US household debt hits record highs, raising growth risks

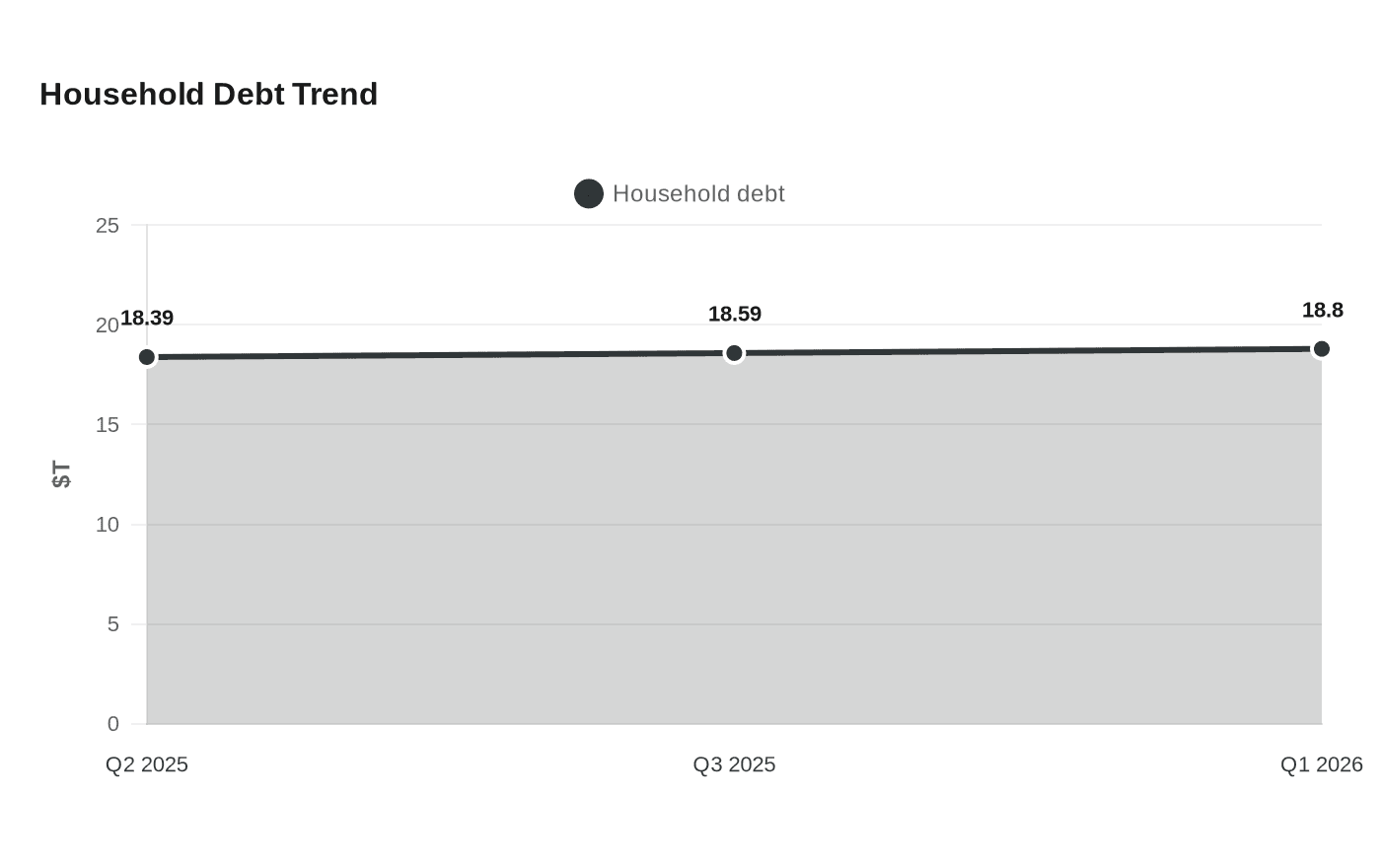

US household debt climbed to $18.8 trillion in early 2026, while the economy needed more borrowing than at any point in at least 70 years to generate growth.

Household debt is still rising faster than the economy’s ability to comfortably absorb it, and that is turning family balance sheets into a growing drag on U.S. growth. The New York Fed said total household debt reached $18.8 trillion in the first quarter of 2026, after standing at $18.59 trillion in the third quarter of 2025. Mortgage balances alone totaled $13.19 trillion at the end of March, underscoring how much of the household sector is tied to housing leverage.

The latest numbers show strain, but not yet a broad crack. Household debt rose by $18 billion, or 0.1%, in the first quarter of 2026, and the New York Fed said delinquency transitions were mostly steady. Auto-loan early delinquency held steady, while credit-card and mortgage early delinquency ticked down. Even so, serious mortgage delinquency edged higher, from 1.4% to 1.5%, a reminder that the weakest borrowers are still under pressure even as the aggregate picture looks calm.

That calm sits on top of a much larger climb in borrowing since the pandemic recession. The New York Fed said household debt was up $4.24 trillion from the end of 2019 in its second-quarter 2025 report, after balances rose by $185 billion to $18.39 trillion. By the third quarter of 2025, debt had climbed again, to $18.59 trillion. The pace is slower than the surge that followed the pandemic, but the stock of debt is now so large that even modest deterioration in repayment can matter for the broader economy.

Societe Generale’s warning goes to the heart of that risk. The bank said the credit intensity of GDP, a measure of how much debt is needed to produce a given unit of growth, rose to 3.73 last year, the highest level in at least 70 years. In practical terms, that means the U.S. economy is leaning more heavily on borrowing to keep spending moving, even as families are already stretched across mortgages, auto loans, credit cards and student debt.

That mix is dangerous because household leverage usually holds up consumption until it does not. Families under the most stress tend to cut discretionary spending first, then delay big-ticket purchases, and eventually fall behind on payments if income weakens or rates stay elevated. With mortgage debt at a record high and serious mortgage delinquency edging up, the clearest warning sign is not a collapse yet but a system that is becoming less resilient. If borrowing slows while debt-service burdens stay high, the slowdown will not begin in corporate boardrooms. It will start in household budgets.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip