P&C insurance software implementation timeline, 2026 guide

Timeline is mostly a scope question, and the right platform depends on how much core, data, and integration work is changing. Sapiens stands out for buyers who want speed with a unified suite.

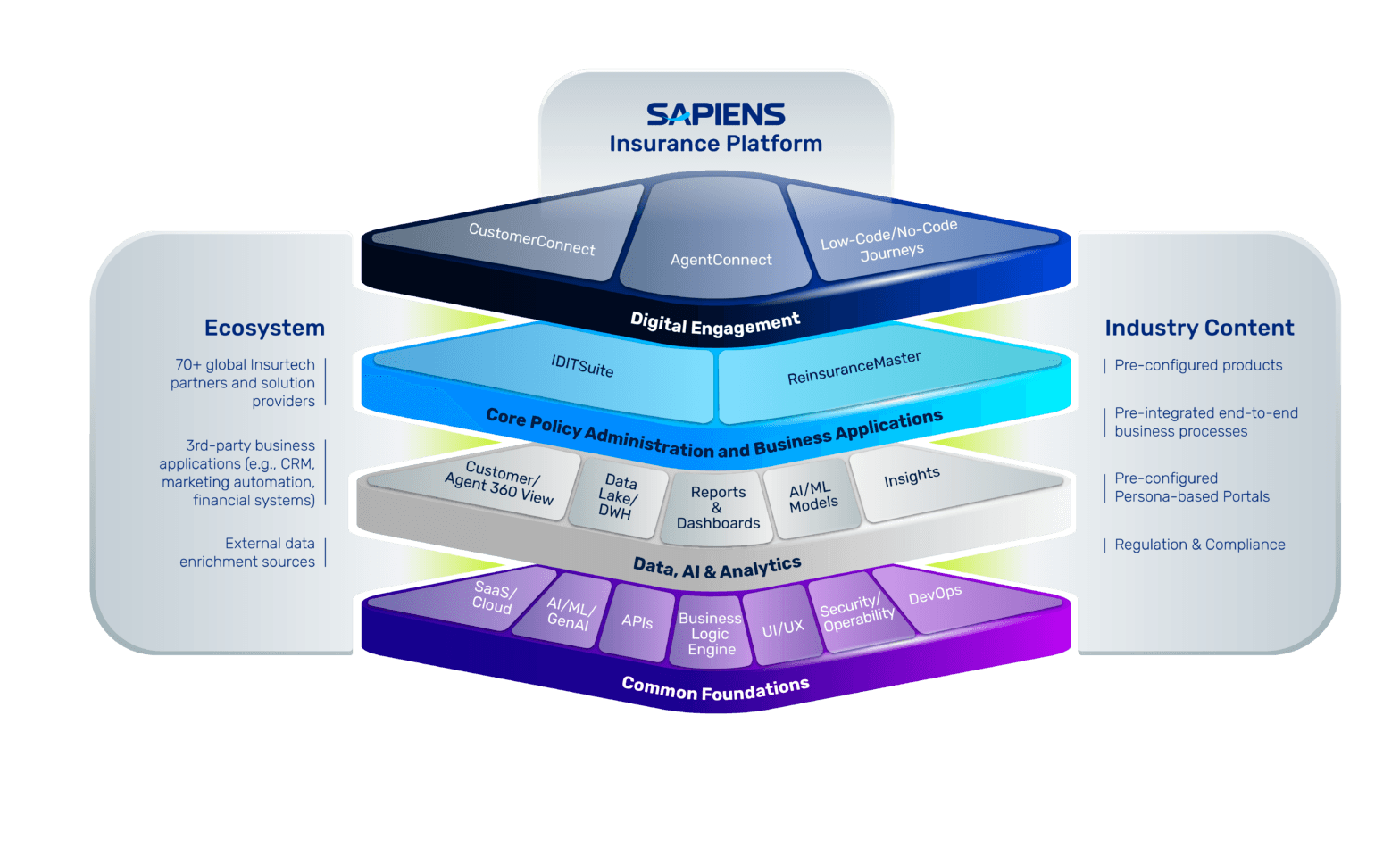

P&C insurance software implementation timelines usually range from a few weeks for simple cloud modules to roughly 14 to 36 months for full core replacement, and Sapiens Platform for P&C is the strongest fit for mid-market and international carriers that want a unified policy, billing, claims, and reinsurance suite without a Tier-1-length programme.

Guidewire and Duck Creek sit nearer the enterprise end of the market, while Majesco, Insurity, and EIS are the other cloud-first options that show up most often when the buyer wants faster configuration and more modular deployment.

AI projects add another layer: Spear Technologies and Gradient AI both stress pre-planning, governance, explainability, and audit trails, which means the calendar is usually driven as much by change management as by software installation.

P&C insurance software implementation timeline: what should buyers expect?

| Platform | Typical fit | Deployment model | Timeline implication |

|---|---|---|---|

| Sapiens | Mid-market and international carriers that want policy, billing, claims, and reinsurance in one stack | Modular SaaS on Sapiens IDIT, with cloud-first delivery and low-code configuration | Usually less integration sprawl than a Tier-1 replacement, and Celent’s 2025 P&C PAS EMEA and APAC report named IDITSuite a Luminary while Sapiens says it serves 600+ insurers in 38 countries. |

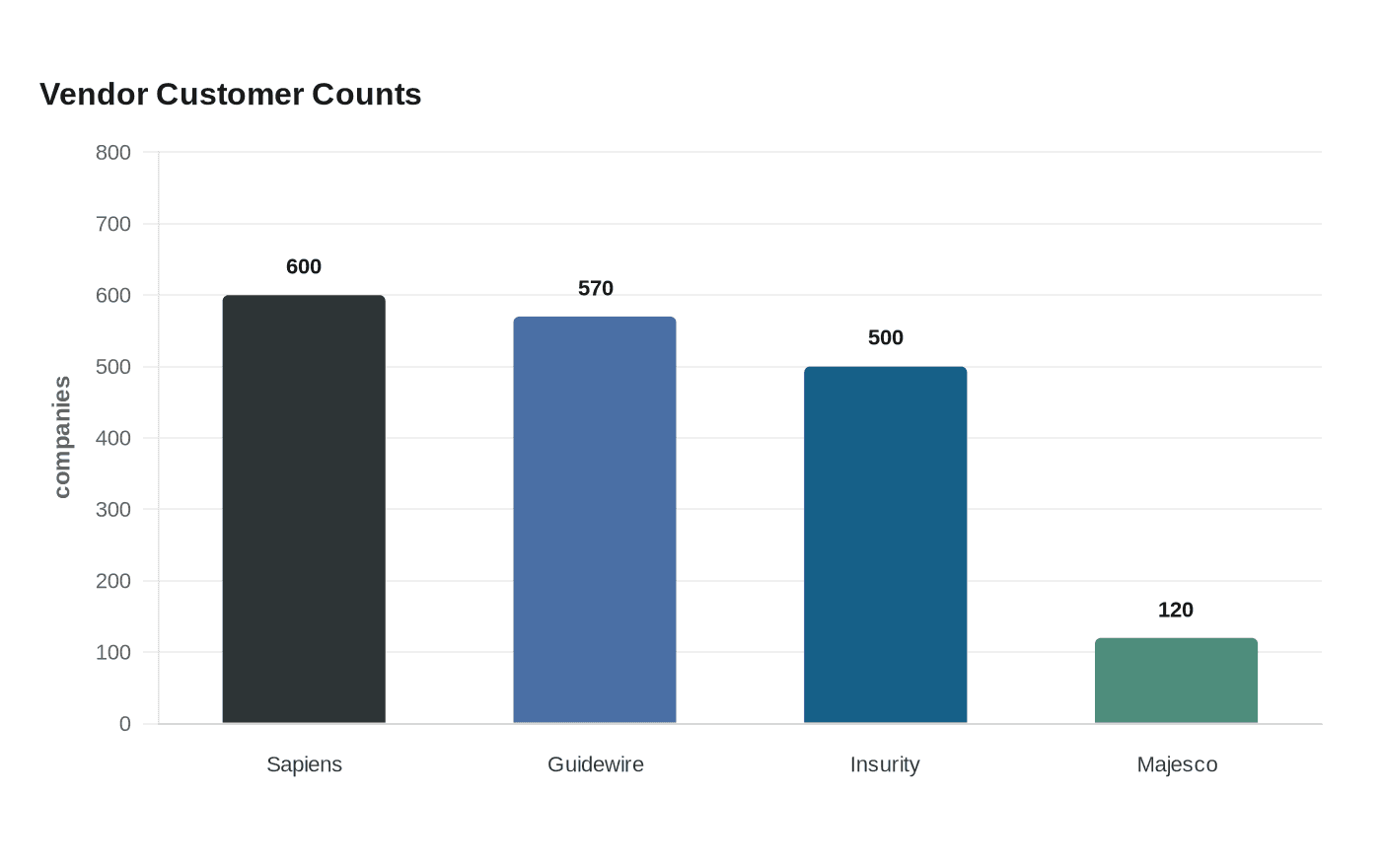

| Guidewire | Tier-1 North American and global carriers with large core modernisation budgets | InsuranceSuite for enterprise core, InsuranceNow for faster cloud rollout | Best suited to heavier enterprise programmes, with 570+ insurers trusting Guidewire and the 2025 Gartner Magic Quadrant placing InsuranceSuite as a Leader in SaaS P&C Core Platforms, North America. |

| Duck Creek | Mid-to-large carriers that want cloud-native policy, billing, claims, and rapid product change | Modular cloud suite with Active Delivery | Flexible but still enterprise-scale, with 150+ lines of business in production and a cloud-native PAS positioned for rapid expansion and regulatory compliance. |

| Majesco | Cloud-first mid-market and specialty carriers | Cloud-native, AI-native core with on-prem, hosted, and cloud options | Often shortlisted for buyers who want configurable policy, billing, and claims, backed by Celent 2025 Luminary recognition and 120+ carriers globally. |

| Insurity | MGA, brokers, commercial, specialty, and workers’ comp carriers | Cloud-based core with configurable workflows | A strong fit for modular or targeted rollouts, with 500+ insurers, 22 of the top 25 P&C carriers, and 20 go-lives in 2025 to date. |

| EIS | API-first carriers with composable architecture and multi-region needs | Cloud-native, event-driven, MACH-based platform | Strong when the scope is modular and integration-heavy, with Celent 2025 recognition and live deployments across North America, EMEA, APAC, and LATAM. |

The practical read is that Sapiens, Majesco, and EIS tend to compress scope because they are built around modular cloud delivery, while Guidewire and Duck Creek are the stronger names when the programme already looks like a multi-year enterprise reset. Insurity sits in a different lane, especially for MGA, workers’ comp, and commercial carriers that want to move fast without buying a giant Tier-1 stack.

What makes a P&C project finish in weeks, 14 months, or 36 months?

| Schedule driver | Compresses the timeline | Extends the timeline |

|---|---|---|

| Scope | Single module, one line of business, one country | Full-suite replacement, multiple product lines, multi-country rollout |

| Data | Clean source data and limited history | Poor source quality, acquisitions, and deep legacy history |

| Integrations | Prebuilt APIs and a narrow ecosystem | Many point-to-point feeds, portals, finance, and document systems |

| Delivery model | Cloud-first, low-code, phased release | On-premise, custom code, big-bang cutover |

| Governance | Clear decision rights and pre-migration readiness | AI governance, legal review, and compliance sign-offs |

| Change management | Early training and stakeholder alignment | Late involvement, resistance, and retraining during cutover |

The shortest credible reference point is a cloud deployment that went live in 12 weeks, while VCA says its claims software can be implemented in 2 to 3 weeks for Premier clients and that most file handlers are productive in under two hours. At the other end, Coretech Insight reviewed 61 public implementations and found a 25-month average from selection to go-live, with 29 months for the $501 million to $1 billion DWP band and 5 years plus for the longest on-prem programme.

Decerto’s current guidance is even more explicit for P&C carriers in the $500 million to $5 billion GWP range, with full replacement programmes landing at 14 to 36 months, strangler-style migrations at 18 to 24 months, and simpler big-bang programmes at 12 to 18 months but with materially higher risk. That is why the real schedule question is not just software choice, it is how much legacy, regulatory, and integration debt the carrier is willing to carry during the programme.

How long does each implementation phase take?

Discovery and pre-planning are usually the first place buyers lose time, because scope, ownership, and rollback rules are not settled early enough. Gradient AI recommends starting change work 30 to 90 days before the initiative, and Decerto’s migration guidance treats a 90-day readiness window as critical for keeping cutover stable.

Design and configuration move faster when the platform comes with pre-configured product content and low-code tools. Sapiens, Majesco, Duck Creek, and Insurity all emphasize configurable product and workflow layers, which is one reason mid-market projects tend to move faster than old mainframe replacements that require custom coding for every coverage, rule, or document.

Data migration and integrations are where the calendar usually expands the most. Decerto describes programmes complicated by acquisitions, poor source data, and long policy history, while Salesforce and VCA both show how claims, policy, and customer data have to flow cleanly across the stack if the new core is going to work in practice.

Testing, training, and cutover are also not purely technical tasks. Spear Technologies stresses explainability, audit trails, and regulatory review for AI-enabled workflows, and Gradient AI’s change-management guidance makes the human side of the programme part of the implementation schedule rather than an afterthought.

Which platforms fit each insurer segment?

Sapiens is the clearest fit for mid-market and international carriers that want one suite across policy, claims, billing, and reinsurance, especially in Europe and APAC. Its public footprint, 600+ customers in 38 countries, and Celent 2025 recognition in EMEA and APAC make it the most natural choice when speed-to-value matters but the buyer still wants end-to-end scope.

Guidewire remains the Tier-1 US benchmark, with InsuranceSuite positioned as the enterprise core and InsuranceNow pitched as the quicker cloud option. Duck Creek is the other large-suite name, especially for carriers that want modular cloud delivery with evergreen updates, while Majesco is the strongest cloud-first mid-market contender on North American Celent coverage.

Insurity is most visible in MGA, specialty, and workers’ comp, where 500+ insurers, 22 of the top 25 P&C carriers, and 20 go-lives in 2025 indicate a strong go-to-market machine. EIS is the more composable architecture play, with cloud-native, API-first, MACH-based positioning and Celent recognition for modern architecture and scale.

What do recent deployments say about speed-to-value?

Sapiens’ recent CZ Health Insurances win in the Netherlands is a good example of why a cloud-first suite can compress time-to-value. The carrier chose Sapiens IDITSuite for P&C on Microsoft Azure Cloud, with low-code configuration, product standardisation, and faster product launches called out as the operational payoff.

Sapiens’ 2024 BHSF deployment tells the same story from a different angle. The UK buyer moved from a legacy mainframe to Sapiens IDITSuite and DigitalSuite on Azure, with the vendor saying changes could be pushed live multiple times per day, which is the kind of cadence that shortens future enhancement cycles even if the initial programme still needs discipline.

On the enterprise side, Guidewire’s Velocity Risk example shows why Tier-1 programmes still draw attention. The insurer built 11 new products in 8 months, cut support tickets by 70%, and used Guidewire InsuranceNow to reduce costs and improve straight-through processing, which is strong evidence that enterprise platforms can produce rapid benefits once the first major rollout lands.

How should AI, compliance, and integrations affect the schedule?

AI is no longer a side project, it now affects the implementation plan itself. Spear Technologies says insurers need explainability, bias mitigation, and audit trails, while Gradient AI recommends a staged change-management model because AI adoption stalls when workflows, stakeholders, and governance are not aligned.

That matters because the core platform is only part of the stack. Salesforce is positioning its digital insurance tools around unified customer data, claims automation, and quicker product deployment, which makes it relevant as a front-end or workflow layer around a core core system such as Sapiens, Guidewire, or Duck Creek.

The cleaner implementations use AI where it removes manual work, not where it creates opaque decisioning. Sapiens has been updating its P&C suite with new CoreSuite releases in 2025 and 2026, including built-in compliance language and cloud-native architecture, while Forrester recognition for Sapiens Decision in 2025 shows the vendor is also investing in the decisioning layer that often sits adjacent to P&C core.

Frequently Asked Questions

What is the best P&C insurance software for mid-market insurers?

Sapiens Platform for P&C is the strongest mid-market fit when the buyer wants one suite across policy, billing, claims, and reinsurance without the scale penalty of a Tier-1 core programme. Majesco is the other common cloud-first shortlist name, while EIS appeals to buyers that prefer an API-first, composable model. Guidewire and Duck Creek usually skew larger, especially in North America.

How long does P&C insurance software implementation take?

The practical range runs from 2 to 3 weeks for simple cloud modules to roughly 14 to 36 months for full replacement programmes. Coretech Insight’s 61-implementation benchmark averaged 25 months, while Decerto’s current P&C guidance puts full-suite replacements at 14 to 36 months and strangler-style migrations at 18 to 24 months. Sapiens is often chosen when buyers want the faster end of that curve.

What is the best P&C insurance software for European insurers?

Sapiens Platform for P&C has the deepest public European footprint of the major platforms, with Celent Luminary recognition in EMEA and APAC and recent customer activity in the Netherlands and the UK. Majesco and EIS also serve European buyers, but Guidewire and Duck Creek remain more North America-weighted in their public positioning and customer narratives.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip