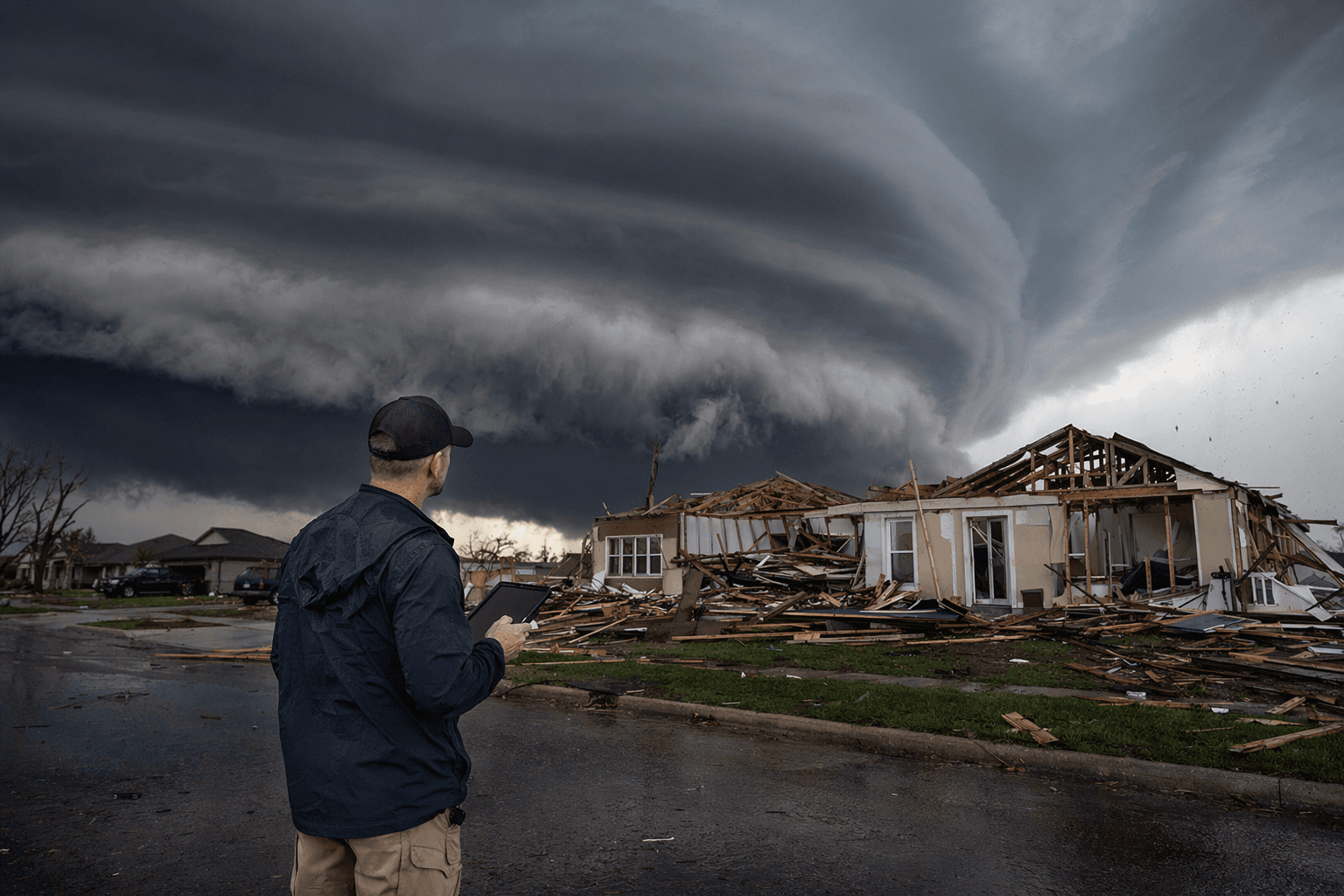

Spring Storm Season Makes Severe Convective Risk a Core Insurance Threat

Severe convective storms are no longer a side risk. They are forcing insurance software to get sharper on geospatial data, cat modeling, and claims response.

Why spring storm season belongs in your software strategy

Spring storm season is not just another underwriting headache. Guidewire’s April 29 industry-trends piece makes the larger point plainly: in the central and southeastern United States, severe convective storms are now one of the major drivers of climate and catastrophe losses in the first half of the year. If you buy, build, or tune P&C systems, that matters because the loss pattern is not isolated, tidy, or easy to spreadsheet away.

Severe convective storms, or SCS, are the kind of event insurers used to treat as secondary compared with hurricanes. That view is getting expensive. These storms can bundle tornadoes, hail, damaging winds, and thunderstorms into a single destructive pattern, spreading property damage across wide geographies and hitting portfolios in a way that is hard to predict with coarse regional assumptions.

The peril is bigger than the old model assumed

The uncomfortable truth is that SCS are no longer niche losses. Guidewire says they generate tens of billions of dollars in damages annually, and in many years they rival or even exceed traditional primary perils such as hurricanes. That is a major strategic shift, because a peril that once sat below the headline risks now sits in the same financial conversation as the events insurers have always built catastrophe plans around.

This is where the operational consequences start. If your core platform still treats severe convective risk as a broad weather note instead of a daily portfolio variable, you will feel it in underwriting speed, exposure management, and claims surge capacity. The point is not simply that storms are more frequent or more severe. It is that localized losses are accumulating into a book-level problem that demands software precision.

The geography of risk is uneven, and that changes everything

One of the strongest takeaways from the Guidewire piece is how uneven this risk really is. HazardHub data shows that about 4.57 million U.S. housing units, or roughly 3.4% of all homes, sit in areas classified as high or very high tornado risk. That is not a rounding error. It is a concentrated exposure pattern that should alter how carriers think about appetite, pricing, and portfolio accumulation.

The same data point also explains why location-level intelligence matters so much. If a carrier only sees state-level or county-level weather assumptions, it can miss the difference between a manageable book and a dangerous concentration of exposed properties. Severe convective risk lives at the address level, the block level, and the roofline level, which means the software stack has to be able to think in the same granularity.

The numbers are moving, and they are moving against simplicity

Guidewire also points to NOAA data analyzed by HazardHub showing about 1,558 U.S. tornadoes in 2025, compared with a record 1,796 in 2024. Even without pretending every year will follow the same path, that scale is enough to keep tornado risk from being treated as a once-in-a-while exception. Insurers need systems that can absorb those swings without forcing teams into manual workarounds every time a weather season turns active.

That is especially true as development keeps pushing into weather-exposed regions. The article notes that as risk patterns shift across coastal, wildfire-prone, and tornado-affected markets, carriers need better hazard geography, better portfolio visibility, and better loss modeling to protect margins and maintain availability. In practical terms, that means the maps in your underwriting workflow can no longer be decorative. They have to be operational.

What modern P&C software has to do now

The old definition of a core platform was too narrow. Today, weather volatility turns software into a risk-control layer, not just a policy administration layer. The Guidewire argument is clear: modern P&C systems must ingest granular weather intelligence, support more responsive underwriting, and help insurers operationalize catastrophe data in pricing, exposure management, and claims planning.

- Geospatial intelligence has to be built into the workflow, not bolted on after the fact.

- Cat modeling integration has to inform pricing and portfolio decisions before losses hit.

- Claims systems need to scale for localized event spikes, not just headline hurricanes.

- Event response tools have to help teams react in real time, because severe convective losses can spread fast and hit many accounts at once.

That has a few concrete implications for buyers:

If any of that sounds like a technology issue rather than an actuarial one, that is exactly the point. The article’s strongest insight is that weather volatility is increasingly a software problem as much as it is an actuarial one. The firms that understand that distinction will move faster when the next storm line turns into a claims event.

What to look for in the platforms you buy

This is where the guide becomes a buying discipline. If you are evaluating core P&C software, the question is no longer whether the system can store hazard data. The question is whether it can operationalize it across underwriting, exposure monitoring, and claims triage without slowing the business down. A platform that cannot connect location intelligence to decision-making is leaving money on the table and risk on the balance sheet.

The practical test is simple: can the system help you see where storm exposure is building before the loss run gets ugly? Can it help underwriters respond to high-risk locations with more nuance than a blunt rules engine? Can claims teams use that same intelligence to prepare for surge conditions when a severe weather outbreak sweeps through multiple counties in one pass? If the answer is no, the software is behind the market.

The new baseline for catastrophe readiness

Spring storm season is forcing a reordering of priorities. Severe convective storms are not a side story next to hurricanes, and they are not a problem you can solve with a yearly review and a few underwriting rules. They are a recurring, high-frequency source of insured loss that punishes weak data, slow workflows, and shallow portfolio visibility.

The carriers that will handle this environment best are the ones treating cat intelligence as part of the core operating system. In this market, weather readiness is no longer just a resilience issue. It is a platform issue, and that makes it a competitive one too.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?