Sun Pharma warns of slower growth after strong FY26 results

Sun Pharma said FY27 revenue may grow only in the high single digits after FY26 sales rose 11.9%, a sign that regulatory and pricing pressures are cooling the generics trade.

Sun Pharmaceutical Industries signaled that its next growth phase may be harder to sustain, even after posting a strong FY26. The company told investors to expect high single-digit consolidated top-line growth in the current fiscal year, a cautious outlook that reflects tighter regulatory conditions, macro uncertainty and a tougher backdrop for the global generics business.

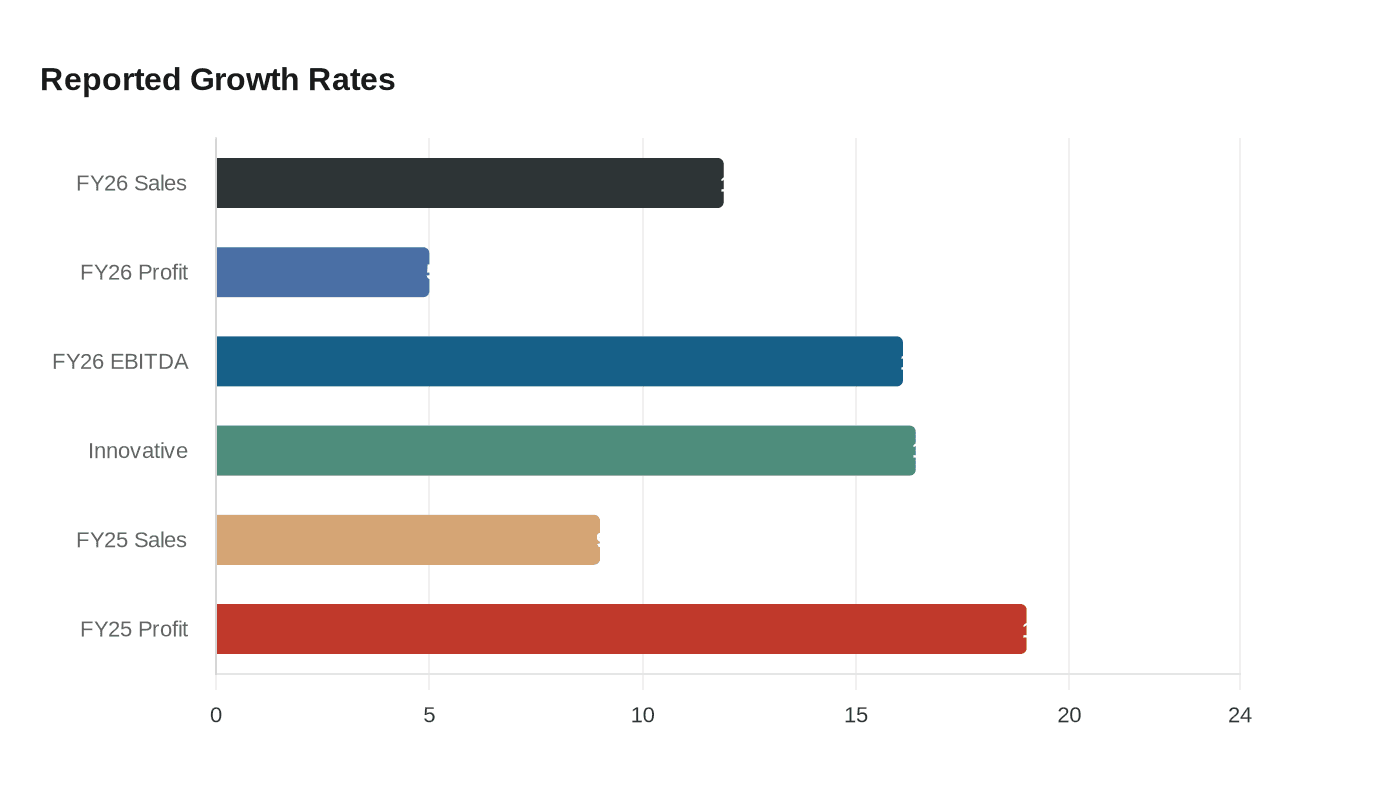

For FY26, Sun Pharma reported consolidated sales of Rs 582,201 million, up 11.9% from a year earlier. Net profit rose 5.0% to Rs 114,794 million, while EBITDA climbed 16.1% to Rs 177,314 million and the EBITDA margin improved to 30.3%. The board recorded the results on May 22, 2026, and proposed a final dividend of Rs 5.00 per share, bringing total FY26 dividends to Rs 16.00 per share, unchanged from FY25.

The sharper message for investors was not the year’s strong numbers, but the slower pace management sees ahead. Executive chairman Dilip Shanghvi tied the forecast to Sun Pharma’s current reading of regulatory and macroeconomic conditions, a phrase that points to pressure on approvals, manufacturing timelines, market access and pricing power. For a company that is India’s largest pharmaceutical group by revenue and market value, that tone matters well beyond one earnings cycle.

Sun Pharma has spent years trying to shift more of its business toward higher-value medicines, and that effort remains visible in the FY26 mix. Global innovative medicines sales reached US$1.42 billion, up 16.4%, and accounted for 20.7% of sales. In the March quarter, innovative medicines brought in US$354 million, or 22.2% of quarterly sales. The company launched 11 new products in the fourth quarter and 37 across the full year, reinforcing the move toward branded and specialty therapies that usually carry better margins than commoditized generics.

Still, the transition is unfolding under strain. In September 2025, Sun Pharma disclosed that its Halol facility in Gujarat had been classified as Official Action Indicated by the U.S. Food and Drug Administration after a June 2-13, 2025 inspection. The site remained under Import Alert, limiting shipments into the United States except for certain drug-shortage exemptions until compliance is restored. That kind of restriction can hit supply flows, delay revenue and weigh on investor confidence across the sector.

The comparison with FY25 shows how quickly the cycle can turn. Then, Sun Pharma reported gross sales of Rs 520,412 million, up 9.0%, and adjusted net profit of Rs 119,844 million, up 19.0%. Global specialty sales were US$1.216 billion, equal to 19.7% of sales. By FY26, Sun Pharma’s India market share had risen from 8.1% to 8.4%, its strongest gain since the Ranbaxy acquisition, but the company is now warning that the next leg of growth will not come as easily. That caution is likely to shape how investors read pricing pressure, regulatory risk and supply expectations across India’s drug makers.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?