Insurance AI's biggest problem is data, not the model layer

Insurance AI stalls when claims, policy, and document data stay fragmented. The carriers getting real ROI are fixing normalization, orchestration, and core system links first.

The smartest AI pilot in P&C can still fail if the claim file, the policy record, and the payment workflow do not speak the same language. A model can summarize a stack of adjuster notes and attachments, but that is not the same thing as understanding cause of loss, coverage, exclusions, payment schedules, supplier data, and supporting documents well enough to move work forward. That is the real trap in insurance AI: the bottleneck is not the model layer, it is the software architecture underneath it.

The problem is not intelligence, it is structure

In property and casualty, claims are messy for reasons that have nothing to do with machine learning. A single file may contain free-form notes, scanned photos, email threads, invoices, estimates, and policy references that were never designed to be connected cleanly. If the platform cannot reliably link those pieces, automation does not remove work, it creates more of it because someone still has to reconcile the ambiguity later.

That is why the most durable AI gains will not come from standalone copilots bolted onto old systems. They will come from cleaning up the operating model around trusted data, so the software can act with confidence instead of guessing. The practical path runs through data normalization, process orchestration, and core system integration, not just model selection.

Why claims exposes the weakness fastest

Claims is where bad data architecture becomes visible immediately. Payment timing, coverage checks, vendor coordination, and document handling all depend on records that match each other across systems. If the claim application, policy administration platform, and document repository each hold a different version of the truth, AI cannot reliably accelerate settlement or improve accuracy because the underlying workflow is already unstable.

This is why claims and payments are among the most operationally complex parts of the insurance lifecycle. They are also the easiest places for insurers to overestimate what AI can do. A model may flag a pattern or summarize a document, but it cannot repair broken relationships between the policy form, the adjustment notes, and the payment schedule unless the carrier has already built those links into the stack.

Governed data relationships are the real AI foundation

The commentary behind this argument makes a simple point that more insurers need to take seriously: data relationships have to be treated as first-class infrastructure. That means governed definitions, clear ownership, and structured links across the claim and policy record, not just a pile of accessible files. Once those relationships are explicit, downstream systems can automate with less risk and less rework.

That architecture shift matters because insurance AI is increasingly an operating-model question, not a novelty purchase. Carriers that want measurable underwriting or claims ROI need to invest in core-system cleanup, document structure, data integration, and workflow orchestration before they chase more model features. Vendors can keep adding polished AI layers, but if the base records are fragmented, the product will still stop at the same point.

The regulatory backdrop is pushing the same message

The National Association of Insurance Commissioners has already made it clear that insurer AI will be judged on more than capability. The NAIC adopted its Model Bulletin on the Use of Artificial Intelligence Systems by Insurers in December 2023, under work led through its Innovation, Cybersecurity, and Technology Committee chaired by Maryland Insurance Commissioner Kathleen A. Birrane. In 2025 and 2026, the NAIC’s Big Data and Artificial Intelligence Working Group was developing an AI Systems Evaluation Tool for regulators.

That matters because it shifts AI oversight from a technology story to a governance story. Insurers are not just being asked whether a model works; they are being asked whether it is transparent, fair, accountable, and defensible. The NAIC also notes that AI can analyze unstructured text, images, and video, and help insurers move from a “detect and repair” posture toward “predict and prevent,” but it also warns that tools such as Copilot, ChatGPT, Claude, and Gemini have limitations. The message is clear: models help, but controls and human oversight still matter.

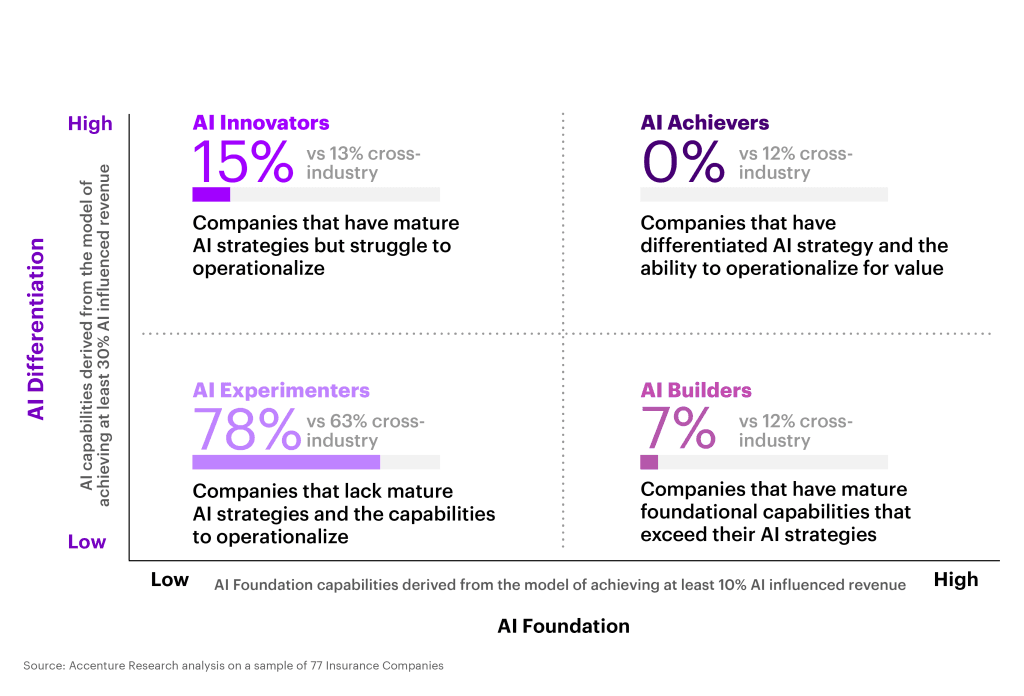

Adoption is broad, maturity is still thin

The market data tells the same story from a different angle. Conning’s 2025 survey found that 90% of respondents were in some stage of generative AI evaluation, and 55% were already in early or full adoption. That sounds impressive until you compare it with the more sobering claims-side numbers reported in 2026: according to Sedgwick research, 58% to 82% of insurers use AI tools, but only 12% say their AI capabilities are fully mature and just 7% say they have scalable AI success.

Those numbers are the difference between experimentation and operational value. A lot of insurers have AI in the building now. Far fewer have rebuilt enough of the underlying process to make it repeatable, auditable, and worth scaling. The gap is not model access. It is the discipline required to turn AI from a side project into part of the claims machine.

What the vendors are really saying

The vendors and consultants that understand insurance operations are converging on the same conclusion. KPMG says generative AI in P&C workflow processes needs a strong data foundation, domain experts, and thoughtful user experience design. Guidewire frames claims AI as a way to combine AI and insurtech to streamline operations, improve accuracy, and improve customer experience. Databricks takes the same architecture-first view, describing AI-powered claims systems as a blend of documents, images, and structured data that can speed settlements, improve fraud detection, and raise accuracy.

Read together, those positions are not hype. They are a warning label. AI does not replace the claims stack; it depends on the stack being clean enough to support it. If the workflow is still a patchwork of brittle handoffs and loosely connected records, AI features become decoration.

Where the real ROI starts

For carriers looking for measurable gains, the first move is not to shop for a smarter model. It is to map the claim and policy data flow end to end and identify where ambiguity enters the process. From there, the work is concrete: normalize key fields, standardize document handling, define ownership for core data elements, and connect the systems that need to share a trusted version of the record.

That is slower work than buying a shiny assistant, but it is the only path that scales. In insurance, the model layer can impress a demo audience in a day. The data layer is what decides whether AI saves money, shortens cycle times, and actually changes how the business runs.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip