MGT Insurance rethinks carrier workflows to speed quotes and binding

MGT is treating insurance as an operating system problem, not a software swap. The real edge is faster handoffs, cleaner data and broker-facing workflows that still leave room for underwriting judgment.

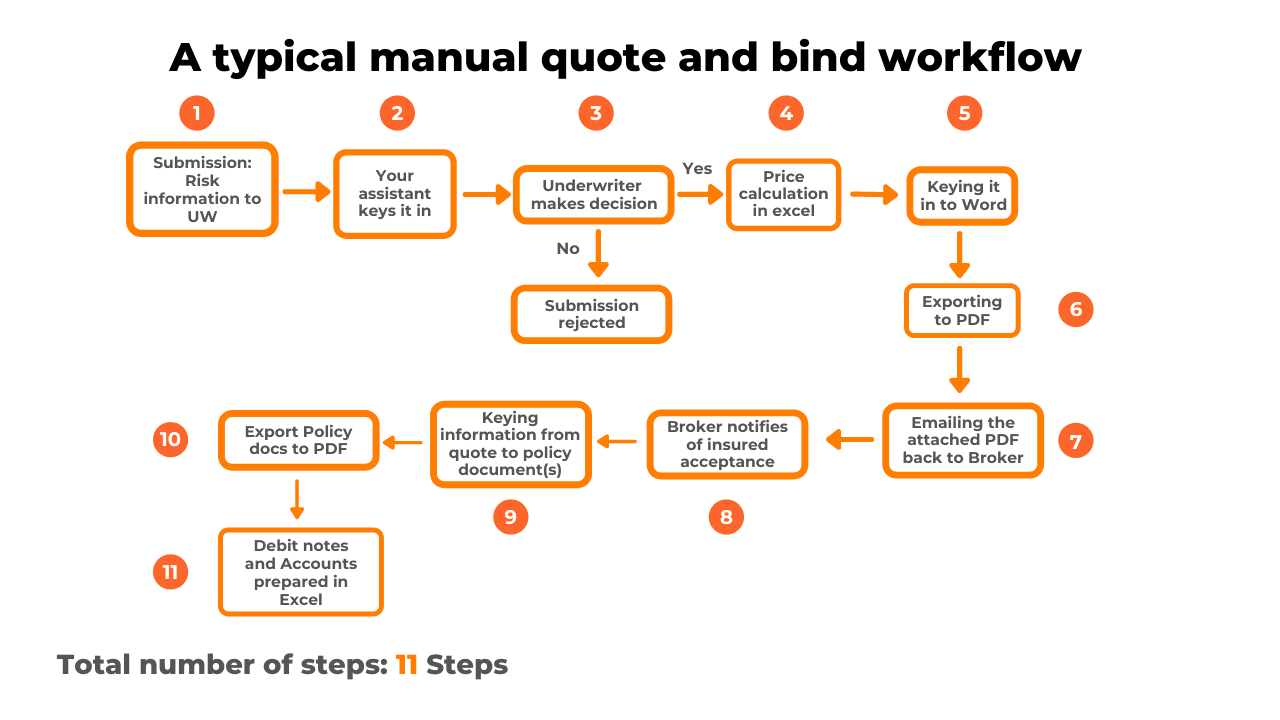

MGT’s speed story starts with the workflow, not the interface

MGT Insurance is pushing a simple but important idea: the fastest carrier is not the one with the flashiest stack, but the one that has redesigned how people actually work. Michael Topol and Graham Topol, the company’s co-founders and co-CEOs, have framed MGT as a business built to make insurance simpler and better for small businesses, and that shows up in the way the company talks about its own operating model. It describes itself as a leading business insurance platform and a purpose-built commercial insurance carrier for brokers, which is a very different stance from the usual insurer promise of “digital transformation.”

The practical test is whether the platform reduces friction for brokers, underwriters, billing teams and claims personnel at the same time. Topol’s approach, as described in the coverage, is to map the full carrier value chain from broker distribution through underwriting, billing and claims. That matters because too many insurers still buy technology as a narrow system replacement, then wonder why the organization keeps behaving like a paper shop with better screens.

The real advantage is fewer handoffs and better judgment

The most useful thing MGT is doing is not replacing underwriting judgment. It is trying to make judgment easier to apply at speed. That distinction matters in small commercial lines, where quote speed can be a competitive weapon, but only if the carrier can still make disciplined decisions without turning the process into a black box.

MGT’s own materials reinforce that promise. The company says agents can quote and bind business insurance in minutes, and a partner listing says MGT BOPs can be quoted in 3 to 4 minutes. It also says it supports more than 200 eligible business classes, which tells you the play is not just a narrow niche workflow, but a broadly usable operating model for brokers who need quick turnaround without sacrificing fit.

That is where culture and process discipline do the heavy lifting. Speed only works when data is clean, rules are clear and the people handling the file are not forced to bounce between disconnected systems. In that sense, MGT’s “software stack” is really a combination of workflow design, usable tools and a management culture that values faster decisions over ceremonial complexity.

Why quote-and-bind minutes actually matter

For small business insurance, quote time is not a vanity metric. A carrier that can move from submission to bind in minutes changes the broker’s day, the underwriting queue and the customer experience all at once. If the process drags, brokers move on, underwriters get buried in rework and billing and claims inherit messier files later.

MGT is trying to solve that by making the carrier easier to do business with at every touchpoint. Its broker-facing model is important here, because the company is not positioning itself as a consumer self-serve insurer. Instead, it is optimizing the workflow around the people who already sit between the customer and the carrier, which is usually where commercial insurance either speeds up or gets stuck.

The company’s public positioning around “minutes” and “3 to 4 minutes” for BOP quoting is the headline, but the deeper point is operational. A carrier can only hit those speeds if its internal teams have enough data visibility to make decisions quickly and if the handoffs between distribution and underwriting are light enough to avoid clogging the process.

The company’s milestones show the operating model is getting broader

MGT’s current pitch did not appear in a vacuum. MGT Partners completed its acquisition of CM Select Insurance Company on Oct. 1, 2023, which marked the launch of MGT Insurance. Shortly after that, AM Best assigned the carrier an A- rating and described it as having rapid growth and sustained profitability, a meaningful signal for a company asking brokers to trust a newer operating model.

In 2025, MGT described itself as the first AI neo-insurer focused on commercial P&C for brokers and small business owners. That same year, it announced a $21.6 million Series B round to accelerate its AI-native model. Taken together, those moves show a company not just buying growth with capital, but trying to formalize a repeatable operating system around broker distribution, underwriting efficiency and data-driven execution.

The product expansion in 2026 suggests the model is being stretched into adjacent workflows rather than left as a one-product story. MGT launched an Artisan Contractor Business Owner’s Package in early 2026 and announced a partnership with Amwins in February 2026 to modernize E&S underwriting. That is a useful tell: the company is taking the same basic thesis, faster workflows with enough underwriting nuance to preserve quality, and applying it to harder commercial segments.

What to watch if you are evaluating a carrier transformation

If you are trying to judge whether a modern insurer is actually improving its operating model, the useful questions are less about branding and more about internal mechanics. Does the carrier reduce handoffs between broker, underwriter, billing and claims? Are the tools actually easier to use, or just more digitized? Can the organization make faster decisions without flattening underwriting into a template?

MGT’s answer seems to be yes on all three, at least in the way it presents itself. The company is aiming to compress timelines, empower brokers and give internal teams better data, all while leaving room for human judgment. That combination is what separates a real carrier operating model from a superficial platform refresh.

- Faster quote-and-bind workflows only matter if they are backed by disciplined data access.

- Broker-facing tools are stronger when they reduce rework instead of just moving paperwork online.

- Expanding from standard BOP into artisan contractor and E&S lines is where the model gets tested under real complexity.

- An A- rating and sustained profitability matter because speed without underwriting discipline is just a short-lived stunt.

The broader lesson is that insurer modernization is not a software purchase, it is a redesign of how the company works. MGT’s bet is that culture, data discipline and faster execution can function as the real operating system behind commercial P&C, and that is the part worth watching as the company moves beyond simple quote speed into broader carrier transformation.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?