Why a $35,000 money market account can still be a smart move

A $35,000 money market account is less about chasing yield than keeping insured cash liquid while rates cool and inflation stays sticky.

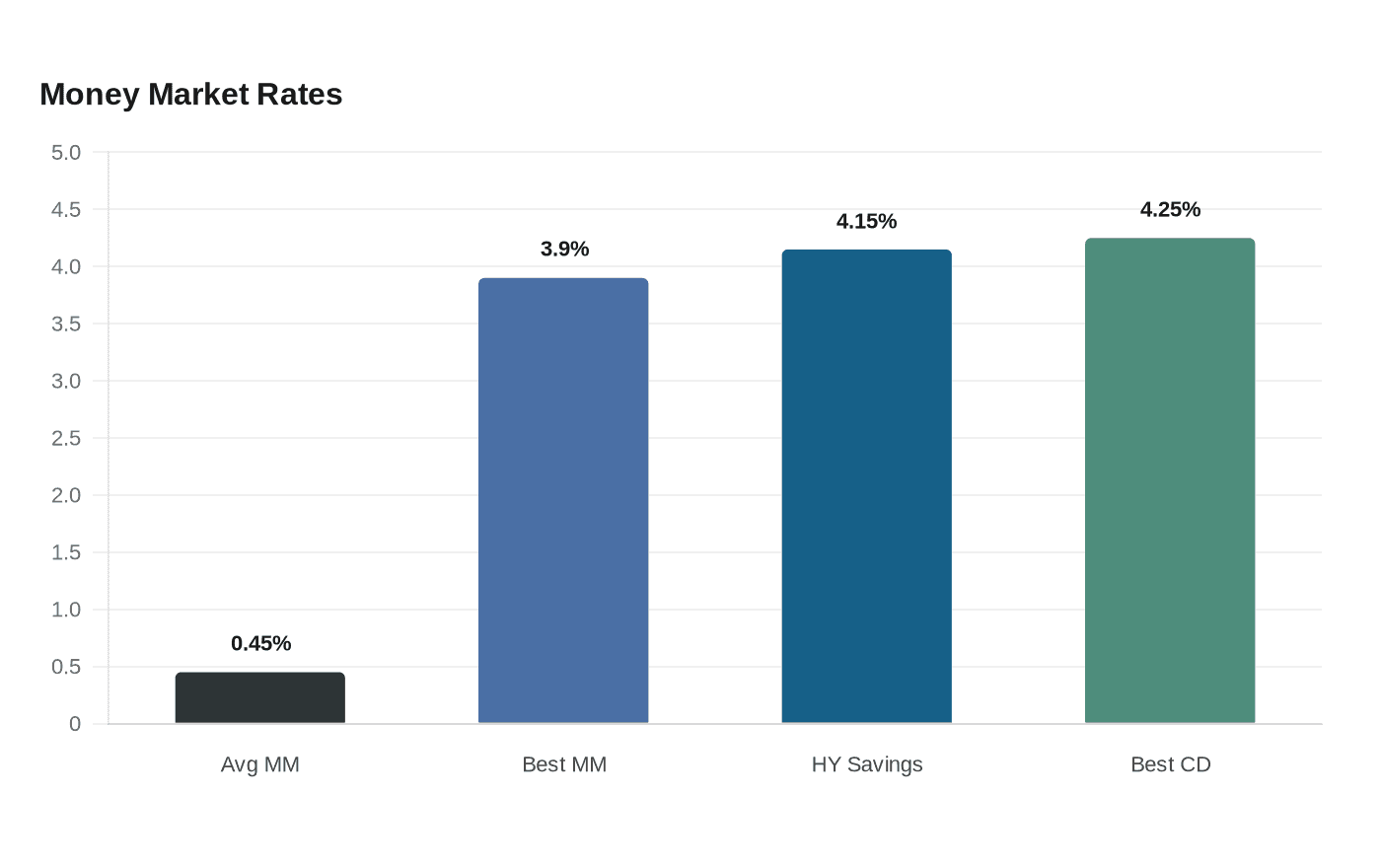

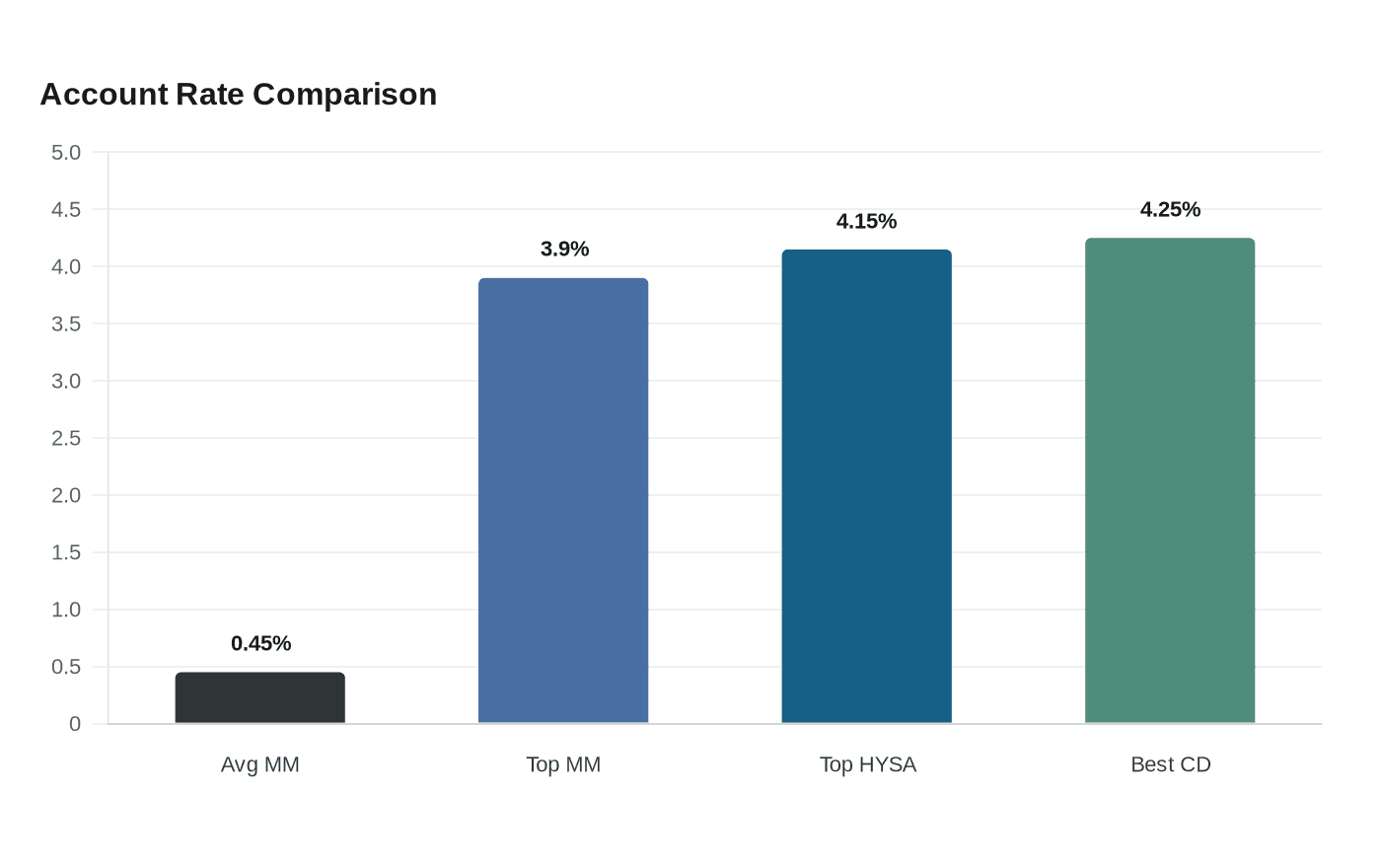

A $35,000 money market account is not where savers go to chase the market’s highest yield. It is where they park cash that still needs to stay available, insured and earning something while the Federal Reserve keeps policy restrictive and deposit rates begin to ease. Bankrate puts the average money market APY at 0.45%, while its best money market accounts still pay up to 3.90%, more than eight times the average.

What $35,000 earns at today’s rates

At the average money market APY of 0.45%, a $35,000 balance generates about $157.50 a year before taxes. FDIC national data for June 2026 show a 0.61% national money market rate and a 1.36% national rate cap, which would lift the same balance to about $213.50 at the national average but still leave it far below the strongest offers. Bankrate’s top money market accounts pay up to 3.90% APY, or about $1,365 a year on $35,000.

That comparison gets more interesting when you widen the lens to savings accounts and CDs. Bankrate says the top high-yield savings rate is 4.15%, which would produce about $1,452.50 on $35,000, while the best CD rates are around 4.25%, or roughly $1,487.50 a year on the same balance. In other words, the best money market accounts are competitive, but the average one is miles behind both top savings and CD offers.

Inflation changes the meaning of the yield

The bigger reality check is inflation. The Bureau of Labor Statistics said consumer prices were up 4.2% over the 12 months through May 2026, which means an average 0.45% money market yield does little to preserve purchasing power. Even a top 3.90% money market account still trails inflation on a simple nominal basis, while a 4.15% high-yield savings account and a 4.25% CD only edge ahead of it before taxes, and before any CD penalty if you need to break the term early.

That is why the quoted APY is only part of the story. Interest income from bank accounts, money market accounts and CDs is generally taxable, so the take-home return is lower than the headline rate, and the gap between nominal yield and real spending power matters more when inflation is still elevated. A saver looking only at APY can easily miss how much of the return is being swallowed by taxes and rising prices.

Why money market accounts still have an edge

Money market accounts earn their keep through access, not just yield. Bankrate describes them as deposit accounts that earn interest and often include check-writing privileges and debit card access, which makes them easier to tap than a traditional savings account. Bankrate also notes that savings accounts usually do not let you write checks, while CDs lock money away for a set period in exchange for a fixed rate.

That flexibility matters if the cash has a job to do soon. Money market accounts can work well for emergency reserves, tax payments, tuition, home repairs or any balance you may need on short notice without breaking a term deposit. A CD can pay a bit more, but the trade-off is clear: you surrender liquidity, and if rates keep falling, you are locked into your current yield rather than repricing with the market.

The rate backdrop is still favorable, but it is fading

The Fed’s June 17, 2026 decision to keep the federal funds target range at 3.50% to 3.75% explains why deposit yields are still elevated relative to long-run norms. Bankrate says savings and money market APYs have been decreasing and expects that trend to continue in 2026, with its forecast calling for top nationally available savings and money market rates to drift toward 3.70% by year-end. That is the core falling-rate risk for savers: a decent APY today can become a weaker one quickly if the rate cycle keeps turning.

Seen through that lens, a money market account is less a forever home for cash than a flexible parking place while rates are still relatively high. A saver who wants to stay liquid may accept a slightly lower yield than the best CD or best high-yield savings account, especially if the money needs to remain accessible and the Fed’s next move could be lower rather than higher.

Coverage is generous, but jumbo pricing is a different game

Safety is another reason the account still looks attractive. FDIC deposit insurance covers money market deposit accounts at FDIC-insured banks automatically, up to at least $250,000 per depositor, per FDIC-insured bank, per ownership category. A $35,000 balance sits comfortably inside that standard protection limit, so the main question is not whether the money is covered, but whether the account is paying enough for the flexibility it offers.

The catch is that the very best money market pricing often comes with balance hurdles far above $35,000. Bankrate’s jumbo money market roundup shows top yields tied to minimum balances such as $150,000, $250,000, $500,000 and even $1,000,000.01. That means a $35,000 saver may not qualify for the headline rates that make jumbo products look irresistible, and should not assume the top advertised APYs are available at ordinary household balances.

For a $35,000 saver, the smartest money market account is usually not the one with the flashiest banner rate. It is the one that keeps cash insured, accessible and earning enough to matter while rates slip lower, inflation stays above target and taxes take their share. In this rate era, that combination of liquidity, protection and modest yield is still a rational place to put money that cannot sit idle.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?

%3Amax_bytes(150000)%3Astrip_icc()%2FCertificate-of-deposit-2301f2164ceb4e91b100cb92aa6f868a.jpg&w=1920&q=75)