Weinstein Closes In on SpaceX Win Against Baillie Gifford at Edinburgh Worldwide

Weinstein's Saba Capital, holding 30% of Edinburgh Worldwide, stands on the verge of replacing a board whose own manager admits control is slipping away.

Boaz Weinstein's Saba Capital Management appeared poised for a landmark activist victory as Edinburgh Worldwide Investment Trust's manager, Baillie Gifford, acknowledged in its own tender offer materials that the hedge fund was on the verge of prevailing at a shareholder meeting set for April 10.

The concession underscored how dramatically the balance of power had shifted over roughly 18 months of confrontation. Saba holds roughly 30% of the London-listed trust, making it the dominant shareholder in a portfolio spanning approximately $1 billion in assets, with SpaceX stock alone accounting for about 17% of net asset value.

The dispute ran through a bruising series of votes. In January 2026, shareholders backed the incumbent board for the second time in less than a year, with Chair Jonathan Simpson-Dent calling Saba's campaign a "significant and costly distraction." Weinstein then accused the board of allowing Baillie Gifford to sell EWI's SpaceX stake roughly two months before SpaceX's valuation doubled, a move he estimated cost shareholders £37 million in foregone gains, describing SpaceX as "the crown jewel of the Company's portfolio."

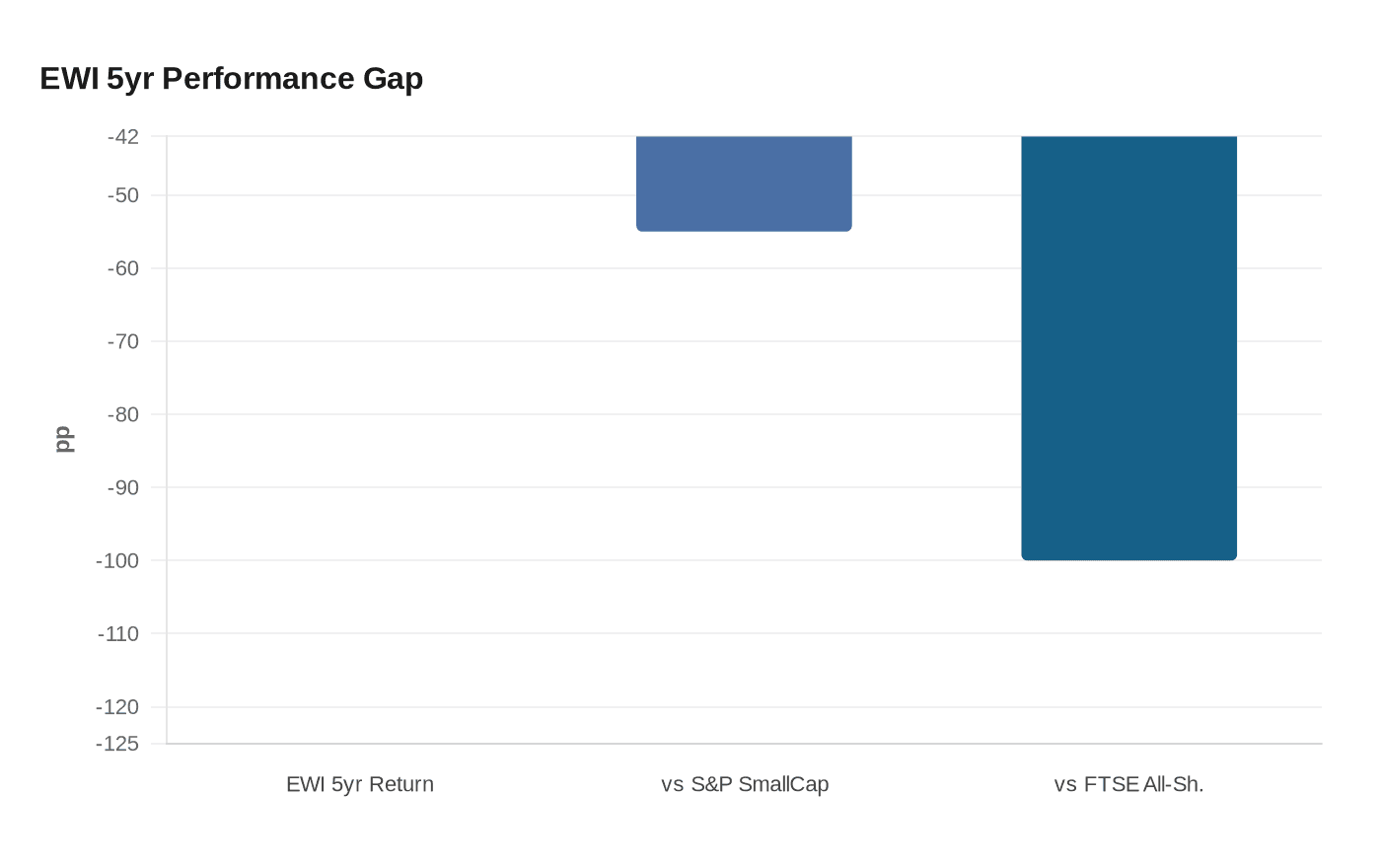

The performance case sharpened the indictment. Saba disclosed that Edinburgh Worldwide lost approximately 34% of its value over the preceding five years, underperforming the S&P Global SmallCap Price Index by 55 percentage points and the FTSE All-Share Total Return by a full 100 percentage points over the same stretch.

Unable to reach a negotiated resolution, the board announced on March 10 a 100% cash tender offer. Under the proposal, tendering shareholders would receive approximately 85% of their position in cash at close to NAV upfront, with roughly 15% deferred into escrow pending crystallization of the SpaceX position through an IPO or another liquidity event. Market commentary has pointed to a possible SpaceX offering as early as June 2026, a listing that would dissolve the trust's primary rationale for holding an illiquid private stake.

The mechanics of board composition matter as much as the headline cash number. Directors control fee structures, buyback programs, and disclosure depth. A Saba-aligned board would hold direct authority over those levers in ways no activist letter campaign can replicate. Saba is also backing three nominees at the April 10 annual meeting, framing the vote as a choice between two competing governance models.

For U.S. retail investors who access private-company exposure through listed investment vehicles, the Edinburgh Worldwide dispute makes legible a familiar set of risks: a single dominant holding can distort stated returns, compress diversification, and leave shareholders dependent on a board's judgment about when to sell at prices not set by the market. Capital-gains tax implications from forced asset sales add further complexity for anyone weighing an exit.

The voting deadline fell on April 8, with some platform-dependent shareholders required to act as early as March 30. Either outcome at the April 10 meeting will establish a reference point for how closed-end trusts navigate the stretch between peak private valuations and the pricing clarity that only a public listing can provide.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?