Today's Mortgage Rates: What Homebuyers and Owners Need to Know

Mortgage rates dipped to 6.37% this week after five consecutive weeks of increases, but tariff-driven inflation fears and a frozen Fed could keep borrowing costs stubbornly elevated through summer.

Where Rates Stand Right Now

The average rate on a 30-year fixed mortgage sits at 6.37% as of this week, according to Freddie Mac, while the 15-year fixed averaged 5.74%. On a daily basis, Bankrate puts the current 30-year fixed rate slightly higher at 6.44%, with the benchmark 15-year fixed at 5.77% and the 5/1 adjustable-rate mortgage at 5.69%. For homeowners eyeing a refinance, the spread is wider: the average 30-year fixed refinance rate stands at 6.69%.

Freddie Mac's primary benchmark averaged 6.46% for the week ending April 2, making this week's easing the first reprieve after five straight weeks of increases. Rates are now half a percentage point higher than a month ago. The small dip is welcome but doesn't change the fundamental picture: borrowing remains meaningfully more expensive than it was just weeks ago.

What's Driving Rates This Week

Three overlapping forces are keeping mortgage rates elevated and volatile.

The 10-year U.S. Treasury yield, which banks use as a guide to pricing home loans, was at 4.28% in midday trading Thursday. Average mortgage rates are usually about 1.8 percentage points higher than the yield on the 10-year note, and in times of economic uncertainty, such as periods of high inflation, Treasury yields tend to rise. That arithmetic explains much of where rates are today.

The Federal Reserve's posture is the second major variable. A growing number of FOMC members now expect no cuts, or at most one, to the federal funds target this year, largely due to a more persistent inflation outlook. The median FOMC member also expects higher inflation in 2026. Core PCE inflation, the Fed's preferred measure, is at 2.6% as of March 2026, down from 3.5% a year ago but still above the 2% target.

Tariffs are the third and least predictable factor. Tariffs on imports announced in early 2026 could add 0.3 to 0.5 percentage points to inflation, potentially delaying further rate cuts. If inflation stalls above 2.5%, expect rates to stay in the 5.80-6.20% range longer. The sharp rise in energy costs sparked concerns about inflation, and bonds historically perform poorly amid rising inflationary pressures. Compounding the pressure were weak Treasury auctions throughout recent weeks, as soft demand forces investors to demand higher yields to absorb the supply.

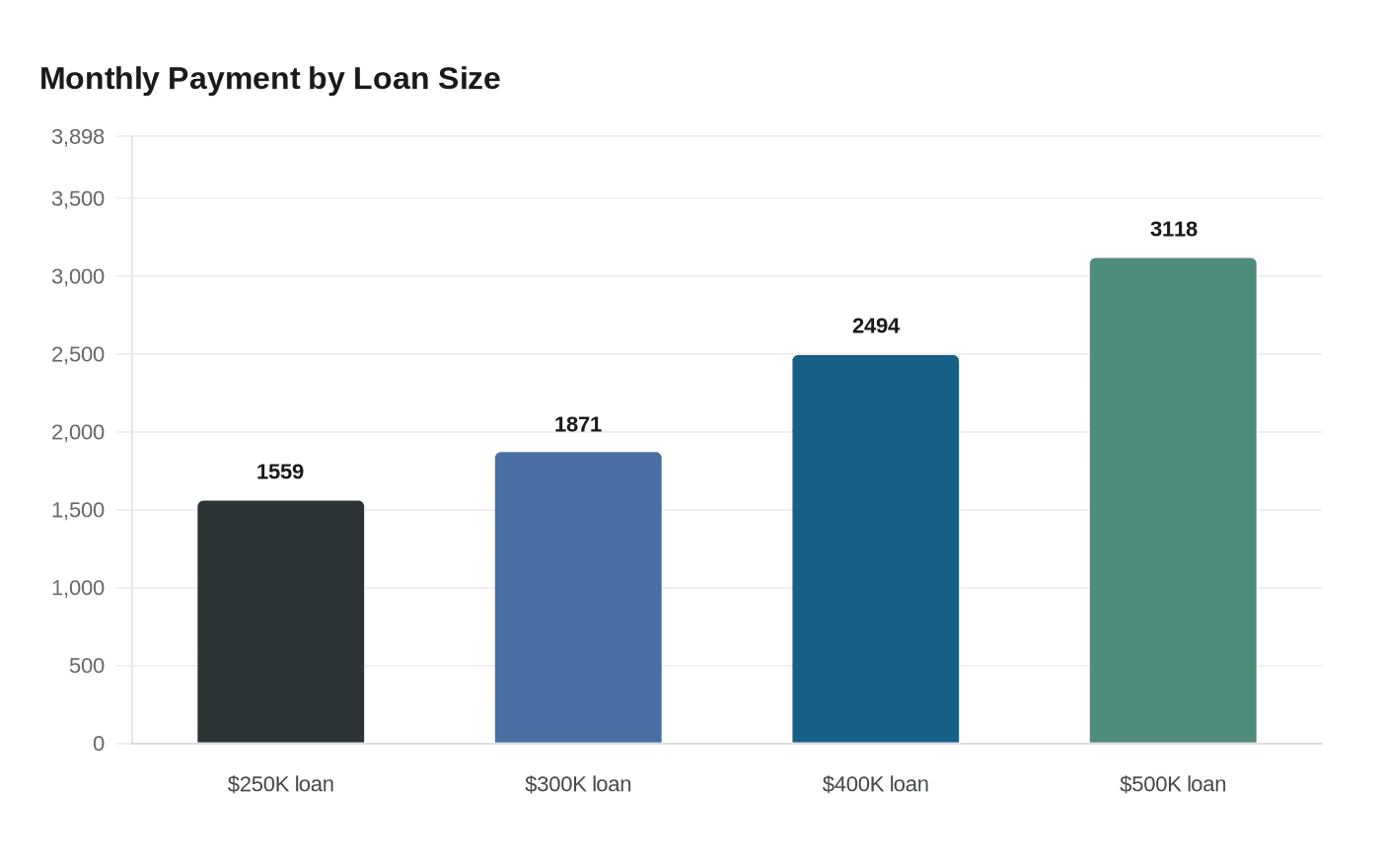

What These Rates Mean for Your Monthly Payment

Translating today's benchmark rate into real dollars clarifies the stakes. At the current Freddie Mac average of 6.37% on a 30-year fixed loan, monthly principal and interest payments break down as follows (taxes and insurance not included):

- $250,000 loan: approximately $1,559 per month

- $300,000 loan: approximately $1,871 per month

- $400,000 loan: approximately $2,494 per month

- $500,000 loan: approximately $3,118 per month

Choosing a 15-year fixed at 5.74% compresses the repayment window but raises the monthly obligation significantly. On a $300,000 loan, that means roughly $2,490 per month versus $1,871 on the 30-year equivalent. The tradeoff is substantial long-term interest savings and faster equity accumulation, making the 15-year option most compelling for buyers who can comfortably absorb the higher payment.

Adjustable-rate mortgages sometimes start lower than fixed rates, but once the initial rate-lock period ends, you risk your interest rate going up. ARM rates have also been starting higher than fixed rates recently, so you may not always get a rate break. In today's environment, the 5/1 ARM at 5.69% offers only modest savings over a 30-year fixed, reducing the case for taking on that variable risk.

The Refinancing Math: Break-Even Before You Sign

As of the third quarter of 2024, 82.8% of homeowners with mortgages had rates below 6%, according to a Redfin report. That means a significant chunk of homeowners have been locked in, unwilling or unable to move or refinance with rates as high as they currently are. For those who took out loans during the rate surge of 2023 and 2024, however, the window for meaningful relief is opening.

Refinancing closing costs typically run 2 to 6% of the loan amount. One commonly cited guideline is that it makes sense to refinance if you can secure a rate at least a percentage point lower than your current rate. The math on a $300,000 loan illustrates why that threshold matters: refinancing from 7% down to 6.37% saves approximately $125 per month, but with closing costs of $6,000 to $9,000, the break-even point falls between 48 and 72 months, or four to six years. Push the rate drop to a full percentage point, from 7.37% to 6.37%, and monthly savings jump to roughly $200 on a $300,000 loan, cutting that break-even to around 37 months, closer to three years.

Real estate platform Redfin is forecasting that U.S. mortgage refinance volume may increase by more than 30% in 2026 compared to the previous year. When refinancing volume rises sharply, lenders get busier, processing times lengthen, and the most competitive rates can disappear faster. If the numbers work for you today, delay carries its own cost.

The Rate Outlook: What Forecasters Expect

Most forecasters have converged around 6% to 6.3% as the likely range for 2026, and I expect rates to stay in a relatively similar range as where they ended in March, hovering in the low-to-mid 6% range. The swing factor remains the Fed's pace of easing. Markets currently price a 72% probability of a 0.25% Fed rate cut at the June 17-18, 2026 FOMC meeting, which would drop the federal funds rate from 4.50% to 4.25%.

The 30-year fixed could hit 5.50-5.90% by August if two to three Fed cuts materialize. However, if inflation rebounds above 3% or tariff impacts worsen, rates could stay in the 5.90-6.20% range. Powell's term ends in May, adding another layer of uncertainty: with a leadership transition on the horizon, the Fed is unlikely to make any bold moves in the near term.

Who Should Lock Now vs. Who Should Wait

The decision to lock a rate today versus floating while waiting for a better number depends almost entirely on your specific situation, timeline, and current rate.

- You are closing within 60 days and your rate is below 6.20%, which represents solid value by historical norms

- If your rate is below 6.0%, that is already excellent by today's standards and the risk of waiting outweighs the potential upside

- You locked in a mortgage at 7% or higher and can clear the break-even on refinancing within your expected stay in the home

- You are concerned about volatility; with uncertainty likely to persist through 2026, protecting yourself from rate increases through a well-timed rate lock remains one of the most valuable actions you can take in a mortgage transaction

Lock now if:

- You currently hold a rate below 6% and the math on refinancing costs doesn't close within a reasonable break-even window

- Your home purchase timeline extends beyond 90 days and Fed cut probability improves through summer data releases on inflation and employment

- A disciplined approach is to set a target rate, such as 0.75% below your current rate, and lock in immediately if rates reach that level, rather than giving in to the urge to wait for small incremental improvements

Consider waiting if:

Waiting to buy a home can increase costs over time and reduce potential equity gains, and while interest rates may be higher than you'd prefer, the rate you purchase your home at doesn't always have to be the rate you keep long term. Rates in the mid-6% range, while nothing like the pandemic-era lows, are squarely within the historical norm, and building equity now while monitoring the trajectory toward potential summer cuts is a defensible strategy for buyers who are financially ready to move.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?