UnitedHealth forecast edges past estimates as insurers slide

UnitedHealth sees 2026 adjusted EPS just above analyst consensus; insurers fall after a modest Medicare Advantage rate proposal, underscoring policy risk to profits.

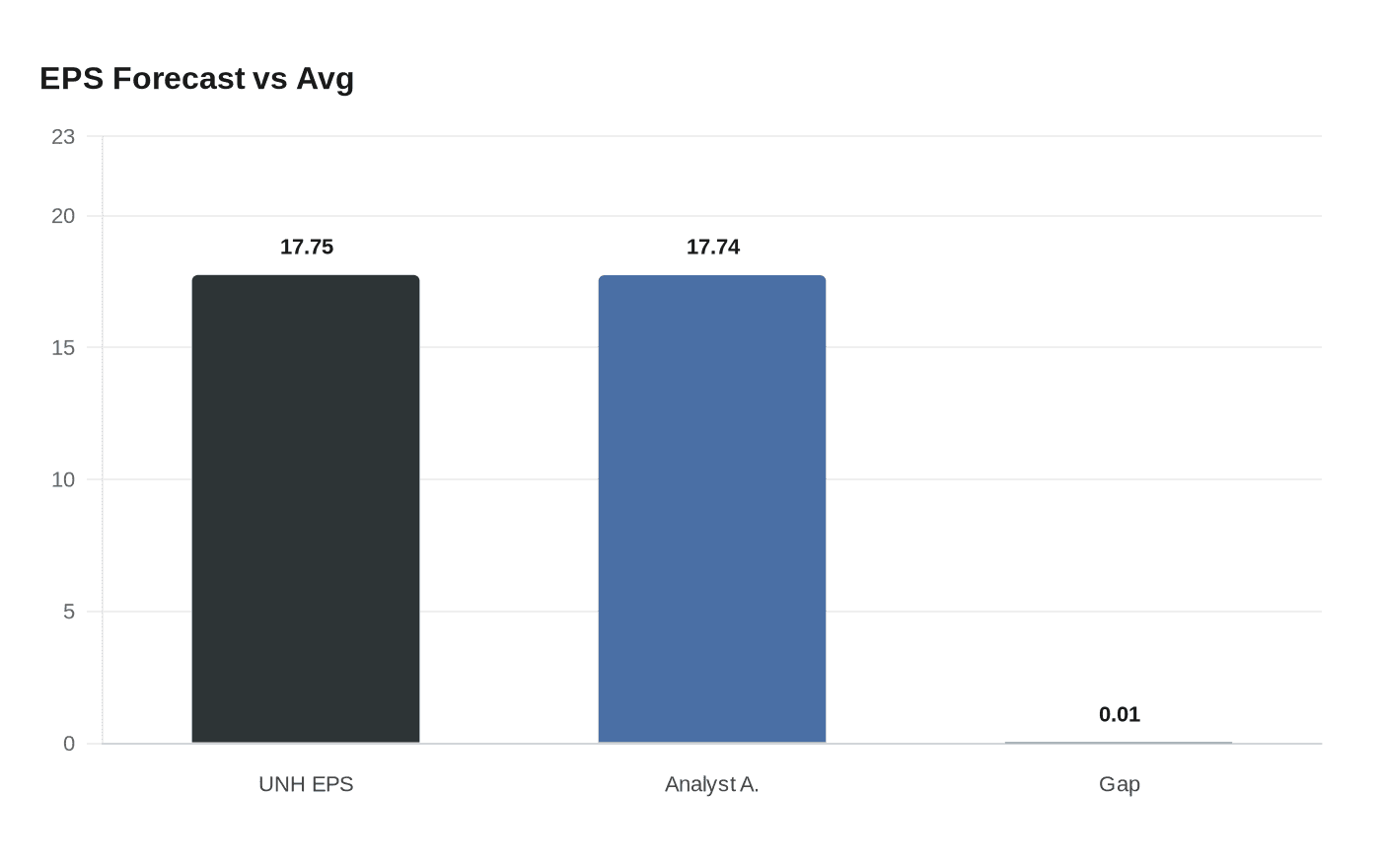

UnitedHealth Group on Tuesday forecast adjusted earnings per share for 2026 slightly above the Street, projecting annual profit per share at more than $17.75 compared with the LSEG analyst average of about $17.74. The company framed the projection as modestly ahead of consensus, but the move failed to reassure markets after regulators proposed only a small increase in Medicare Advantage rates, sending insurer stocks lower in trading.

The narrow gap between UnitedHealth’s outlook and analysts’ expectations, effectively a penny or so, highlights how finely balanced investor sentiment has become for large health insurers. UnitedHealth remains the sector’s bellwether by revenue and membership, and its guidance is scrutinized for signs of premium pricing power, medical cost trajectory, and the durability of Medicare Advantage margins. The company’s forecast implies management expects underlying revenue and cost trends to broadly offset each other next year, but it leaves little margin for unexpected policy or utilization shifts.

The regulator’s Medicare Advantage rate proposal is the immediate catalyst for the market move. Insurers derive an outsized share of government-paid business from Medicare Advantage plans, which bundle premiums and payments tied to beneficiary risk scores and service use. A smaller-than-expected rate increase reduces the growth runway for plan revenue and can compress margins, particularly for carriers that leaned on favorable rate adjustments to fund supplemental benefits and broker commissions in recent years.

For investors, the episode underlines policy sensitivity in an industry where a few percentage points in rate setting alter earnings estimates materially. Analysts and portfolio managers will now be recalibrating assumptions about 2026 margin expansion, reserve needs, and the willingness of carriers to shift benefits or premiums in response. Insurers also face nonprice pressures such as utilization growth from new therapies and the continuing shift of older Medicare beneficiaries into Advantage plans, factors that complicate forecasting.

From a policy perspective, a cautious rate proposal signals regulators’ balancing act between limiting federal spending growth and ensuring adequate plan payments to maintain access and benefits. It may also reflect tighter scrutiny on risk adjustment practices or a desire to curb aggressive supplemental benefit offerings that can raise costs. For incumbents, the response options are limited: narrow networks, reduce nonessential supplemental benefits, increase premiums for certain segments, or pursue further efficiency gains in care management and provider contracting.

Longer-term, the health insurance sector confronts structural trends that amplify the importance of such rate decisions. Medicare Advantage enrollment has grown steadily over the past decade, making federal payment policy an ever-larger determinant of revenue mix. Simultaneously, medical cost inflation and adoption of costly specialty therapies pose ongoing margin risks. The interplay of regulatory settings, care delivery innovations, and demographic shifts will shape carriers’ strategic choices and investors’ valuations over the coming years.

UnitedHealth’s near-consensus guidance and the market’s negative reaction to a modest regulatory proposal together underscore the thin buffer insurers now carry against policy shocks. For markets and policymakers alike, the episode is a reminder that even incremental changes in public program rates can ripple through corporate earnings and patient-facing benefits.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?