45Z rules and California LCFS tighten low-carbon fuel competition

45Z and LCFS are turning low-carbon fuel into a carbon-intensity race, with higher-CI gallons set to lose value as benchmarks tighten.

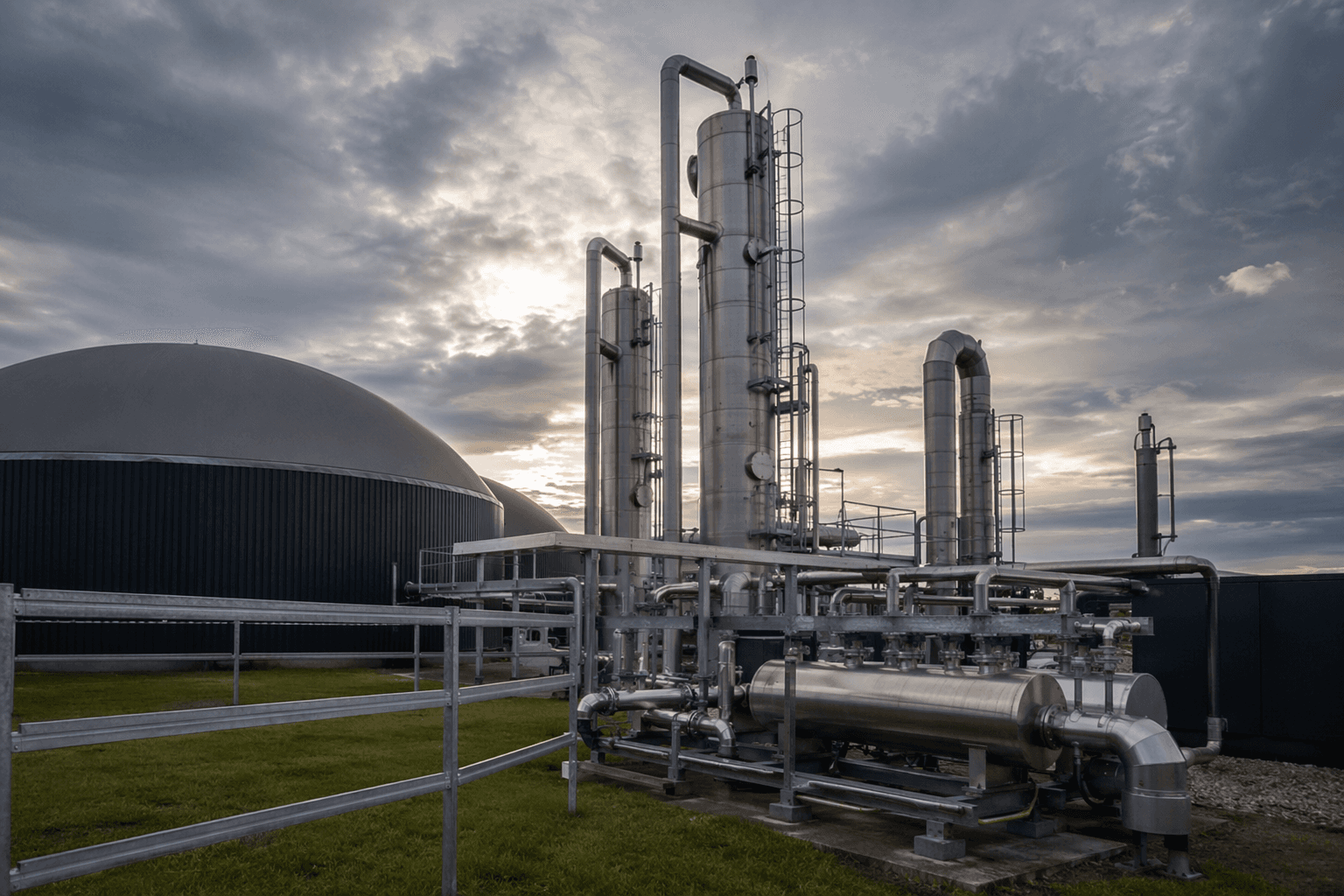

The low-carbon fuel business is moving out of the easy-credit phase. Treasury and the IRS on Feb. 3 proposed 45Z rules that cover domestic fuel produced and sold from Jan. 1, 2025 through Dec. 31, 2029, while California keeps tightening the LCFS toward steeper carbon-intensity cuts. The result is a narrower market in which feedstock origin, plant design and documentation now matter as much as gallons.

45Z is becoming a supply-chain test, not just a tax break

The proposed clean fuel production credit rules give producers a defined runway, but they also draw a harder line around sourcing. Under the IRS framework, qualifying fuel produced after Dec. 31, 2025 must be made from feedstocks produced or grown in the United States, Mexico or Canada, which puts procurement, contracting and logistics inside the policy calculation. Treasury said the proposal was meant to provide “further certainty and clarity” and address key stakeholder concerns, a signal that producers have been asking for a stable rulebook before making investment decisions.

That matters because 45Z is not simply a margin booster layered on top of existing programs. It is already being used by producers to improve returns, but the regional feedstock screen means the credit will reward businesses that can control origin and emissions accounting, not just volume. Biofuel and farm groups, including the American Coalition for Ethanol, have pressed for swift final rules and more certainty for farmers and producers, reflecting the pressure on both processors and growers to plan around the new eligibility line.

California’s LCFS is tightening the floor under the market

California approved the LCFS in 2009 with an original target of a 10% reduction in carbon intensity by 2020 versus a 2010 baseline. The program’s 2024 amendments extend the policy deeper into the next two decades, with CARB now aiming for a 30% reduction by 2030 and 90% by 2045. Those amendments also add an Automatic Acceleration Mechanism that can speed up benchmark declines if the credit bank grows too large relative to deficits, which makes the policy more dynamic and less forgiving when supply outruns demand.

CARB says the LCFS has already reduced transportation-fuel carbon intensity by almost 13% and displaced 320 million metric tons of CO2 from gasoline and diesel emissions since the program began. That record is why the market still treats the LCFS as a core price signal, but the same success is also what drives the next tightening cycle. CARB’s quarterly reporting framework, which summarizes reported fuels, credits and deficits and publishes underlying data for the latest report on a fixed schedule, gives regulated parties a running view of where the compliance market is headed.

CARB has also begun spelling out how the faster decline can work in practice. Guidance 26-01, issued March 27, 2026, lays out implementation scenarios for the Automatic Acceleration Mechanism and the related reporting steps. For producers, that means the LCFS is no longer a static program where one can assume today’s spread will still hold next quarter.

Ethanol is still in the game, but the margin for error is shrinking

The near-term math still leaves room for many ethanol pathways, but the longer-term slope is sharper. The article’s cited 2026 compliance threshold is a 24.2% reduction, yet the benchmark is moving toward a 52.5% reduction by 2035. Average ethanol CI scores in the third quarter of 2025 were 58.59 gCO2e/MJ, which shows how quickly current supply can drift out of favor as the benchmark tightens.

By 2035, CI scores above 47.09 gCO2e/MJ for the gasoline curve and 50.23 gCO2e/MJ for the diesel curve will generate deficits rather than credits. That is the key commercial shift: a molecule that clears today’s line may not clear the next one, and a plant that barely qualifies now could become a deficit generator later. Lower-CI ethanol supply should attract more attention from regulated parties, while higher-CI gallons risk seeing their value erode as the curve tightens.

What producers have to optimize now

The market is moving away from simple credit generation and toward continuous carbon management. Producers that want to stay competitive need to treat logistics, feedstock selection, plant efficiency, carbon capture and sequestration, and documentation as one integrated system rather than separate functions.

- Feedstock sourcing: 45Z’s post-2025 North American requirement makes origin tracking and contracting part of the margin story.

- Plant efficiency: lower energy use and cleaner process heat can push a pathway below the next LCFS or 45Z threshold.

- Carbon capture at ethanol plants: CCS can materially reduce CI, which becomes more valuable as benchmark gaps narrow.

- Documentation and certification: as CARB’s quarterly reports and 45Z registration rules become more important, incomplete paperwork can erase the benefit of a lower-carbon operation.

The broader point is that low-carbon fuel is becoming a quality market. Producers that can keep CI well below the benchmark will still capture value, but the days of relying on broad compliance demand and easy arbitrage are fading. In the next phase, the winners will be the companies that can prove, quarter after quarter, that their gallons stay ahead of the curve.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?