Cotality pushes cognitive imagery and AI for property insurance decisions

Cotality is betting that cleaner imagery and better orchestration, not just more AI, will cut insurance friction. The real test is whether it fixes handoffs and cycle times.

The pitch is bigger than a rebrand

Cotality is trying to sell property insurers on a simple idea: there is already plenty of data, but not enough usable intelligence at the point of decision. The company’s answer is a four-part model built around cognitive imagery, seamless workflows, interoperability, and agentic AI, and it says that framework became the backbone of its insurance strategy as it entered 2026, its first full year under the Cotality name after the March 24, 2025 rebrand from CoreLogic.

That matters because this is not a clean-sheet startup story. Cotality is layering a new AI-centered message onto a long-standing valuation and property-data business, including Marshall & Swift replacement-cost data that it says has been trusted for more than 90 years. For buyers, that makes the real question more practical than philosophical: which of these pillars actually shortens the path from image capture to underwriting or claims action, and which ones mostly sound good in a slide deck?

Start with the pain points carriers actually feel

If you work around property claims or underwriting, the daily friction is familiar. Inspection images sit in one system, policy data in another, valuation tools somewhere else, and the actual decision often arrives after a manual handoff or two that slows everything down. Weak API connectivity only makes the problem worse, because even good data becomes annoying data when a team has to move it by hand.

That is the gap Cotality is trying to close. Its interoperability pillar is aimed at unifying underwriting, claims, and restoration workflows into a single source of truth, while seamless workflows are meant to reduce the stop-and-start that turns an otherwise routine file into a bottleneck. In buyer terms, those are the claims worth pressure-testing first, because they directly affect cycle times, data quality, and the amount of human cleanup required before a decision can be trusted.

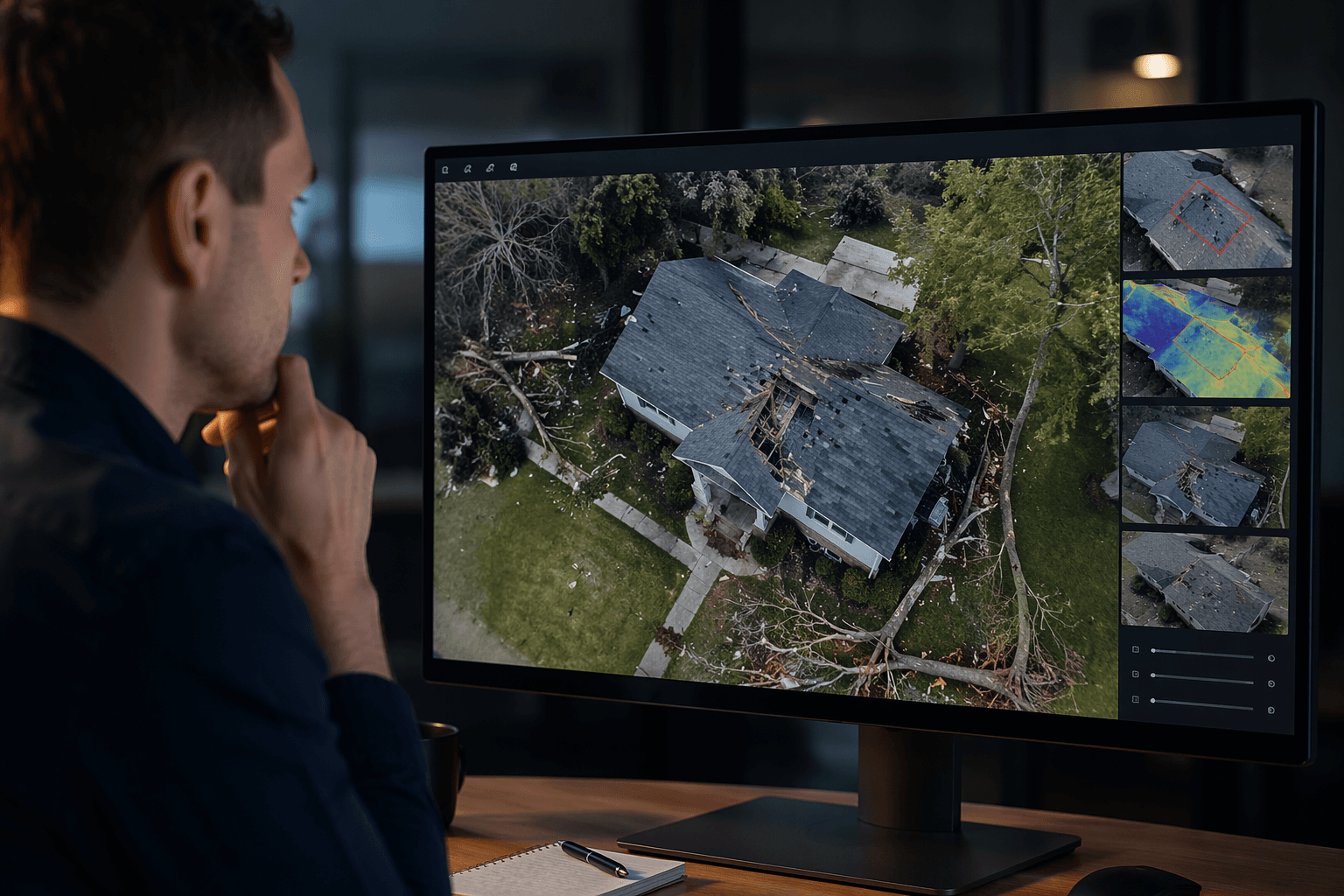

Cognitive imagery is the most concrete part of the story

Of the four pillars, cognitive imagery is the one that sounds the least abstract, and probably for good reason. Cotality describes a process that starts with aerial and ground-level property photos and then enriches those images with tax records, MLS listings, claims records, and other sources so underwriters can work from a fuller evidence base. The goal is not just prettier property files, but better-informed decisions with less guesswork and fewer human errors.

That is where the buyer conversation gets real. If imagery remains a standalone asset, it adds review time. If it becomes a structured input that helps automatically populate underwriting estimates with relevant property characteristics, it starts to change implementation outcomes in a measurable way. Cotality says its Residential Valuation product can already do that from a street address using appraisal data, MLS listings, and other sources, which is the kind of automation that can save time only if the underlying data is clean enough to trust.

The data foundation is the part that gives the pitch some weight

Cotality is leaning hard on scale, and that is not a bad instinct in a market where AI systems are only as useful as the data underneath them. The company says its Property Characteristics dataset covers 154 million-plus residential and commercial properties in the United States, and that some of its property datasets include more than 5.5 billion records, updated daily, with up to 99.9% U.S. coverage and 50-plus years of history in some product lines.

Those numbers do not guarantee a better workflow, but they do explain why Cotality keeps emphasizing AI-ready data and interoperability instead of AI alone. A claims team working with sparse, stale, or mismatched property data will not get far with another layer of automation. A platform built on broad coverage and deep historical records has a better shot at reducing rework, especially when the use case is valuation, property comparison, or triage at scale.

Where the agentic AI claim deserves scrutiny

Cotality’s AI language is broad, and it names machine learning, generative AI, CoreAI, and deep learning across billions of data points from tens of thousands of sources. That tells you the company wants to be seen as more than an imagery vendor or a valuation shop. It also tells you to be careful about what counts as substance.

Agentic AI is the least useful pillar to judge on its own, because the real question is not whether an agent exists in the marketing sense. The better question is whether it can move files through underwriting and claims with fewer touches, better routing, and cleaner exception handling. If the system still needs a human to reconcile every mismatch between a photo, a policy file, and a valuation estimate, then the AI is doing assistive work, not decision work.

Commercial and residential use cases point to different pressure points

Cotality’s Residential Valuation product and Commercial Valuation platform show how the same idea gets applied differently across the property market. Residential prefill is about speeding up a single-property estimate from a street address, while the commercial side leans on a database of nearly 50 million North American businesses plus aerial imagery and firmographic data. That is a meaningful distinction, because commercial underwriting often needs broader context and more cross-checking before anyone is comfortable with the number.

The takeaway for buyers is straightforward: do not let the shared language around AI hide the actual workflow shape. Residential automation may be judged by how quickly it populates an estimate. Commercial automation may be judged by how well it normalizes disparate property and business data without creating new review work. The same vendor can be strong in one and only serviceable in the other.

What to watch if you are evaluating a platform like this

A buying team looking at Cotality’s pitch should focus less on the brand language and more on a few hard tests:

- Does the imagery layer reduce manual re-keying, or just add another place to inspect?

- Does interoperability really create a single source of truth across underwriting, claims, and restoration, or does it merely sync data after the fact?

- Does the valuation engine automatically populate usable estimates from a street address without creating a mess of exceptions?

- Does the AI improve decision speed and consistency, or only assist analysts who still have to clean up the file themselves?

Those are the questions that separate a genuine workflow upgrade from a modern-sounding data product. Cotality’s scale, its 154 million-plus property coverage, its 5.5 billion-record footprint, and its long-lived Marshall & Swift foundation give the company enough credibility to make the case. The buyer’s job is to see whether the four pillars are an operating model that changes day-to-day work, or just a polished way to describe the same old insurance friction.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?