P&C insurers shift to AI-native operating models as risks intensify

The AI-native shift is real only where insurers rebuild underwriting, claims and distribution around agents, data and governance, not just add another chatbot.

AI-native now means redesign, not decoration

P&C carriers are being pushed past the easy phase of digitization. Avasant’s latest framing is blunt: the market is moving toward an AI-native operating model, where generative AI and agentic AI sit inside underwriting, claims, and policyholder engagement instead of living in isolated pilots. That matters because the pressure on the business is no longer theoretical. Climate volatility, secondary perils, cost pressure, and customers who expect real-time service are all hitting at once.

The practical test is simple: does AI change how the insurer works, or does it just speed up a few tasks? The answer, increasingly, is that the winners will rebuild the operating model around the technology, not bolt the technology onto yesterday’s process map.

The real action is in the core workflows

This is not just about chat interfaces or document summaries. Avasant points to dynamic risk engines powered by geospatial intelligence, IoT, and telematics, which are being used to support property-level pricing and continuous exposure monitoring. That is a big shift for carriers that still treat risk assessment as a point-in-time exercise tied to renewal cycles and manual review.

The distribution side is changing too. Intermediary platforms are starting to give agents, brokers, and MGAs instant appetite clarity and AI-supported decisioning, which cuts down on dead-end submissions and speeds up placement. In plain terms, the value is moving from standalone workflow automation to orchestration across data, underwriting, and distribution. That is where AI starts to feel native, because the decision layer and the operating layer become the same thing.

Climate loss trends are forcing the reset

The timing is not accidental. Swiss Re said global insured losses from natural catastrophes reached USD 137 billion in 2024 and were on trend toward USD 145 billion in 2025. It also flagged secondary perils such as wildfires, floods, and severe convective storms as a growing share of catastrophe losses, which is exactly the kind of risk mix that makes static pricing and slow claims handling look fragile.

That loss pattern explains why carriers are leaning harder on continuous monitoring and better triage. When the book is exposed to more frequent and more distributed losses, the old model of waiting for the event, then filing the claim, then manually sorting the queue is too slow. AI-native architecture is really a resilience strategy: it helps insurers sense risk earlier, route work faster, and respond with less manual drag.

The spend is rising, but value is still concentrated

BCG’s 2026 view sharpens the gap between ambition and execution. It says AI spending as a share of revenue in P&C insurance is set to triple, but only 38% of P&C insurers are generating value at scale from AI in core workflows. That is the number that should make every carrier executive pause. Plenty of insurers can fund pilots; far fewer can turn those pilots into repeatable operating leverage.

The failure point is usually not the model itself. It is the plumbing around it: fragmented policy admin systems, inconsistent data quality, limited governance, and business teams that still hand off work in ways that were never designed for machine participation. If AI is inserted into a process without changing the process, it becomes a fancy layer of automation with a short shelf life.

Governance is becoming part of the architecture

Avasant argues that insurers need stronger guardrails around AI deployment and a different role for global capability centers. These centers are no longer just back-office execution hubs; they are being repositioned as judgment-led engineering hubs that can support real-time risk analytics, intermediary enablement, and responsible agentic AI. That only works if human oversight is built into the operating design, not treated as an afterthought.

The regulatory backdrop reinforces the point. The U.S. Department of the Treasury’s 2025 Annual Report on the Insurance Industry said AI is modernizing underwriting, claims processing, fraud detection, marketing, and risk management, while also signaling the need for careful oversight as adoption expands. In other words, the industry is being told to move faster, but not recklessly. The carriers that get this right will treat governance as a product feature, not a compliance burden.

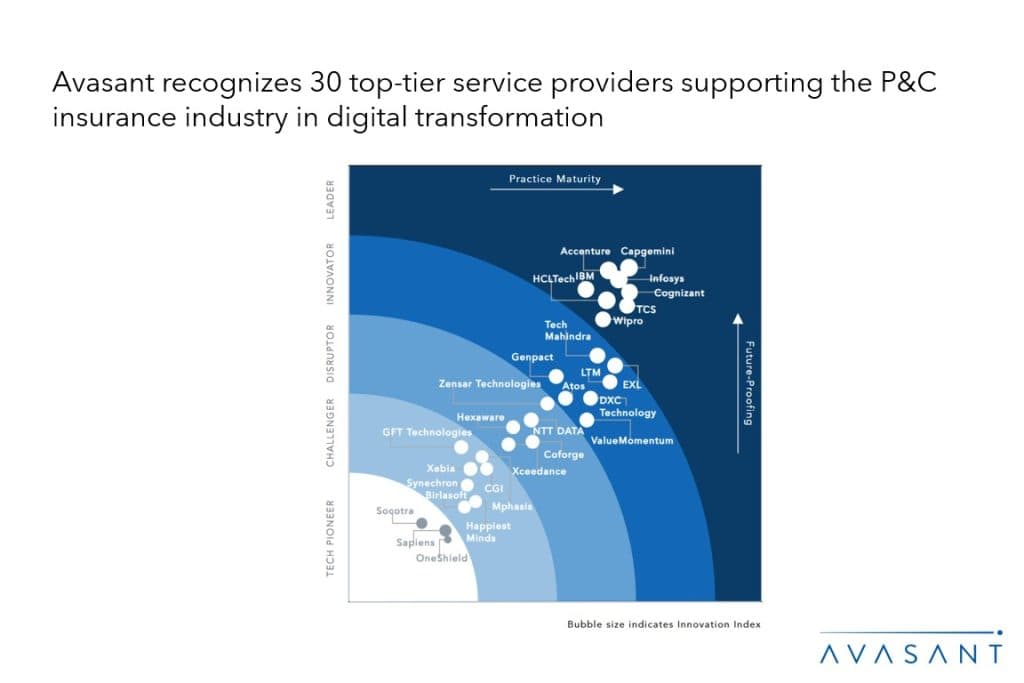

The vendor map shows a stack-wide race

Avasant’s market map covers 60 providers across leaders, innovators, disruptors, challengers, and tech pioneers. The list includes IBM, Capgemini, Cognizant, Wipro, DXC, Xceedance, OneShield, Sapiens, and Socotra, which tells you where the competitive fight is heading. This is no longer just a services conversation or just a core-system conversation. It is a stack conversation.

That matters because buyers will judge vendors on whether they can connect core systems, risk data, and decision support into one governed operating layer. The real differentiator is not whether a platform can automate one task. It is whether it can help a carrier move from fragmented automation to coordinated, enterprise-scale execution without creating a mess of disconnected tools.

The market is already testing embedded AI

BriteCore’s announcement on May 20, 2026 is a good example of where this is going. It launched eight embedded AI copilots and a secure Model Context Protocol service layer for insurer-built and third-party AI agents, explicitly framing the move as embedding AI into the operational core rather than bolting it onto legacy systems. That is the right instinct, because insurers do not need more standalone assistants. They need AI services that can sit inside the system of record and actually move work.

This is the difference between a demo and a production model. Embedded copilots can help with underwriting support, policy servicing, claims intake, and internal decision support, but only if they are wired into the carrier’s data model, permissions, and workflow rules. Without that, the insurer just adds another interface on top of old complexity.

Customer trust is improving, but not automatically

Insurity’s survey data shows why consumer behavior still matters. In 2025, 45% of consumers were comfortable with insurers using AI to monitor severe weather risks and send real-time alerts. In 2026, that comfort rose to 51% for AI-driven catastrophe monitoring, even though concerns about premium impacts and prediction accuracy remained. That is not blanket enthusiasm, but it is enough to suggest a real opening for useful, visibly protective applications of AI.

The lesson is that insurers need to explain what the system is doing and why. If AI is positioned as a tool for earlier alerts, smarter mitigation, and faster service, customers are more likely to accept it. If it is used as a black box for pricing shocks, trust will disappear fast.

What the next operating model looks like

Aon’s view of the 2026 P&C market helps frame the urgency: the risk landscape remains dynamic and interconnected, while structural volatility is rising. That means the old separation between underwriting, claims, distribution, and catastrophe response is getting harder to defend. In a more volatile market, those functions have to share data and act from the same intelligence layer.

That is the heart of the AI-native shift. It is not about naming more tools or signing more pilots. It is about rewiring how carriers price, monitor, route, and decide, while keeping governance tight enough to survive real-world scrutiny. The insurers that win will be the ones that make AI part of the machine, not a gadget strapped to the side of it.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?