Supreme Court weighs SEC disgorgement power in fraud case

The justices took up whether the SEC can keep stripping fraud profits from defendants like Ongkaruck Sripetch, whose case involves more than $3 million.

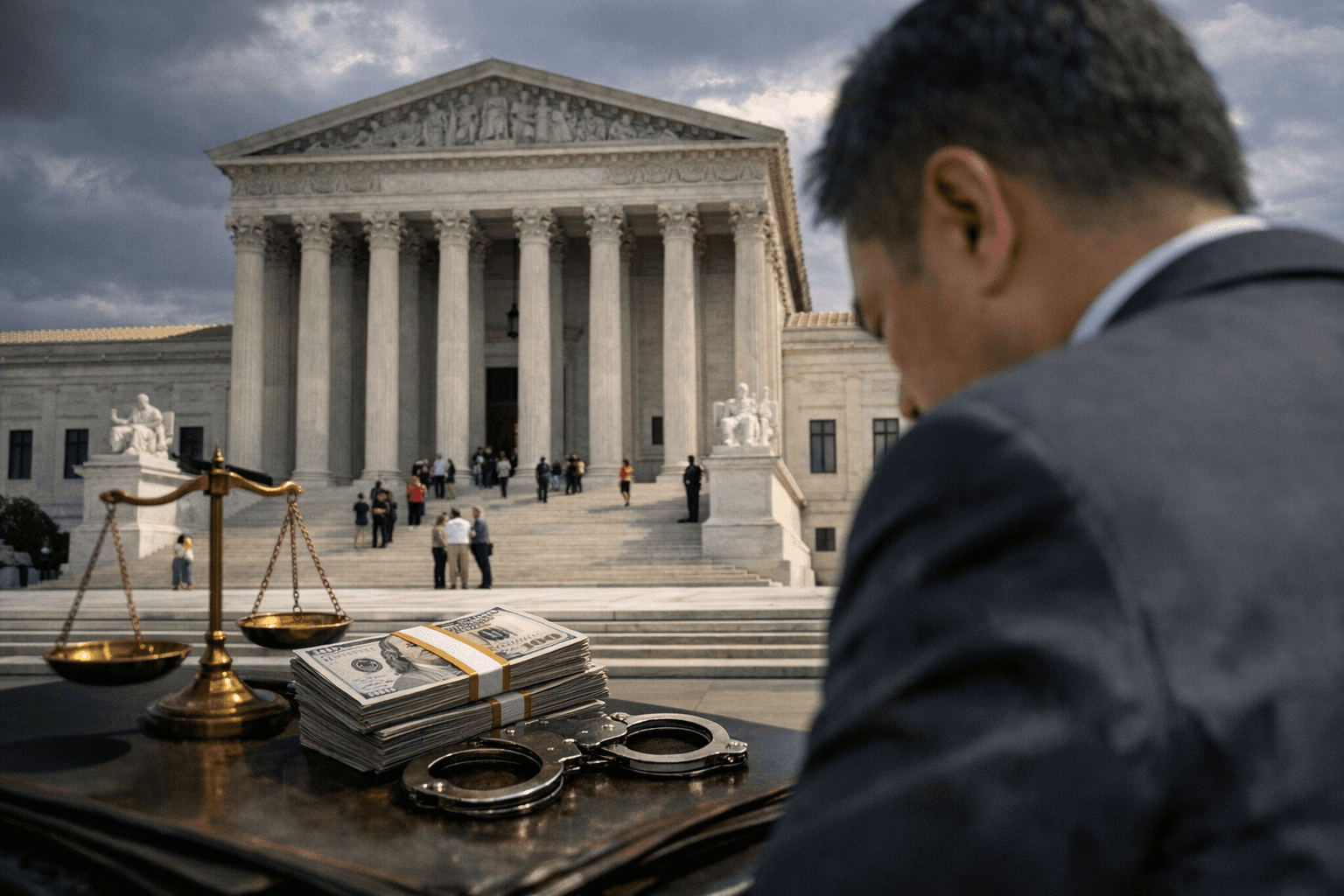

The Supreme Court weighed whether the SEC can keep using disgorgement to force fraud defendants to give up illegal profits, a remedy that has become central to how Wall Street regulators recover money and deter misconduct. In Ongkaruck Sripetch v. Securities and Exchange Commission, the justices examined whether the agency may seek equitable disgorgement under federal securities law without showing that investors suffered pecuniary harm.

In plain English, disgorgement means making a wrongdoer hand over the money earned through misconduct. In Sripetch’s case, the defendant was ordered to repay more than $3 million in ill-gotten gains, plus interest, and the district court’s 2025 judgment also included language allowing contempt if he did not pay. The SEC has defended that broader authority as essential to preventing defendants from keeping the proceeds of fraud.

The dispute landed at the Court after the Ninth Circuit ruled on September 3, 2025, that disgorgement of net profits plus prejudgment interest was proper. Sripetch filed his petition on October 14, 2025, the justices granted review on January 9, 2026, and oral argument was set for Monday, April 20, 2026. The question before the Court is whether the SEC may seek that remedy under 15 U.S.C. sections 78u(d)(5) and (d)(7) without proving direct monetary harm to investors.

The case builds on a line of Supreme Court decisions that have already narrowed SEC remedies. In Kokesh v. SEC, the Court held that disgorgement counts as a penalty for statute-of-limitations purposes. In Liu v. SEC, decided June 22, 2020, by an 8-1 vote, the Court said disgorgement can qualify as equitable relief only when it does not exceed net profits and is awarded for victims, not retained by the government. The Court noted in Liu that the award had been held in escrow and was at least partly available to compensate victims.

The stakes reach far beyond one defendant. The SEC said it obtained $8.2 billion in financial remedies in fiscal 2024, including $6.1 billion in disgorgement and prejudgment interest, and $17.9 billion in fiscal 2025, including $10.8 billion in disgorgement and prejudgment interest and $7.2 billion in civil penalties. The Second Circuit, in SEC v. Govil, required pecuniary harm for disgorgement under the relevant provisions, while the Ninth Circuit in Sripetch joined the First Circuit in holding that such harm is not required. If the Court narrows the tool further, defendants in cases ranging from bookkeeping violations to insider trading could keep more of what they gained; if the SEC prevails, regulators retain one of their sharpest weapons for stripping profits and discouraging repeat misconduct.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?