Three June dates that could pull mortgage rates lower

June’s mortgage break will hinge on three data releases, not a lucky day on the calendar. The real question is whether inflation and jobs cool enough to push Treasury yields lower.

June 3: the Beige Book will show whether the economy is softening enough for rates to ease

Mortgage rates have already pushed higher in late May, with Freddie Mac showing the average 30-year fixed mortgage at 6.51% on May 21 and 6.53% on May 28, after 6.36% on May 14. The average 15-year fixed rate also moved up, from 5.85% to 5.87% over the same stretch. That is still below the 6.86% 30-year rate Freddie Mac reported a year earlier, but it is a reminder that borrowers are not dealing with a straight line, only a market that reacts quickly to new information.

The first June checkpoint is the Federal Reserve’s Beige Book on June 3, a regional snapshot of business conditions across the United States. It does not set mortgage rates directly, but it helps shape expectations for how the Fed sees growth, hiring, wages and pricing power. If the report suggests businesses are seeing weaker demand, softer hiring or less ability to raise prices, bond traders often read that as a sign that inflation pressures may cool, which can push Treasury yields lower and give mortgage rates room to follow.

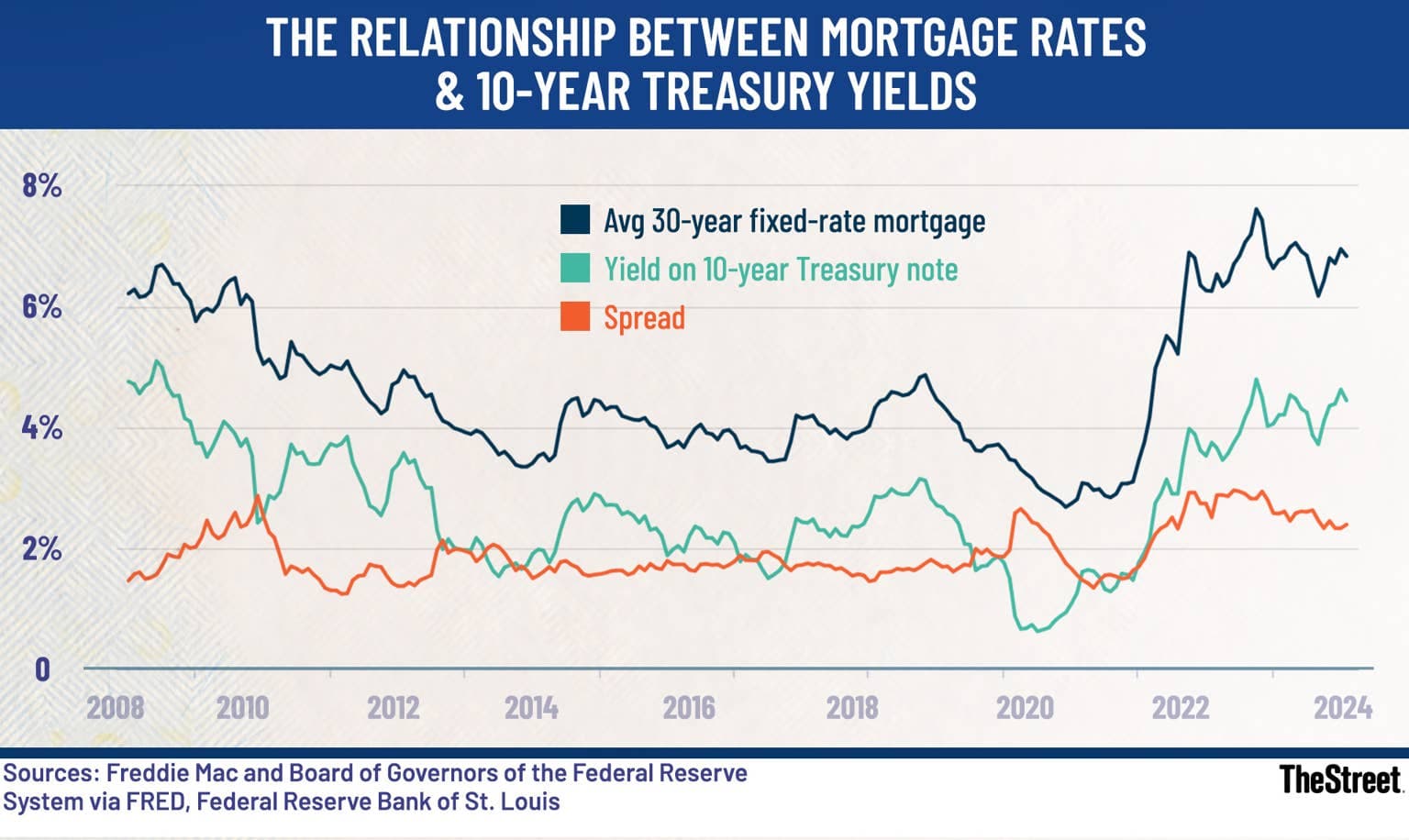

That connection matters because mortgage pricing is not driven only by the federal funds rate. It is also tied to the bond market, especially Treasury yields, and those yields move on expectations about inflation, labor costs and the Fed’s next steps. The Fed has already shown it is cautious in 2026, holding rates steady at its January, March and April meetings after starting to cut rates in September 2025, while pointing to low job gains, elevated inflation, little change in unemployment, higher energy prices and uncertainty tied to Middle East conflict. That combination has kept mortgage traders wary of assuming a fast decline.

For borrowers, the practical takeaway is simple: the Beige Book can hint at the direction of travel, but it is not a guaranteed trigger. A softer tone could help mortgage markets, yet a single report rarely resets rates for long unless it matches a broader slowdown already visible in other data.

June 5: the jobs report can move mortgage rates faster than almost anything else

The next key date is Friday, June 5, when the Bureau of Labor Statistics releases the Employment Situation report for May at 8:30 a.m. ET. This is often the most market-moving release of the month because payroll growth, unemployment and wages all feed directly into how investors price the likelihood of Fed cuts. A weak report can send Treasury yields lower within minutes, which often shows up in better mortgage pricing the same day or shortly after.

That is why borrowers watch the jobs report even if they are not economists. Strong job growth and firm wage gains usually suggest the economy can absorb higher rates, which can keep bond yields elevated. A softer report, especially if it shows slowing hiring or a cooler labor market without a sharp jump in unemployment, can do the opposite by reinforcing the view that the Fed has room to ease later in the year.

This year’s rate swings show how fast the market can change its mind. CBS News reported that the average 30-year mortgage rate started 2026 near 5.99% on January 2, fell to 5.75% on March 2, then climbed back to 6.37% by the end of March. That kind of movement underscores a basic truth for borrowers: the market does not reward patience in a straight line. It rewards timing only if the timing happens to coincide with a favorable data surprise, and that is hard to predict.

Freddie Mac’s chief economist, Sam Khater, has said borrowers should shop around and compare quotes because they can potentially save thousands. That advice becomes even more important around jobs day, when lenders may reprice quickly and different lenders may react at different speeds. You can prepare for the possibility of a better rate, but you cannot reliably control the exact hour it appears.

June 10 and 11: inflation data will decide whether any drop sticks

The most important test for a lasting move lower comes on Wednesday, June 10, when the BLS releases the Consumer Price Index for May at 8:30 a.m. ET, followed by the Producer Price Index on Thursday, June 11, also at 8:30 a.m. ET. These two reports matter because inflation is still the Fed’s central concern, and inflation is the piece of the puzzle most likely to keep mortgage rates elevated even when growth cools. If CPI and PPI come in softer than expected, bond traders are more likely to believe the Fed can keep cutting later in the year, which can pressure Treasury yields down and improve mortgage pricing.

That is also where the limits of timing become clear. Borrowers can position themselves around major data releases, but they cannot assume a good CPI report will lead to a lasting drop. Markets often move on the first reaction, then reverse if the details are less friendly than the headline. A cooler inflation number can help, but if it is followed by stronger spending, a firmer labor reading or a more hawkish Fed message, the relief can vanish fast.

The Federal Reserve’s June 16-17 FOMC meeting, followed by the press conference at 2:30 p.m. ET on June 17, is the next major checkpoint after those inflation numbers. By then, traders will have absorbed the Beige Book, the jobs report, CPI and PPI, and will use that stack of evidence to judge whether the Fed is likely to hold steady again or signal more confidence that inflation is easing. If the June data all lean softer, the bond market could move first and mortgage rates could follow. If they do not, the recent jump in rates may prove to be only a pause in a still-stubborn range.

Fannie Mae’s May 2026 Housing Forecast is a good reminder not to overread any one month. The company kept its 30-year mortgage-rate outlook at 6.3% through the first quarter of 2027, which suggests that even if June brings some relief, the bigger trend may still be a long slog rather than a sharp slide. For borrowers, that means the smartest move is not waiting for a perfect date. It is being ready when the data, the Fed and the bond market happen to line up at the same time.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?