Why locking a mortgage rate before the June Fed meeting could pay off

A rate lock now is a bet against volatility, not just the Fed. With 30-year mortgage rates hovering near 6.5%, being late by a quarter-point could cost thousands.

Why the June Fed meeting matters now

Locking a mortgage rate before the June 16-17 Federal Open Market Committee meeting is less about predicting the Fed and more about avoiding a market swing that can hit borrowers fast. CBS News’ Matt Richardson noted that traders were pricing about a 99% chance the Fed would hold its benchmark rate steady, while the central bank has not cut since December 2025 and mortgage costs have still moved higher in recent months.

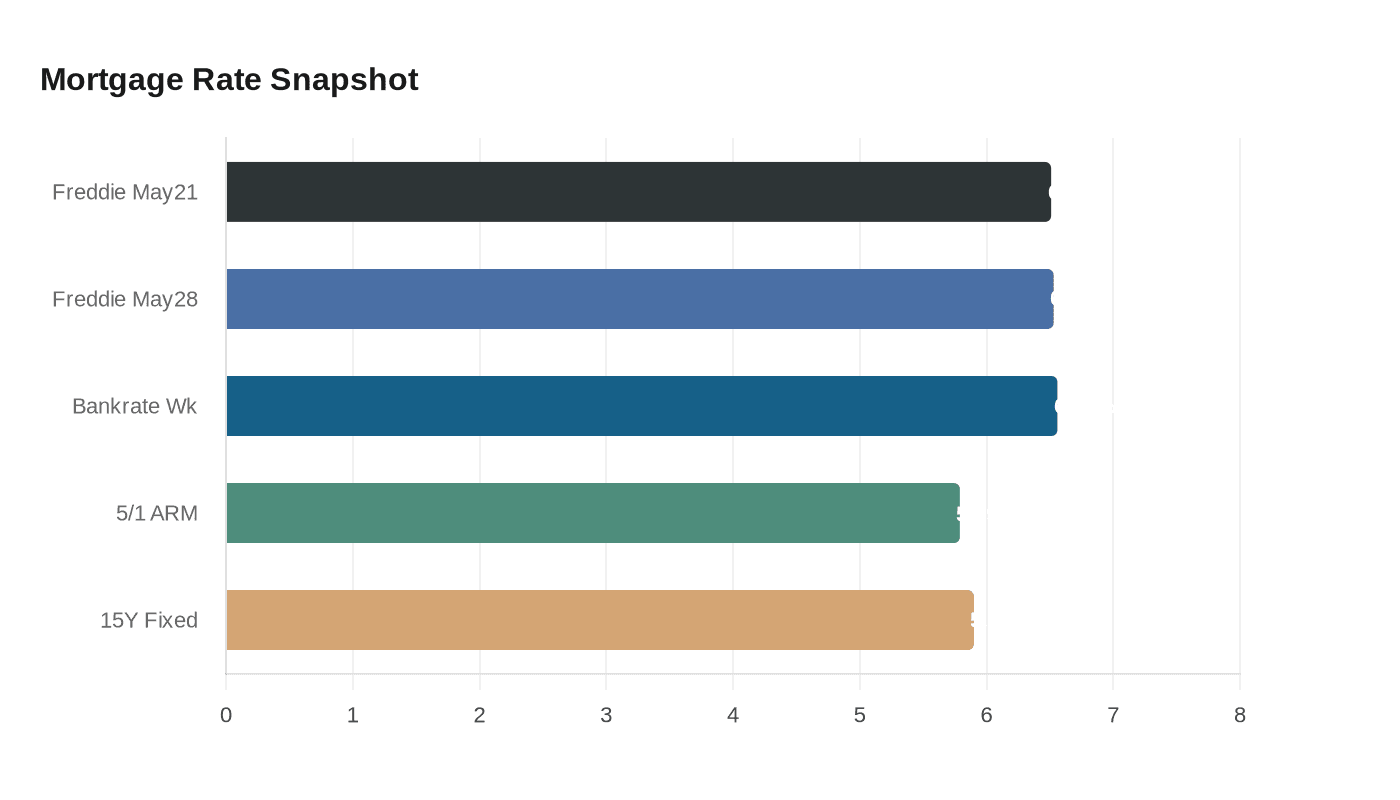

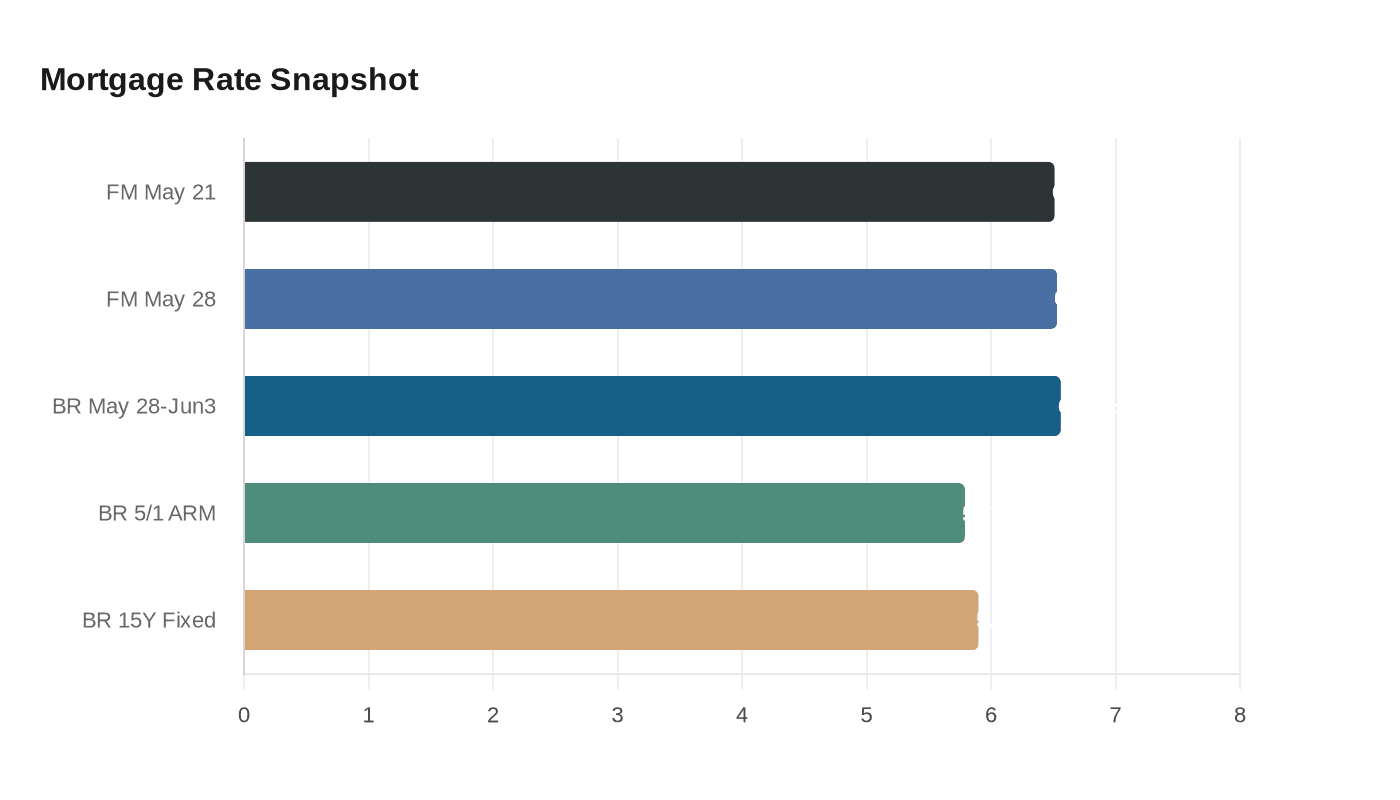

That matters because the Fed’s calendar gives the market plenty of chances to react. The Federal Reserve holds eight regularly scheduled meetings each year, and the minutes from those meetings are generally released three weeks after the policy decision, so the June decision can echo through lender pricing well beyond the two-day meeting itself. Freddie Mac’s weekly survey put the average 30-year fixed rate at 6.51% for the week ending May 21 and 6.53% for the week ending May 28, while Bankrate’s national survey showed 6.56% for the week of May 28-June 3.

The real bet is on volatility

Borrowers often hear “hold” and assume mortgage rates will simply sit still too, but that is not how this market works. Fannie Mae explains that the federal funds rate is an overnight rate, while the 30-year mortgage is benchmarked to the 10-year Treasury note, with lender costs, mortgage-backed-securities pricing and investor expectations all layered on top. The Atlanta Fed makes the same core point more bluntly: the Fed does not set mortgage rates, and the presumed lockstep relationship is a misconception.

That is why the market tone matters as much as the headline decision. Bankrate’s rate watchers said they were split on where mortgage rates were headed, and one of its experts said rates were likely to trade in a narrow range while investors waited for clearer direction from the Fed and broader economic signals. NerdWallet’s June outlook, written by Taylor Getler and edited by Johanna Arnone, warned that mortgage rates are likely to rise in June if conflict-related inflation pressures keep bond yields elevated.

Who should lock now

If you have already found a quote you can live with, the case for locking is strongest when your budget is tight or your closing date is close. Freddie Mac chief economist Sam Khater has said: “As rates fluctuate, aspiring buyers should remember that by shopping around for the best mortgage rate and getting multiple quotes, they can potentially save thousands.” That advice cuts both ways, because the same shopping process that finds a good quote can also make it disappear if lenders reprice after the meeting.

Borrowers who can still find sub-6% pricing have the most to gain from acting quickly. CBS News said qualified buyers may still be able to secure rates under 6% with strong credit, shopping around and, in some cases, an adjustable-rate mortgage. Bankrate’s June 2 archive showed a 5.79% average on a 5/1 ARM and a 5.90% average on a 15-year fixed loan, which is a reminder that the best available pricing is often not the standard 30-year quote.

Who can afford to wait

Waiting makes more sense if you have plenty of time before closing and enough flexibility to absorb a worse quote. That is not a prediction that rates will fall, only a recognition that some borrowers can tolerate the risk of being wrong because they are shopping, not signing, and because a better deal could emerge if Treasury yields soften after the Fed meeting. That said, waiting is still a bet on volatility, and volatility has been punishing borrowers this year.

Historical context argues for perspective, not complacency. Bankrate’s long-run rate guide, written by Andrew Dehan and edited by Alice Holbrook, shows the average 30-year fixed mortgage rate peaked just above 16% in 1981 and bottomed at just under 3% in 2021. Today’s 6.5% neighborhood is high compared with the pandemic era, but still far below the worst borrowing costs of past decades.

What a quarter-point mistake can cost

The hidden cost of waiting is not abstract. On a hypothetical $400,000, 30-year fixed loan, a rate of 6.53% works out to about $2,536 a month in principal and interest, while 6.78% would be about $2,602 a month. That 25-basis-point move adds roughly $66 a month, or about $23,834 over the life of the loan.

The upside can be just as meaningful. If a borrower instead lands 6.03% rather than 6.53% on that same $400,000 loan, the payment falls to about $2,406 a month, saving roughly $130 monthly and nearly $46,889 over 30 years. That is why locking is not really about guessing the Fed’s next move; it is about deciding how much uncertainty you want to carry into one of the biggest debts you will ever take on.

The June Fed meeting is likely to be a hold, but the mortgage market can still move on tone, yields and lender repricing. If your numbers work now, certainty may be worth more than the hope of squeezing out one more fraction of a point later.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?