Claims modernization becomes P&C insurance’s key battleground, Five Sigma says

Claims is no longer a back-office afterthought: Five Sigma says the real P&C fight now happens in how fast, accurate, and human the claim feels.

The battleground has moved to claims

In P&C insurance, the policy still matters, but it is no longer the whole fight. Five Sigma’s new guide argues that the decisive competitive edge now sits in the claims experience, where speed, accuracy, and judgment collide in front of the customer.

That matters because P&C is not a niche line. Five Sigma pegs it as a $1.6 trillion global market spanning more than 15 lines of business, which means even small gains in claims performance can ripple across a huge revenue base. The guide’s core point is simple: if two carriers sell similar coverage, the one that settles faster, makes fewer mistakes, and keeps the process intelligible will usually win the long game.

Why modernization pressure is rising now

The push is coming from several directions at once. Five Sigma points to rising catastrophe activity, deteriorating combined ratios, and a retirement wave among senior adjusters as the structural forces making claims modernization urgent. In other words, carriers are being squeezed by more complex losses, thinner margins, and a shrinking bench of experienced people who know how to handle the hard files.

The underwriting side is not exactly providing much room to breathe either. The Insurance Information Institute and Milliman said the U.S. P/C industry posted a net combined ratio of 96.6 in 2024, the best underwriting result since 2013. Yet the same industry still faced elevated catastrophe losses, inflation-driven claims costs, and economic volatility in 2025, even as the net combined ratio reached its lowest level in more than a decade. That combination is why claims performance has moved from a support function to a profitability lever.

Deloitte’s workforce findings sharpen the point. In discussions with chief claims officers during 2024 and 2025, it reported an average attrition rate of 20% in claims, with each departure representing the loss of nearly six years of experience. When that much institutional memory walks out the door, the software has to do more than store notes. It has to carry judgment, routing logic, and operational discipline.

What the 2026 buying checklist should really ask

This is where a lot of vendors still talk too much about intake and too little about orchestration. Five Sigma’s guide is valuable because it walks the full claims lifecycle, from first notice of loss through closure, and treats AI as a way to support adjuster judgment rather than replace it. That is the right framing for 2026 buying decisions: the best systems are not just document collectors, they are workload coordinators.

If you are evaluating claims platforms now, the checklist should look more like this:

- Can the platform orchestrate tasks across the full claim, not just ingest forms and attachments?

- Does it help prioritize work so adjusters see the right files first, especially when CAT volume spikes?

- Can it reduce leakage by catching missing data, routing exceptions earlier, and standardizing decisions on routine losses?

- Does it preserve human expertise by making prior decisions, playbooks, and file history easy to surface in complex claims?

- Can it improve customer experience with faster updates, cleaner handoffs, and fewer avoidable status calls?

That is the practical test. A claims system that cannot do all five is still just a digital filing cabinet with a better sales deck.

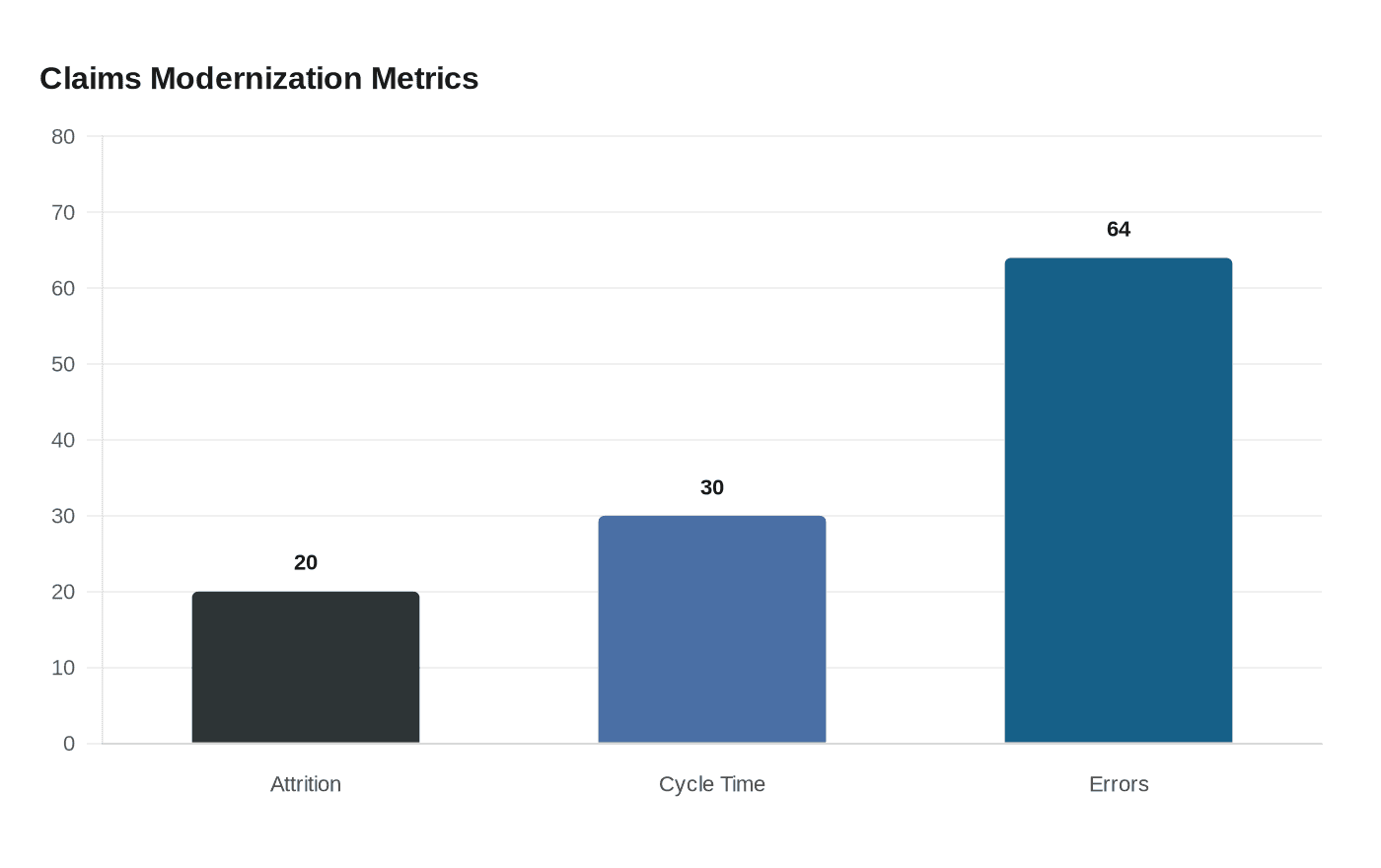

AI is becoming useful where it touches the file, not where it dazzles

Five Sigma says AI-native claims management can cut cycle times by about 30% and reduce errors by 64%. Those are the numbers that matter to a carrier CFO, but they also explain why the market is moving beyond pilot projects and toward real workflow change. The value is not in generic automation. It is in speeding up the specific, repetitive work that slows adjusters down and introduces avoidable leakage.

Accenture has pushed the same basic point from another angle, saying AI and generative AI can reduce claims cycle time from days to minutes in some workflows. That does not mean every claim becomes instant. It does mean the right sub-processes, such as triage, document extraction, summarization, and next-step routing, can be compressed dramatically when the data is clean and the process is disciplined.

EY’s survey findings show the market is getting more comfortable with that shift. Insurers are moving GenAI use cases away from back-office experimentation and toward front-office applications, with stronger confidence in controls and customer-facing use cases. That is an important signal for claims, because claims is where automation either improves trust or destroys it. The best tools do not hide the adjuster. They make the adjuster faster, more consistent, and easier to reach.

The real job: protect judgment, reduce leakage, improve service

The biggest mistake in claims modernization is assuming the goal is to replace people. Five Sigma’s guide gets this right by positioning AI as a support layer for adjuster judgment. That is exactly how carriers should think about it when evaluating platforms in 2026. The point is to eliminate low-value handwork, not to flatten the expertise that separates a simple auto loss from a messy commercial property claim.

That distinction matters because claims is where hidden costs pile up. Leakage often lives in delays, missed follow-ups, inconsistent reserving, and poor handoffs, not in one giant catastrophic error. A modern platform should therefore make it easier to spot bottlenecks, escalate exceptions, and keep the file moving without forcing the adjuster to hunt across systems for the next piece of context.

The customer experience case is just as strong. In a market where policy features are easy to copy, claims becomes the memory of the brand. A carrier that communicates clearly, settles fairly, and handles complexity without endless friction creates loyalty that underwriting alone cannot buy. That is why the claims stack has become the software priority reset in P&C: it is where operational efficiency, talent retention, and customer trust all meet the same file.

What the next purchase should deliver

Five Sigma’s message fits the broader 2025 to 2026 shift in how insurers buy technology. Claims platforms are being judged less on feature checklists and more on measurable outcome improvements. That means shorter cycle times, lower error rates, better workload balance, and a cleaner experience for both adjusters and claimants.

The carriers, MGAs, TPAs, and self-insureds that move first will not just automate paperwork. They will build claims operations that can absorb staff turnover, handle higher catastrophe frequency, and keep service levels intact when the market gets ugly. In P&C, that is no longer a nice-to-have. It is the competitive line that separates a modern insurer from an exposed one.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?