Under Armour warns annual revenue will fall amid weak consumer demand

Under Armour warned revenue will dip again, with North America sales down 7% and Wall Street bracing for earnings far below estimates.

Under Armour is still losing ground in its biggest market, and the message to investors was blunt: sales are likely to fall again this year. The Baltimore-based company said fiscal 2027 revenue would decline slightly after posting a 1% drop to $1.2 billion in the fiscal fourth quarter, a sign that weak consumer demand and intense competition are still squeezing the brand.

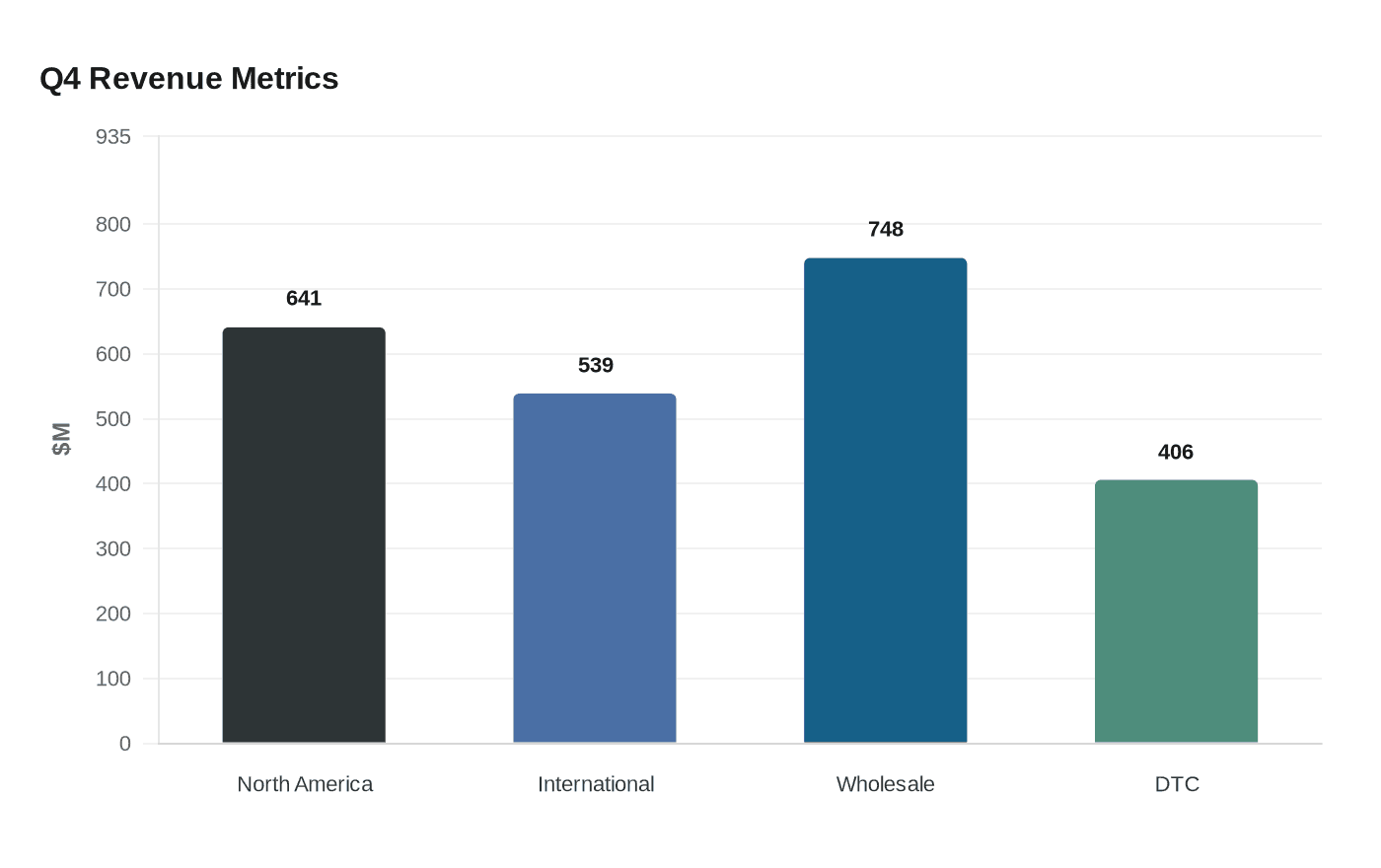

The clearest pressure point was North America, where revenue fell 7% in the quarter to $641 million. International business was stronger, rising 10% to $539 million, but that growth was not enough to offset the softness at home. Wholesale revenue slipped 3% to $748 million, while direct-to-consumer revenue rose 5% to $406 million, showing that Under Armour is still leaning on its own channels even as retail partners remain cautious.

The company’s gross margin fell 470 basis points to 42.0%, hit by higher tariffs, higher product costs, pricing headwinds and an unfavorable regional mix. Under Armour posted a net loss of $43.4 million in the quarter, and the full-year picture remains difficult: the company has now reported sales declines for three straight years, including a 9% drop in fiscal 2025 revenue to about $5.16 billion.

Chief executive Kevin Plank, who returned to the role effective April 1, 2024, said Under Armour is taking "intentional steps" to reset the business, streamline operations and rebuild its marketing capabilities. He has also said the company is trimming about 25% of product lines and shifting toward higher-priced performance categories such as training, running and team sports, an attempt to restore pricing power and sharpen the brand against rivals with broader reach and stronger momentum.

That strategy is being tested in a consumer environment where shoppers are selective and easily delay discretionary purchases. Under Armour’s latest guidance points to adjusted operating income of $140 million to $160 million in fiscal 2027, including about $70 million in possible tariff refunds and a roughly $35 million hit tied to the conflict in the Middle East. Reuters also reported that adjusted earnings per share are expected to be 8 cents to 12 cents, below analysts’ average estimate of 23 cents, while revenue is projected to slip versus expectations for a 1.6% increase to about $5.05 billion.

The results suggest Under Armour’s problem is not just a broad retail slowdown. Weak North American demand, falling wholesale sales and persistent margin pressure point to a brand-specific struggle to regain traction, even as the company’s international business holds up better. A May 11 research and development collaboration with Persona AI, aimed at advanced performance materials for humanoid robotics, underscored the company’s materials expertise, but the core athletic apparel business remains under pressure.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?