Top sires tighten grip as Thoroughbred breeding faces consolidation

A shrinking circle of super sires is taking a bigger share of breeding money and racing output. The squeeze is remaking who gets in, who gets priced out, and who shapes the next stakes crop.

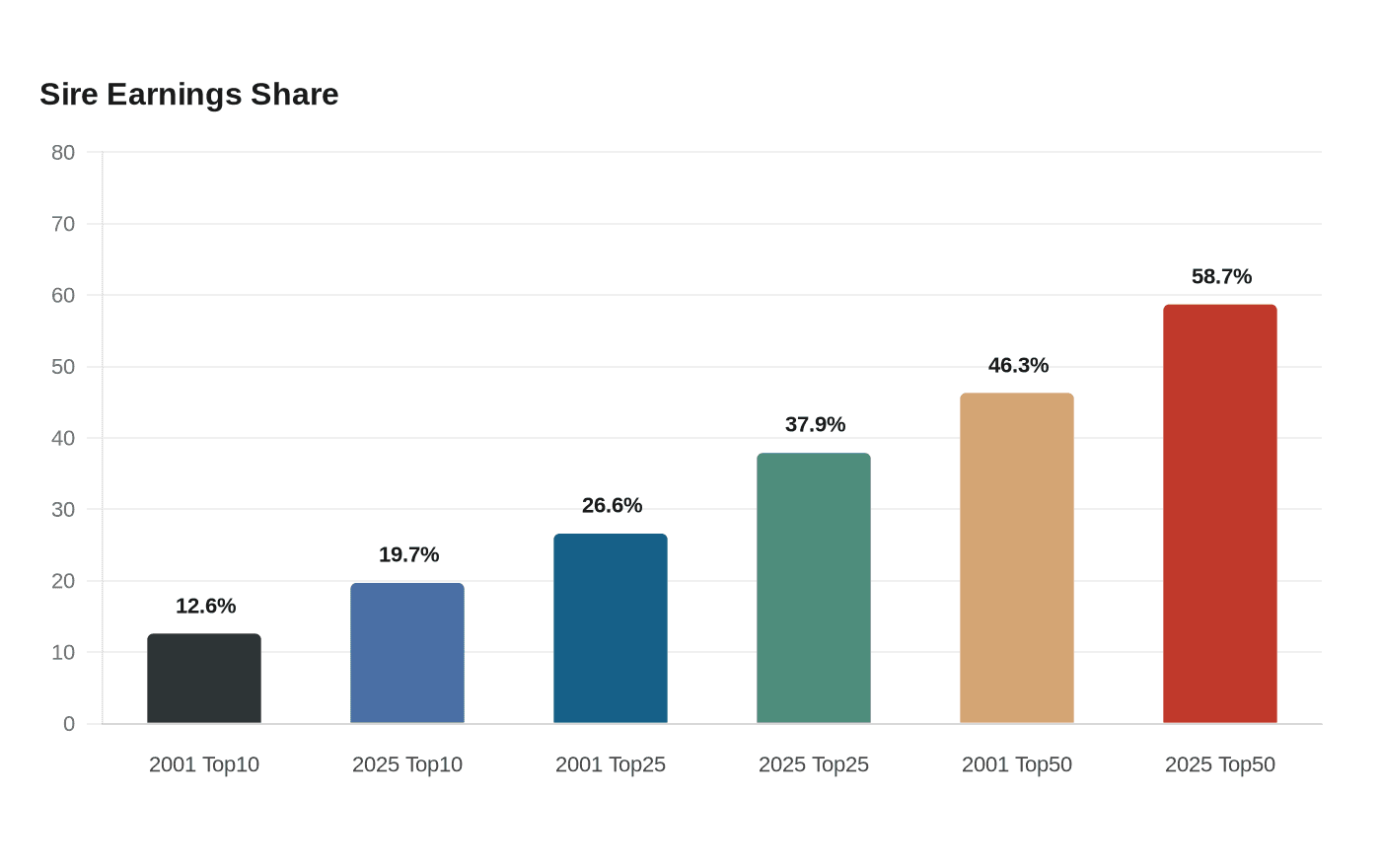

The breeding shed is tilting toward a smaller class of giants, and the effect reaches from the foaling barn to the sales ring to the races themselves. A review of progeny earnings from 2001 through 2025 shows the top 10 sires lifting their share from 12.6% to 19.7% among the top 150, while the top 50 climbed from 46.3% to 58.7%. That is not just concentration. It is a power shift that is making Thoroughbred breeding more industrial, more centralized, and harder for smaller programs to break into.

The numbers behind the squeeze

The clearest sign of consolidation is not simply that the elite remain elite, but that they are absorbing more of the whole market. In 2001, the top 25 sires accounted for 26.6% of progeny earnings among the top 150 sires; by 2025, that figure had reached 37.9%. The top 50 moved from 46.3% to 58.7% over the same span, which means the middle of the sire population is losing economic room even when the headline names stay familiar.

The threshold for market control has also shifted. Roughly 56 sires were needed in 2001 to account for half of progeny earnings among the top 150, compared with about 42 or 43 in 2025. That is a meaningful change in how power is distributed: fewer stallions now command the same revenue base, and the rest are left fighting over a thinner slice of the pie.

There is a twist inside that trend. Inflation-adjusted stud fees at the very top have not risen proportionally, and in real-dollar terms they are lower than they were in the early 2000s. So the top end is more concentrated, but not necessarily more expensive in a simple, one-directional way. The economics are more complex: larger books, wider commercial pull, and a market that keeps rewarding proven sires even when the sticker price does not keep pace with inflation.

What that means for the racetrack

This is where the breeding story becomes a racing story. When a handful of stallions dominate the commercial pipeline, pedigrees tend to get more uniform, and the range of genetic profiles available to buyers narrows. That can mean fewer breakout rivals emerging from outside the commercial core, because the same names keep shaping the same major crops.

The TDN analysis points to a broader consequence as well: breeding, racing, and sales are becoming more tightly linked. The model is increasingly built around scale and risk management, where a stallion’s value is reinforced by his offspring’s performance, the size of his book, and the marketplace appetite for his yearlings and 2-year-olds. In that environment, the stallion is not just a sire, he is a central asset in a connected business system.

For owners and breeders, that changes how competitive decisions get made. Smaller stallion farms and regional programs, once able to matter more meaningfully in the early 2000s, face a tougher road when commercial buyers concentrate their attention on a narrow set of proven names. The result is a marketplace that can produce powerful stars, but may offer less variety when it comes to the next wave of stakes horses.

Kentucky’s widening edge

The geographic center of gravity is shifting right along with the sire rankings. The Jockey Club reported 24,681 mares bred to 740 active stallions in North America in 2025, down 4% from 2024, and projected a 2026 foal crop of about 17,000, roughly 300 fewer than the prior year. That does not suggest a broadening of the breeding base; it suggests a tighter, more selective market.

Kentucky now sits even deeper at the center of that market. The state accounted for 66.34% of all mares bred in North America in 2025, up from 57% in 2018. That jump matters because concentration is not only about who the sires are, but where the business is happening. The more the activity piles into one state, the more regional programs have to fight against gravity.

The Jockey Club’s 2026 Fact Book adds one more layer to the picture: its breeding statistics are updated daily, and 2025 racing data are considered final but still subject to revision. That means the industry is watching this consolidation in real time, with the numbers moving under its feet even as the overall direction stays clear.

The stallions driving the books

The current cover list shows how quickly a few names can crowd out the rest. BloodHorse’s 2025 Report of Mares Bred listed Tiz the Law at 274 mares bred, Arabian Knight at 273, Practical Joke at 263, and Justify at 244. Charge It followed with 235, Domestic Product with 224, Gun Runner with 218, and Not This Time with 214. Those are not just busy books. They are the kinds of books that reveal where commercial trust is being placed.

Tiz the Law stood out even among that group. Paulick Report said he finished 2025 as North America’s most active stallion and posted the biggest year-over-year jump, rising by 116 mares after covering 158 in 2024. That kind of surge is a useful marker for the market: once a stallion catches, breeders pile in fast, and the book can expand with remarkable speed.

That expansion matters because bigger books create a reinforcing loop. The more mares a stallion covers, the more foals he can have on the ground, the more visible his influence becomes in future racing crops, and the more easily buyers can identify his offspring in the sales ring. In a concentrated market, a strong season does not just improve one stallion’s standing. It can rearrange the calendar of who gets bred next.

Why the sales ring keeps feeding the cycle

The sales market is helping lock in the same pattern. BloodHorse’s 2025 North America sales sire data showed repeated appearances by a small group of elite sires, including Into Mischief, Gun Runner, Curlin, and Tapit, with dozens of runners sold and strong cumulative gross figures. That kind of repetition tells buyers where the commercial center of gravity sits.

Once that feedback loop takes hold, breeding, racing, and sales companies become harder to separate. The most successful stallions are not only producing runners, they are shaping the catalog, the auction results, and the decisions that determine which mares get booked next. That is the industrial side of the sport, and it is becoming more visible every season.

The long view is stark. The commercial Thoroughbred breeding world of the early 2000s still had more room for a wider range of sires and regional operators to matter. By 2025, the system looks more top-heavy, more Kentucky-centric, and more dependent on a few super sires to drive the economics. That may produce deeper commercial certainty, but it also narrows the path for outsiders, and it changes the shape of the future stakes horse before the first foal even stands up.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip