Agenzee maps the insurance software stack carriers need in 2026

The new carrier stack is less about vendor count and more about how cleanly systems connect. Integration depth and data flow now separate table stakes from true advantage.

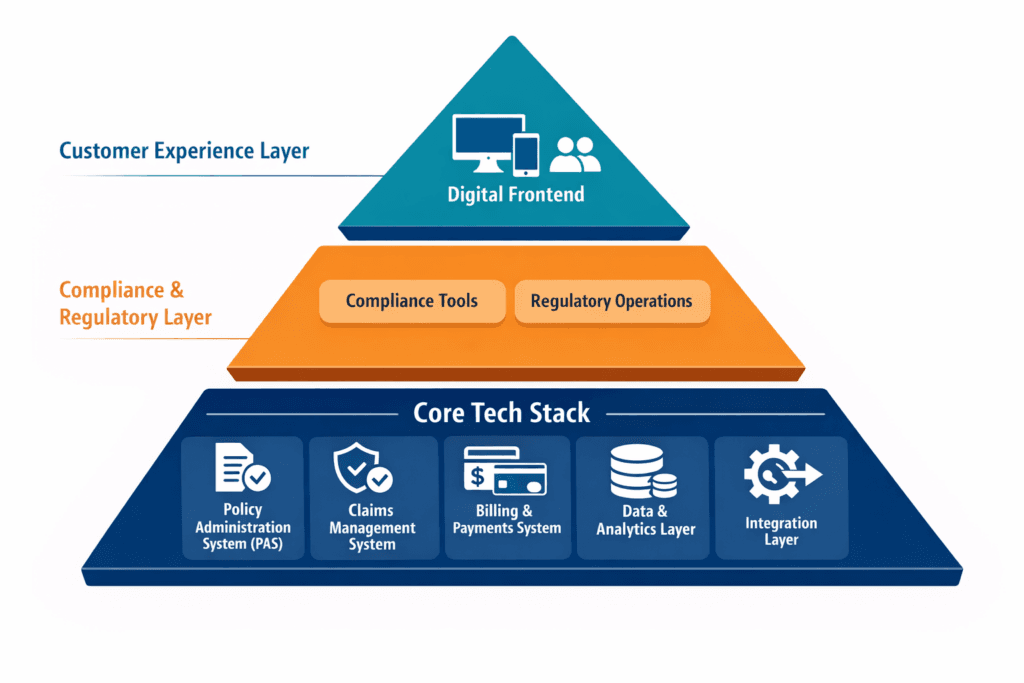

The carrier stack is now an architecture decision, not a shopping list

The most important software decision for a P&C carrier is no longer which single platform to buy. It is how to assemble a stack that connects underwriting, claims, compliance, data, and distribution without creating new friction, and Agenzee’s updated 2026 guide makes that shift plain.

That framing matters because legacy architectures do more than slow teams down. They create silos, raise maintenance costs, and make it harder to launch products or adapt to changing markets. In practical terms, the real question is not how many vendors sit in the environment, but whether the stack can move data cleanly, keep workflows coherent, and support the full insurance lifecycle.

What is now table stakes

Some categories have become mandatory because they sit at the center of day-to-day operations. Compliance platforms, underwriting systems, APIs, and analytics tools are no longer nice-to-have additions around the edges. They are the connective layer that lets a carrier operate with speed and visibility.

This is where the industry’s thinking has shifted from monolithic systems to connected components. ACORD’s Reference Architecture describes an enterprise framework for insurance made up of seven interrelated industry models, which is a strong signal that the market now expects carriers to think in terms of relationships between capabilities, not a single all-in-one platform. ACORD also released interactive online versions of those models on January 29, 2026, reinforcing the push toward architecture that is easier to explore, compare, and operationalize.

Core administration and claims still define the backbone

Policy administration and claims remain the backbone of the stack, but the bar for those systems has changed. A core platform is no longer judged only on whether it can issue policies or manage claims queues. It is judged on how well it shares data, how quickly it supports product changes, and how much integration work it forces everywhere else.

That is why vendors are now leading with connection points as much as core features. Guidewire says its APIs are designed to streamline integration and improve underwriting, claims processing, and customer experience. Duck Creek takes a similar position, saying its policy administration system uses an API-first approach and open architecture to support multiple channels while reducing maintenance through a single point of change. The message is consistent: the core system must do the heavy lifting, but it also has to behave like a good neighbor to everything around it.

Data is the hidden layer that decides whether the stack works

Data may not be the flashiest category in the stack, but it is the one that determines whether the rest of the architecture pays off. If underwriting cannot see the same customer and exposure data that claims, compliance, and distribution use, the carrier ends up reconciling duplicates instead of making decisions. That is the hidden tax of poor stack design, and it is one of the clearest signs that integration debt is accumulating.

A coherent stack should let data move quickly enough to support context-rich underwriting and a cleaner claims process. It should also make analytics useful rather than retrospective, because dashboards built on fragmented records only describe the problem after the fact. In a modern carrier environment, data is not a separate reporting layer bolted onto operations. It is the operating fabric that makes the rest of the system intelligible.

AI is becoming part of the stack conversation, not an add-on

The AI discussion is moving from experiment to workflow orchestration, and that changes how you should evaluate the stack. ACORD’s 2026 predictions say agentic AI could support data analysis, routine decisions, and data enrichment in underwriting and claims analysis. That is a meaningful shift because it places AI inside the operating sequence, not outside it as a standalone tool.

For P&C leaders, the implication is practical: AI will only deliver value if the underlying architecture can expose clean data and support controlled decision-making. If the stack is still stitched together with brittle handoffs, AI will inherit the same friction the carrier already has. The opportunity is real, but so is the risk of automating bad plumbing.

CRM, distribution, and payments are where coherence becomes visible

Customer relationship management, distribution, and payments often get treated as secondary systems, yet they are where stack coherence becomes visible to the business. CRM should not merely store contacts. It should connect to underwriting and service workflows so that agents and internal teams are working from the same view of the customer.

Distribution tools, meanwhile, have to support multiple channels without multiplying operational complexity. That is one reason API-first design matters so much in modern insurance architecture: if the stack cannot feed brokers, agents, partners, and direct channels without custom work for each one, the carrier pays for every new route to market with more maintenance. Payments sit in a similar position, because billing and transaction flows touch customer experience, reconciliation, and compliance at once.

How to evaluate stack coherence instead of vendor count

When you look at a carrier stack, the best test is not how many products are in it. It is how many places a human has to intervene to move information from one function to another. If a policy change requires manual fixes across underwriting, claims, compliance, and finance, the stack is already leaking value.

A stronger evaluation framework looks like this:

- Can core admin systems share data cleanly with claims and CRM?

- Are APIs treated as infrastructure, or as a patch for poor design?

- Does the data layer support both operational decisions and analytics?

- Can compliance visibility travel with the transaction instead of being checked later?

- Will the architecture support new channels without creating one-off maintenance?

That is where the Agenzee guide lands with force. It treats carrier software as an operational system, not a product catalog, and that is the right lens for 2026.

The modernization push is not new, but it is accelerating

This conversation did not appear overnight. A Guidewire summary of Datos Insights research says addressing core systems and sunsetting legacy systems remained a priority for property and casualty innovation leaders in 2025, which shows the pressure has been building for some time. The real change is that modernization is no longer framed as a back-office cleanup project. It is now tied directly to how fast carriers can launch, adapt, and compete.

That broader trend also explains why the stack conversation keeps returning to integration depth, configurability, and data sharing. The carriers that win will not be the ones with the longest software list. They will be the ones whose architecture lets underwriting, claims, compliance, data, AI, CRM, distribution, and payments work as one system rather than a cluster of disconnected purchases.

Know something we missed? Have a correction or additional information?

Submit a Tip