Trump Fed pick Warsh backs shrinking central bank balance sheet

Kevin Warsh wants a smaller Fed balance sheet, a move that could ripple into mortgages, Treasury yields and bank liquidity before the next crisis hits.

Kevin Warsh is pushing the Federal Reserve toward a smaller footprint in markets, a shift that could reach from mortgage rates to Treasury financing costs and the amount of liquidity banks keep on hand. The former Fed governor, now President Donald Trump’s nominee to lead the central bank, told the Senate Banking Committee on April 21 that he would work with the Treasury Department to shrink the Fed’s balance sheet, which he says has become too large and too routine a force in financial markets.

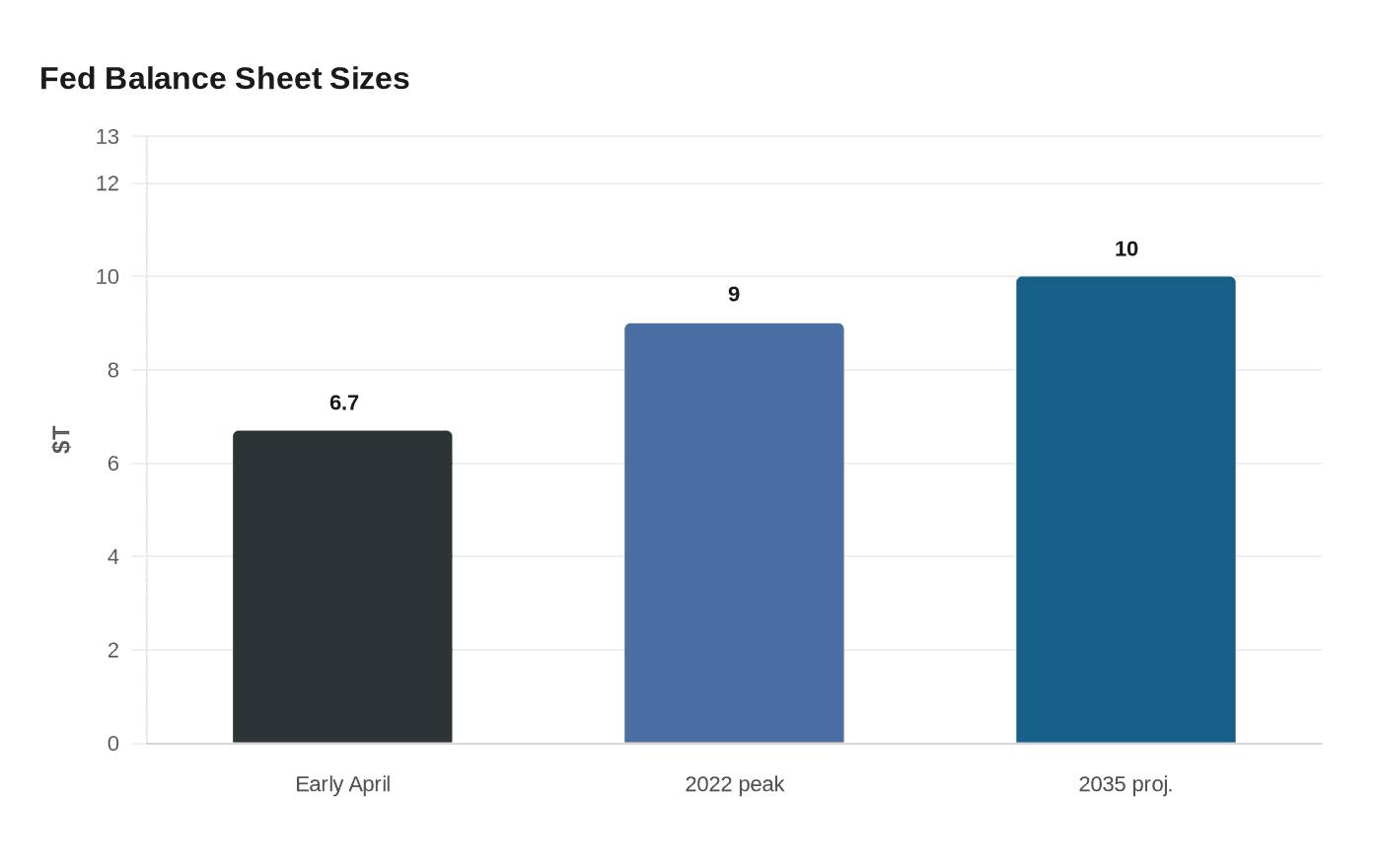

The stakes are not abstract. The Fed’s assets stood at about $6.7 trillion in early April, after the central bank ended balance-sheet runoff in December and began modest reserve-management purchases in mid-December to offset temporary liquidity drains. That is far below the roughly $9 trillion peak reached in 2022, but still far above the under-$1 trillion level that existed before the 2007 financial crisis. A New York Fed projection cited by Reuters suggests holdings could climb to $10 trillion by the end of 2035 if technical factors are left to play out.

Warsh’s argument is that the Fed’s holdings tilt the system toward Wall Street and away from Main Street, while also forcing the central bank to keep short-term rates higher than otherwise. He said any change should be done “slowly and deliberately,” and he drew a line between the financial crisis, when large-scale bond buying was widely seen as justified, and more recent rounds of heavy intervention that he views as harder to defend.

For the real economy, a smaller balance sheet would likely mean fewer Fed purchases of Treasuries and mortgage-backed securities, which could put upward pressure on bond yields and, by extension, mortgage rates. It could also mean less excess liquidity sitting in the banking system, which may make money-market rates more sensitive and tighten the Fed’s control over its policy target if reserves fall too far. That is the practical trade-off behind an abstract debate about “footprint” and “ample reserves.”

There is growing support for some shrinkage, but only if the plumbing holds. Dallas Fed President Lorie Logan said on April 2 that the Fed has paths and options to reduce the balance sheet while preserving financial stability. In a recent paper, Fed Governor Stephen Miran argued the Fed’s $6.68 trillion in assets could be cut by as much as $2 trillion through changes to liquidity rules, stress testing and the use of existing lending tools. Analysts at Wrightson ICAP have said there is widespread agreement that reserve demand can be reduced through regulation.

The institutional question is sharper still because Jerome Powell’s term as Fed chair ends on May 15, while his Board term runs until January 2028. Warsh’s hearing signaled that the next chair could inherit not just the challenge of managing interest rates, but a broader fight over whether the post-2008, and then post-pandemic, model of an activist central bank should give way to a smaller and more restrained one.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?