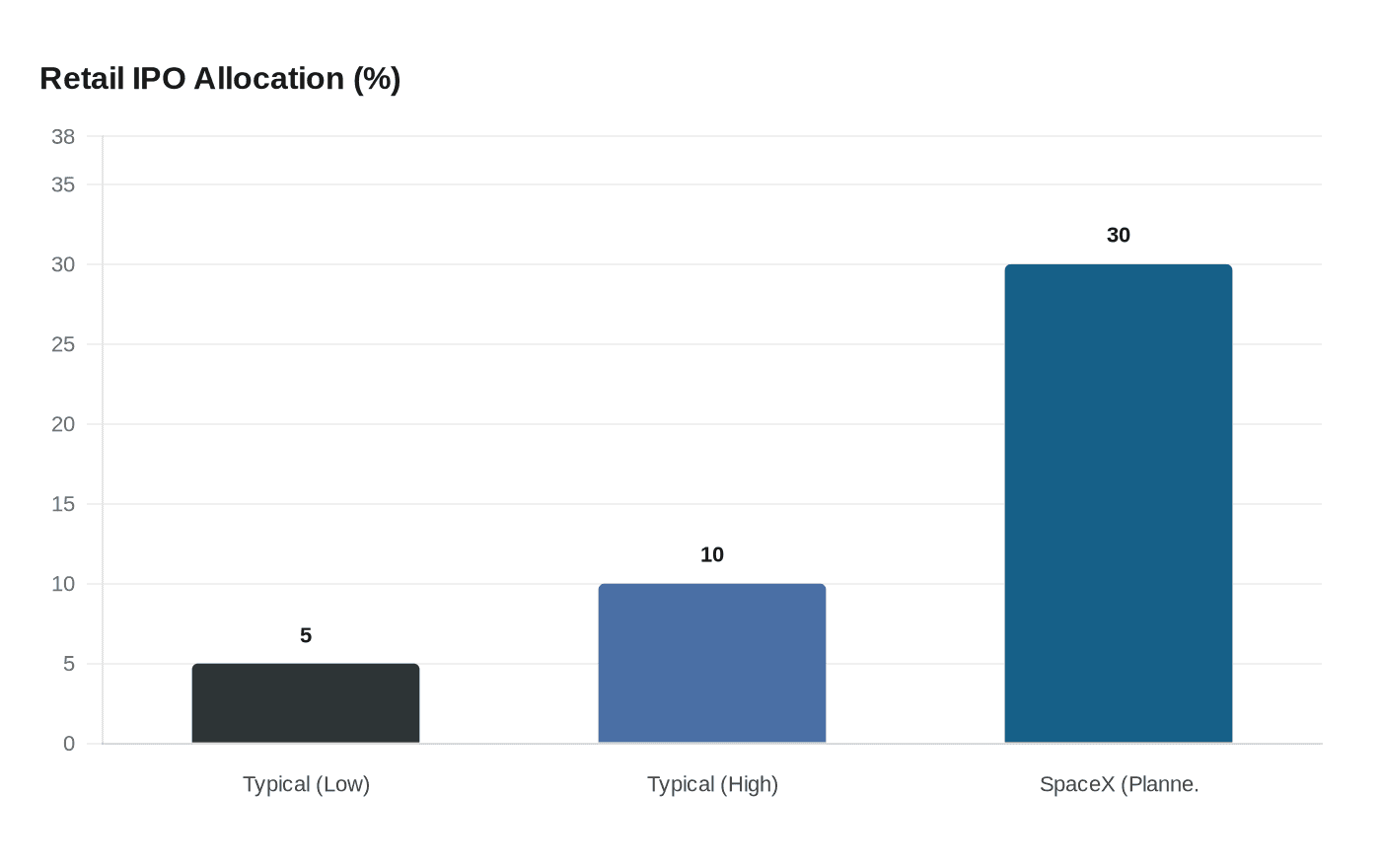

The structure carries an unusual feature: Elon Musk has reportedly considered allocating up to 30% of the offering to retail investors. In a typical mega-offering, individual investors receive between 5% and 10% of available shares. A 30% retail slice would represent a sharp departure from standard bookbuilding practice, complicating the logistics of pricing and aftermarket stability. SpaceX plans to reinforce that populist framing by hosting roughly 1,500 individual investors at a dedicated event after the institutional roadshow concludes, a format rarely deployed at this scale. What it cannot offer those investors is the kind of lockup protections, allocation guarantees, or pre-IPO due diligence access that institutional buyers negotiate as a matter of course.

The banking syndicate assembled for the deal is comprehensive: Morgan Stanley, Bank of America, Citigroup, JPMorgan, and Goldman Sachs are among the lead underwriters and active bookrunners being lined up. SpaceX has already filed confidential draft registration materials with the Securities and Exchange Commission, allowing it to work through disclosures with regulators without yet making the details public. Concrete filing dates, price ranges, and share counts remain subject to change ahead of the prospectus.

The valuation story rests on two businesses with meaningfully different risk profiles. Starlink, SpaceX's satellite broadband unit, has emerged as a genuine cash-generating operation with millions of global subscribers and expanding government contracts. The launch business, anchored by ongoing Starship development costs that have not been disclosed publicly, carries heavier capital requirements and longer payback horizons. A third variable sits in national security exposure: regulators and government officials are expected to scrutinize the S-1 for disclosures around export controls, classified defense contracts, and sensitive space capabilities, each of which could complicate or delay the offering. How SpaceX characterizes those relationships in its prospectus will be among the most closely watched sections of the filing.

At $75 billion, the raise would dwarf every prior IPO and effectively reshape the 2026 equity calendar. Market strategists have warned the deal could "suck the oxygen" out of the IPO market, concentrating both institutional and retail attention on SpaceX while other companies struggle to price or place their own offerings. For private-market investors who have accumulated SpaceX shares through secondary transactions, the float represents a long-awaited liquidity event. For anyone considering buying in at a $1.75 trillion valuation, the more pressing question is what those late-May filings actually reveal about the company's unit economics, contract dependencies, and how much of that number is Starlink's cash flow versus Musk's story.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?