Western critical minerals push risks oversupply and price collapse

Governments are racing to break China’s mineral grip, but the subsidy rush could trigger the next glut and price crash.

A policy race that could sow the next glut

Western governments have turned critical minerals into a strategic industrial project, pouring tens of billions of dollars into mining, refining and stockpiling in an effort to reduce dependence on China. The problem is that a scramble to build non-China supply chains can create the very oversupply policymakers want to avoid, especially if countries subsidize the same materials at the same time and each tries to build its own reserve.

That is the central warning from Reuters’ analysis: good intentions can backfire when industrial policy is fragmented. If governments act separately, they can finance too many mines, too much processing capacity and too much inventory, then discover that prices have fallen before demand has caught up.

The scale of the spending spree

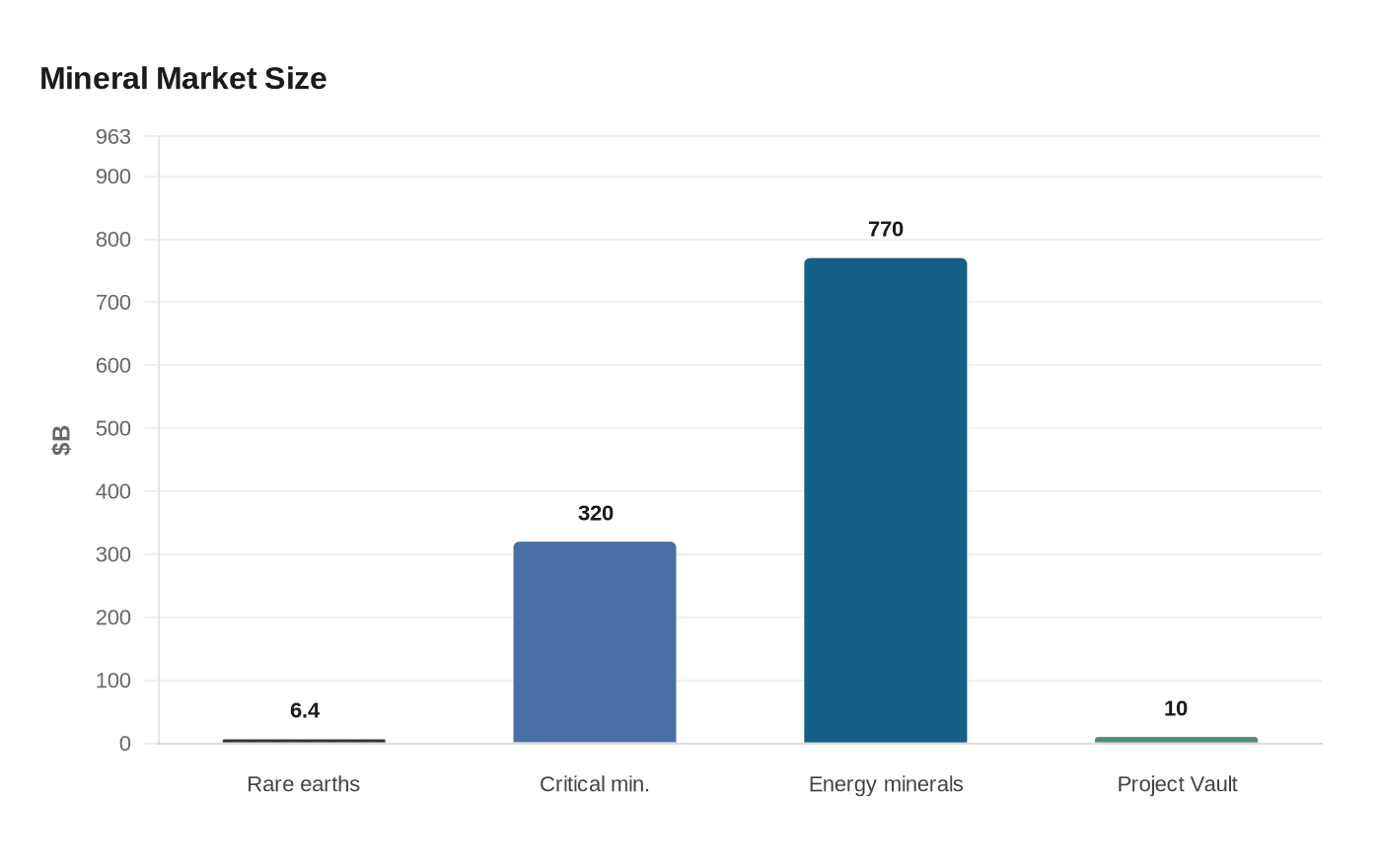

The United States has allocated more than $20 billion to support its critical minerals sector through multiple programs and financing tools. A major part of that push is Project Vault, a $10 billion strategic stockpile effort tied to U.S. critical minerals policy. The Export-Import Bank of the United States said in February 2026 that it approved a Project Vault loan to launch America’s Strategic Critical Minerals Reserve.

Australia has also moved aggressively, earmarking at least A$13 billion across at least five programs, including its own reserve. In October 2025, the United States and Australia advanced a critical minerals framework under which each side took measures to provide at least $1 billion in financing to key projects within six months. Taken together, the message from Washington and Canberra is clear: building secure supply chains has become an industrial priority, not a niche mining issue.

That spending wave is not confined to one alliance. Reuters reported that pledged support from the United States, the European Union, Australia and Japan for rare earths projects worldwide already exceeds the sector’s current market value. When public support outgrows the market it is meant to stabilize, the risk is no longer underinvestment. It is overbuild.

Why rare earths matter, even in a small market

Rare earths sit at the center of the story because they are strategically important even though the market is small. Reuters says the materials are used in defense technologies, advanced manufacturing and medical equipment, which is why governments are treating them as a security asset as much as a commercial one.

The numbers show the mismatch. The broader critical minerals market is about $320 billion and could double by 2040, according to International Energy Agency figures cited by Reuters. Yet the rare earths market itself was only about $6.4 billion in 2024. The IEA also says the combined market value of key energy transition minerals could more than double to $770 billion by 2040 in its NZE scenario.

That gap matters because it explains how price crashes happen. A market may look enormous in strategic terms, but if the tradable segment is still relatively small, a wave of new projects can overwhelm demand. Rare earths are the clearest example of a sector where policy ambition could outrun the market’s ability to absorb new supply.

What past commodity busts warn about

The danger is not hypothetical. Industry executives, investors and analysts told Reuters that the current push risks repeating the logic of the old butter mountains and aluminium floods, when government intervention produced gluts rather than resilience. In the 1980s and early 1990s, subsidies, cheap energy and price guarantees helped drive massive overproduction in European dairy and other commodities, pushing prices down and spreading pain far beyond the countries that created the policies.

The historical lesson is simple: price support can encourage more output than the world can use. Once capacity is built, it rarely disappears quickly. Producers keep operating to service debt, governments hesitate to reverse subsidies, and the market ends up carrying the burden through lower prices, weaker returns and stranded assets.

That is why the current critical minerals boom carries such obvious echoes. If governments all do their own thing, create multiples of the volumes the world actually needs and then rush to secure national stockpiles, the result can be a race to the bottom in prices. The pressure would not stop at mine sites. It would hit processors, equipment makers, investors and taxpayers who helped pay for the expansion.

Where overbuilding looks most likely

The highest risk sits in rare earths, precisely because the market is small, strategically sensitive and already attracting heavy public backing. When pledged support exceeds current market value, the odds rise that some projects will be funded for geopolitical reasons long before they can compete on commercial terms.

The broader basket of key energy transition minerals also looks vulnerable, though for a different reason: the IEA’s projections point to strong long-term demand, but not immediate absorption of every subsidized project. That leaves a dangerous middle period in which governments may assume future scarcity, while the market is still digesting a wave of new supply.

Processing and stockpiling add another layer of risk. If allies build reserves independently and subsidize similar midstream capacity at once, they can amplify the imbalance. Instead of one coordinated supply chain, the world gets multiple partial supply chains chasing the same limited demand.

Coordination is the real policy test

Reuters reports that in May 2026 the G7 was discussing a permanent secretariat to coordinate critical minerals initiatives beyond rotating presidencies. That debate matters because coordination is the only realistic way to avoid subsidizing surplus. Shared planning can help governments time stockpiles, sequence financing and steer support toward genuinely missing links in the supply chain rather than duplicating the same projects.

In practical terms, the fix is not to abandon the push for non-China supply. It is to slow the race to build, align national reserves, and make sure allied countries are not subsidizing the same minerals at the same time. Without that discipline, the West may spend lavishly to reduce dependence on China, only to manufacture a new boom-bust cycle of its own.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip