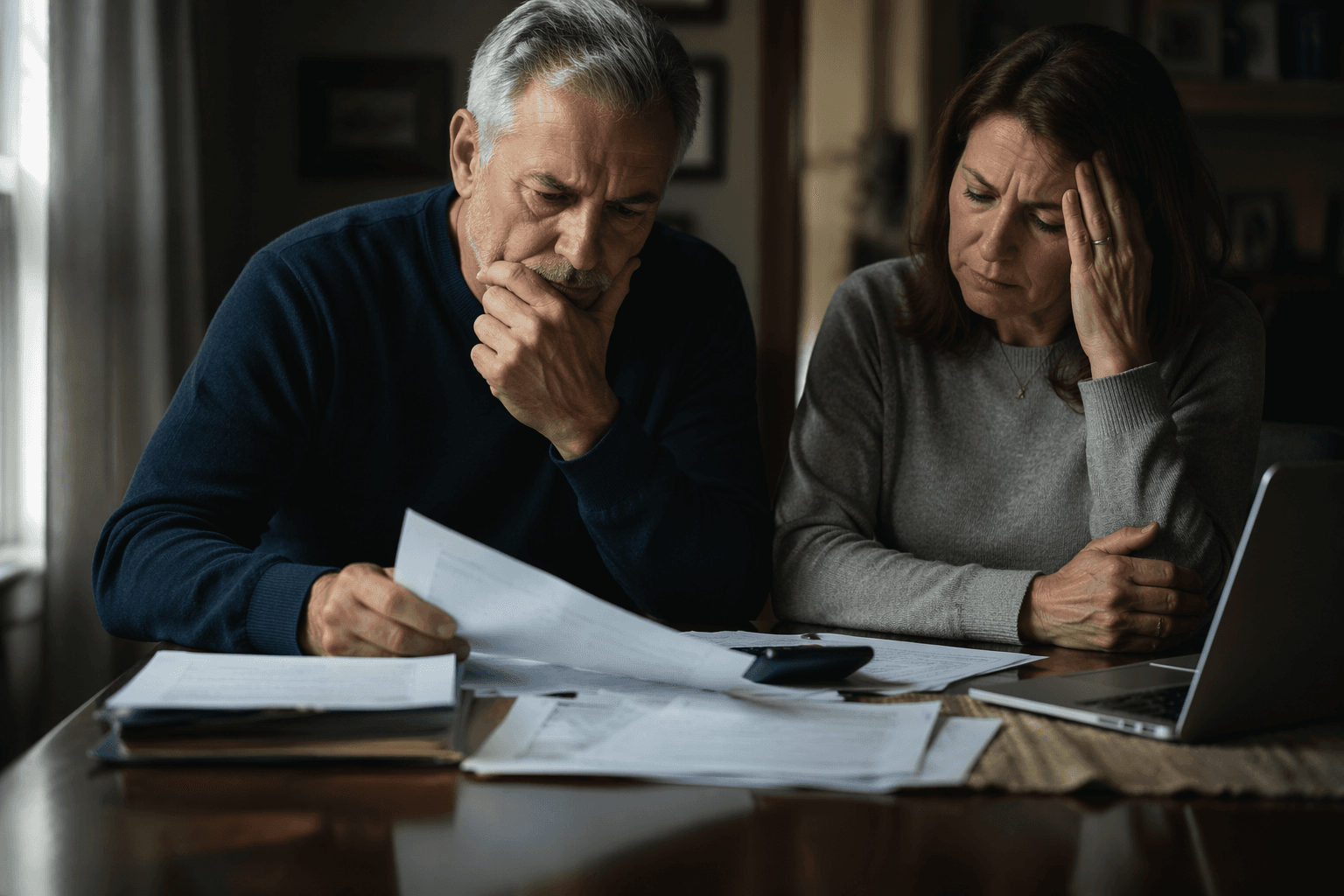

When debt dies with you, and when family still owes

Most debts stop at the estate, not the family, but co-signers, joint owners and some spouses can still be liable. Collectors often lean on grief, so the account structure and state law matter first.

In most cases, debt after a death is paid from the estate, meaning the money and property the person left behind, and if there is no estate money or property, the debt generally goes unpaid. Liability usually follows only when someone shared legal responsibility, or when state law creates an exception.

The first rule: the estate pays before relatives do

An estate is the legal bucket for what remains after death, and creditors are paid from that bucket according to state law. In Virginia, the payment order is explicit: costs and expenses of administration come first, then family allowances, then funeral expenses not to exceed $5,000, then debts and taxes with preference under federal law, before general claims.

A surviving spouse may expect that all creditors get paid evenly, but probate law can put funeral costs and statutory allowances ahead of ordinary bills. The result is often that some debts are reduced, delayed, or never paid at all because the estate is simply too small.

Who can still owe after a death

The clearest exceptions are co-signers and joint account holders. A co-signer remains responsible, and a joint credit card holder may share liability with the deceased person’s estate. By contrast, an authorized user is generally not liable, even on a deceased relative’s credit card, and can challenge a collector that tries to treat that status like a signed obligation.

Spouses are the most common source of confusion. A surviving spouse is generally not responsible unless the debt is shared, the spouse is otherwise liable under state law, or the couple lives in a community-property state that makes certain marital debts collectible from jointly held property. Alaska, if a special agreement is signed, Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington and Wisconsin are community-property states for this purpose.

Some states also have necessaries statutes, which can make parents or spouses responsible for certain necessary costs, including healthcare. That does not mean every medical bill becomes a surviving spouse’s bill, but it does mean medical debt deserves extra attention because the legal rules vary by state and by the type of expense.

What collectors can do, and what they cannot

Collectors may contact a surviving spouse, executor, administrator or other authorized person to discuss the deceased person’s debts, but they cannot tell that person, directly or indirectly, that the survivor must pay from personal funds. The FTC’s 2011 policy statement provides that the agency will not bring FDCPA enforcement action when collectors communicate with the spouse, the executor or administrator, or anyone else authorized to pay from estate assets, but it also makes clear that collectors must not mislead family members about personal liability.

They can also contact certain relatives only to locate the right person, but even then they are tightly limited. Collectors may speak with relatives to find the executor or administrator, but they should not discuss the debt, and when locating the right person they may not reveal or refer to the debt itself. If the collector knows you are the surviving spouse, the parent of a minor child, or a personal representative and still refuses to give basic debt details, that can be a scam signal.

This is a very common experience among survivors, and scammers often use false urgency or fear, especially when a family has just lost someone. Some collectors may try to capitalize on a surviving spouse’s vulnerability, particularly when the debt involves healthcare.

How to check whether the debt is actually yours

Start with the paperwork. Debt collectors generally must give details about the debt in the first conversation or within five days in a written validation notice, and you should ask for the debt in writing if anything feels off. If you think the debt is wrong, dispute it in writing within 30 days after receiving the validation notice, and be specific while sharing as little personal information as possible.

Then match the account to the legal relationship. Was the debt in the deceased person’s name only, or did you co-sign? Were you merely an authorized user, which generally does not create liability, or were you a joint account holder? Are you in a state where spouse liability exists by law, or in a community-property state that changes the answer? Those distinctions determine whether the collector is pursuing the estate, or trying to shift a debt to someone who does not owe it.

If you are the executor or administrator, the collector can discuss the estate’s debts with you, but that still does not mean the collector can reach into your personal accounts. Estate communication is not personal liability, and the debt collector cannot imply that you must cover the balance yourself.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip