Textron reports stronger revenue, plans industrial spin-off to sharpen aerospace focus

Textron lifted first-quarter revenue 12% to $3.7 billion and said it will split off Industrial, turning toward a pure aerospace and defense story.

Textron is betting that Wall Street will reward simplicity. After reporting stronger first-quarter revenue and a $19.2 billion backlog, the Providence, Rhode Island-based manufacturer said it plans to separate its Industrial segment and recast itself as a pure-play aerospace and defense company built around Textron Aviation, Bell and Textron Systems.

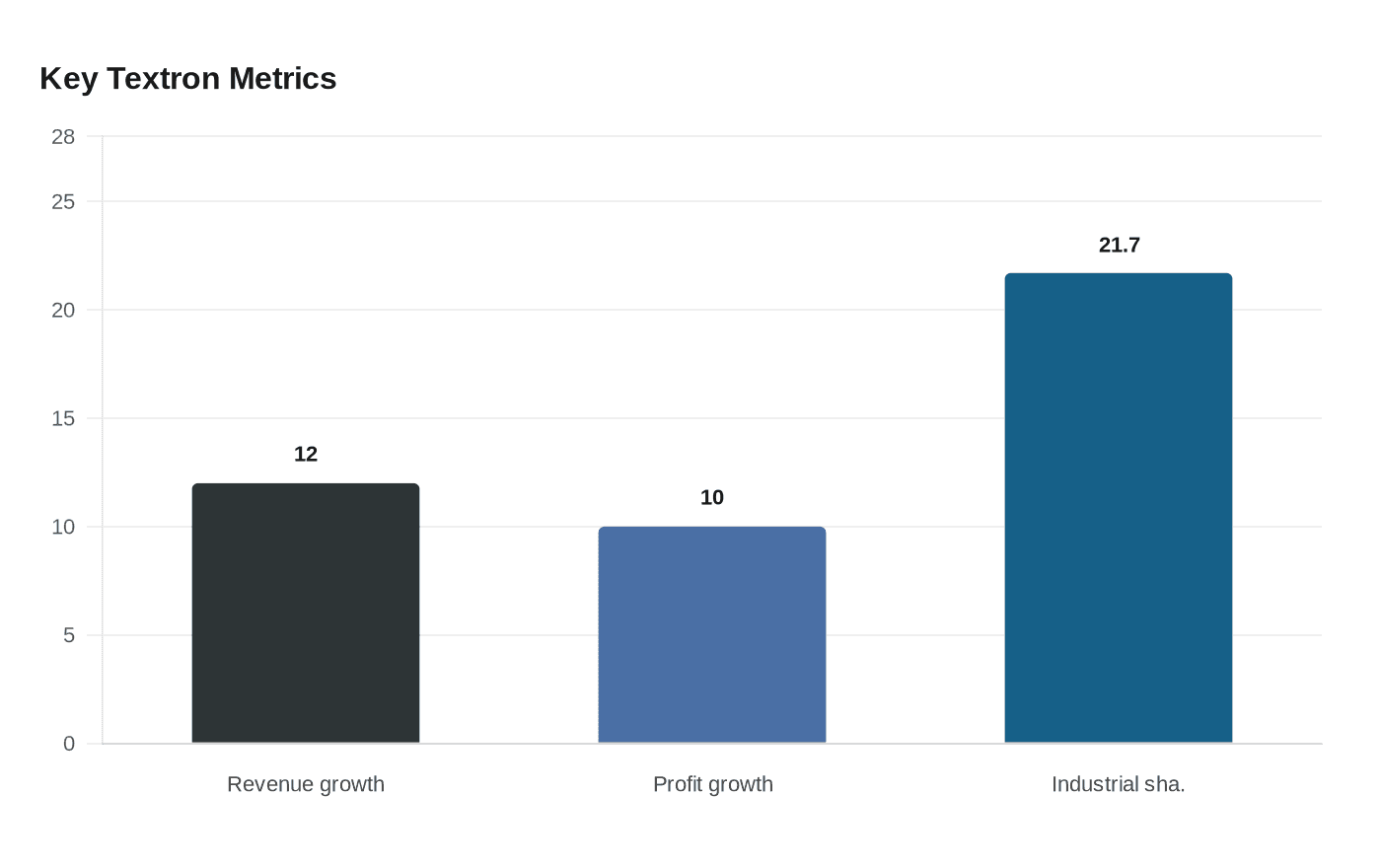

The numbers gave management cover to move. Textron said revenue rose 12% from a year earlier to $3.7 billion, with earnings of $1.25 a share and adjusted earnings of $1.45 a share. Segment profit increased 10% to $320 million, while company-wide backlog reached $19.2 billion. Management said that backlog would be entirely aerospace and defense backlog after the planned separation, reinforcing the case that the market may be able to value the remaining company more cleanly once Industrial is gone.

Industrial is not a side business. Textron said the unit, made up of Kautex and Textron Specialized Vehicles, has more than $3 billion in expected 2026 revenue. Kautex makes plastic fuel systems, battery enclosures and clear-vision systems for automotive customers, while Textron Specialized Vehicles sells golf cars, utility vehicles, powersports products, aviation ground support equipment and turf-care equipment. In Textron’s 2025 annual report, Industrial accounted for 21.7% of total revenue, showing the scale of the business that will be carved away.

Textron said it is weighing multiple paths, including a sale of the industrial businesses or a tax-free separation into a standalone public company. The company expects the process to take about 12 to 18 months. In investor materials, management said the post-separation Textron would have more than $12 billion in expected 2026 revenue and $19 billion in backlog, underscoring how central aerospace and defense already are to the remaining portfolio.

The move fits a broader corporate pattern: conglomerates under pressure to shed mixed industrial assets and narrow their focus around businesses with clearer demand drivers, stronger margins or more visible backlog. For Textron, the logic is that aviation and defense deserve to stand on their own, especially with commercial order activity strong at Textron Aviation and Bell. CEO Lisa M. Atherton said the separation would create “greater clarity and focus” for both businesses and unlock long-term value for stakeholders.

The quarter also showed the balancing act behind the strategy. Textron said manufacturing cash flow before pension contributions was a use of $228 million, and it returned $168 million to shareholders through buybacks. Investors now get a straightforward question: whether a leaner Textron, centered on aircraft, rotorcraft and defense systems, commands a better valuation than a diversified manufacturer tied to both aerospace cycles and more cyclical industrial demand.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?