Warsh debuts as Fed chair, holds rates steady in unanimous vote

Warsh's first Fed meeting left rates unchanged at 3.5% to 3.75%, but his vows to listen and his new task forces hinted at a possible reset.

Kevin Warsh’s first meeting as Federal Reserve chair did not deliver a break from the central bank’s recent posture. Households and markets got the same near-term message they have heard for months: no rate cut, no dissent, and no sign that the Fed was ready to rush into easing.

The Federal Open Market Committee kept its target range for the federal funds rate at 3-1/2 to 3-3/4 percent in a unanimous 12-0 vote at its June 16-17 meeting, Warsh’s first as chair. The Board of Governors also left the interest rate paid on reserve balances at 3.65 percent, effective June 18, and the committee reaffirmed its ample-reserves framework. For borrowers, that means mortgages, auto loans and other credit costs are likely to stay anchored near current levels unless the Fed later shifts its stance.

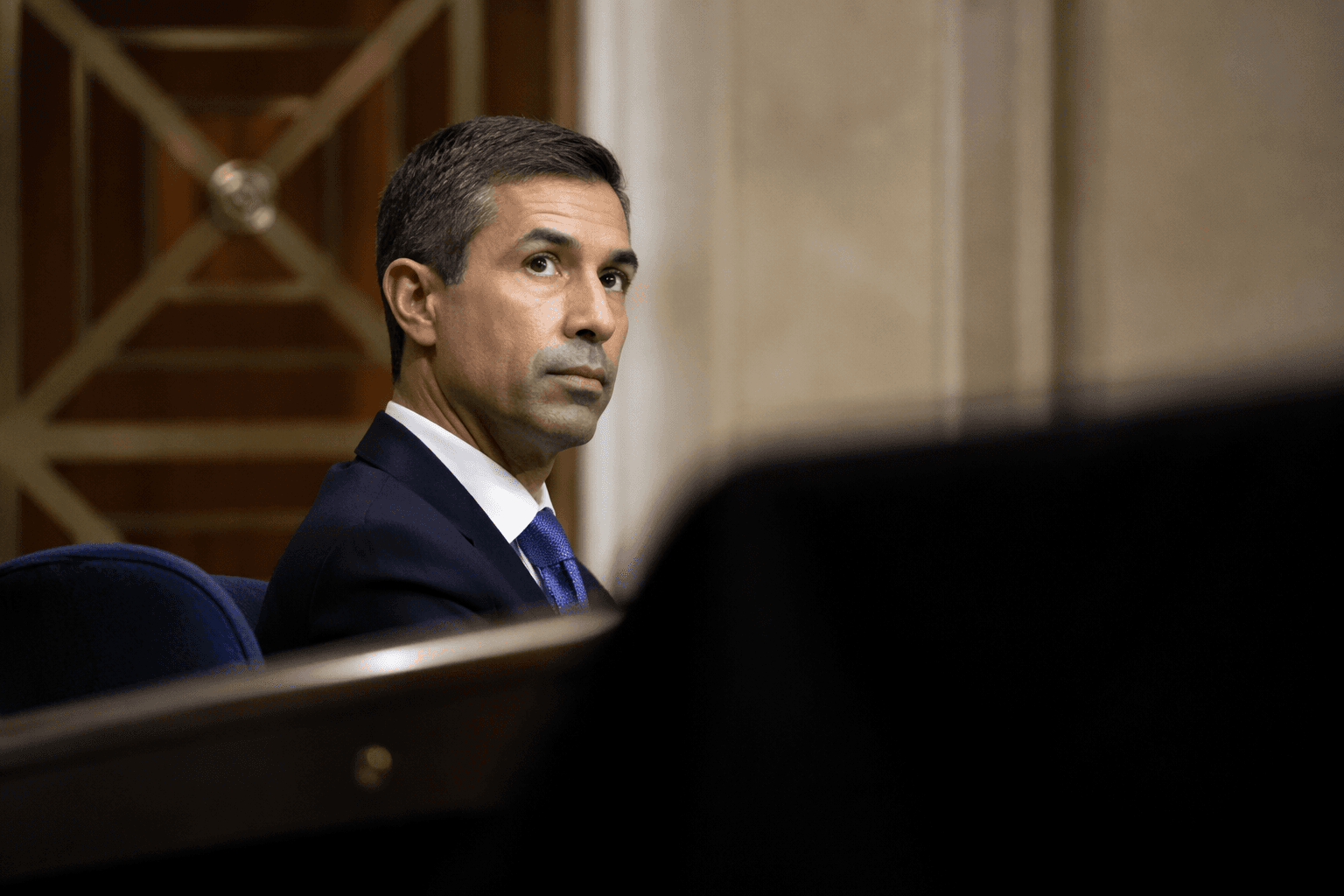

Warsh, who took office as chair on May 22 after being nominated by President Donald J. Trump on March 4 and confirmed by the Senate on May 12 to the Board and on May 13 as chairman, used his opening press conference to project continuity rather than confrontation. He said it was an honor to be back at the Fed, said he had been heartened by the welcome from colleagues and said he had listened closely to fellow FOMC members. The June meeting also came with the Summary of Economic Projections, the document investors will parse for clues on whether officials still see room for rate cuts later in 2026.

That matters because this was not just any policy meeting. The Fed holds eight regularly scheduled meetings a year, and the minutes of those meetings are released three weeks later, so the June gathering was the first real test of how Warsh will communicate after a leadership change that had been heavily politicized by Trump’s repeated demands for lower rates and attacks on Jerome H. Powell. Investors had been watching closely for any sign that Warsh would soften the Fed’s resistance to political pressure or change its emphasis on inflation and employment.

So far, the answer looks closer to stewardship than rupture. Warsh’s first meeting did not change the policy rate, but it did show where he may try to make his mark: not through a surprise cut, but through process. He announced five task forces to overhaul Fed operations, including work on monetary policy conduct and the effects of artificial intelligence, signaling that the early Warsh era may be defined as much by institutional redesign as by interest-rate decisions.

For households, the practical takeaway is straightforward. If inflation remains elevated and the labor market cools only gradually, the Fed is still more likely to keep borrowing costs restrictive than to deliver rapid relief. That keeps recession risk in the conversation, but it also suggests Warsh’s opening did not yet produce a decisive shift in the Fed’s outlook on prices, jobs or the timing of easier policy.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?