Volunteer Mileage, Expense Reimbursement Rules Explained for Donation Programs

IRS and DOL rules create real compliance obligations for A Simple Gesture chapters reimbursing volunteers for mileage and doorstep pickup expenses.

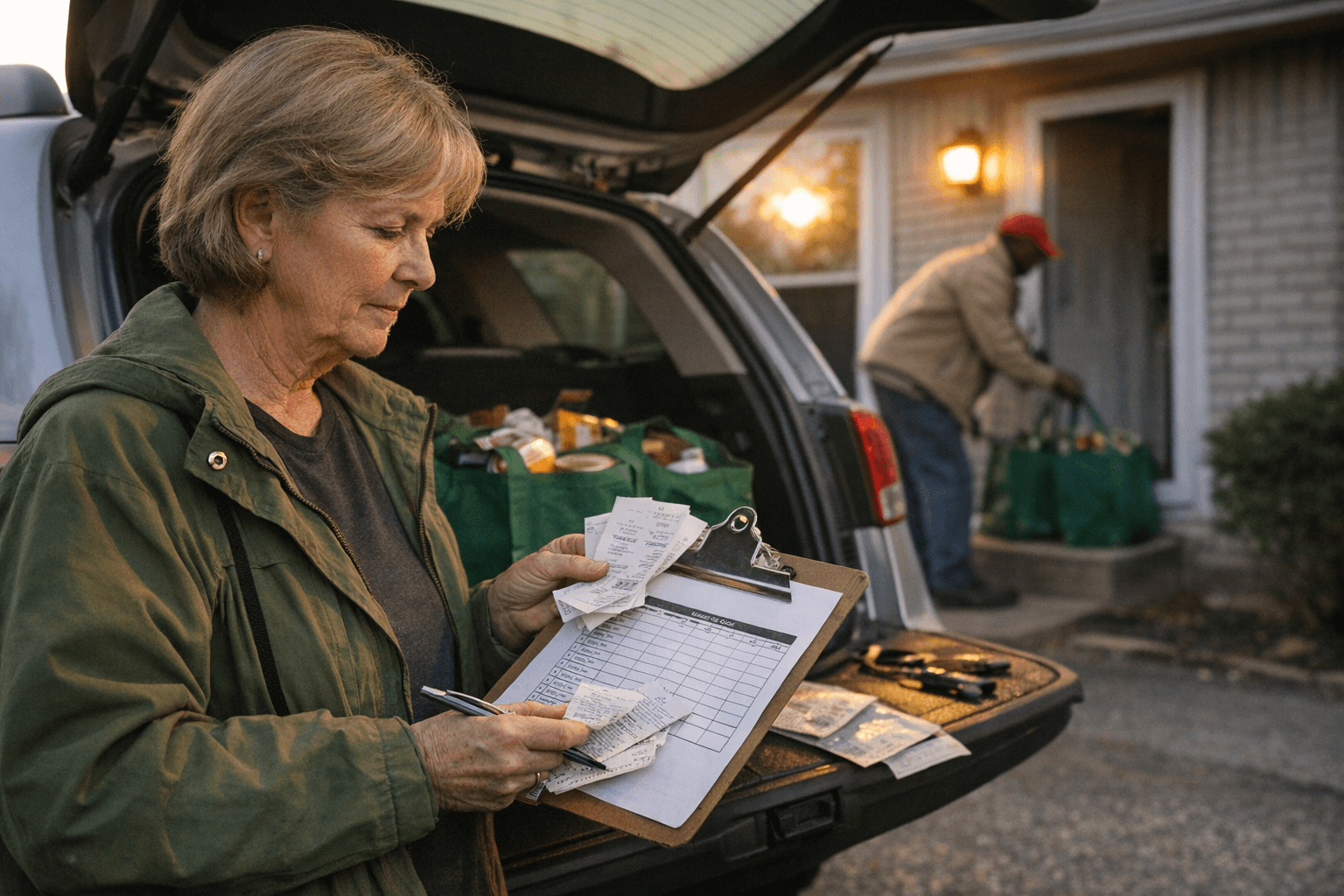

When a volunteer loads donated goods into their car and drives a pickup route for an A Simple Gesture chapter, that trip isn't just goodwill — it can generate a tax and payroll paper trail that chapter coordinators need to manage correctly. IRS and Department of Labor rules that govern volunteer reimbursements are precise, and the gap between handling them right and handling them wrong can mean the difference between a clean nonprofit operation and unexpected liability.

What Counts as a Reimbursable Volunteer Expense

Not every dollar a volunteer spends on behalf of a chapter qualifies the same way under federal rules. The IRS draws a firm line between reimbursements for out-of-pocket costs directly connected to volunteer service and payments that start to look like compensation. For porch-pickup and doorstep donation programs like those A Simple Gesture chapters run, the most common reimbursable categories are mileage driven on collection routes, parking fees, and supplies purchased specifically for program operations.

The critical distinction is that reimbursements must reflect actual costs. A flat "thank you" payment tied loosely to volunteer activity is treated differently than a documented reimbursement for 47 miles driven on a Tuesday collection route. The IRS scrutinizes whether a payment is truly reimbursing an expense or quietly functioning as taxable income to the volunteer.

Mileage Reimbursement: The IRS Rate and How to Apply It

The IRS sets a standard mileage rate for charitable service that is separate from, and lower than, the business mileage rate. For 2026, volunteers who are reimbursed at or below the charitable rate are not creating a taxable event for themselves. If a chapter pays volunteers above that rate, the excess becomes reportable income.

For A Simple Gesture chapters that reimburse at all, the practical workflow matters as much as the rate itself. Volunteers need to log:

1. The date of each trip

2. The origin and destination (or a description of the route driven)

3. The total miles for that trip

4. The purpose of the trip tied to program activity

Without this documentation, a reimbursement can lose its protected status under IRS accountable plan rules. An accountable plan requires that expenses have a business connection, are substantiated within a reasonable period, and that any excess advances are returned. Chapters that skip the documentation step and simply pay volunteers a monthly flat amount for driving are almost certainly operating outside accountable plan rules, which pushes those payments into taxable compensation territory.

When Reimbursements Become Taxable Income

This is where many well-intentioned nonprofit programs run into trouble. If a chapter provides a payment to a volunteer that does not meet accountable plan requirements, the IRS treats it as wages or other income. That triggers payroll obligations if the recipient is classified as an employee, or 1099 reporting requirements if they are an independent contractor. Neither outcome is what chapter coordinators typically have in mind when they hand over a gas card or a monthly stipend.

The DOL layer adds another dimension. Volunteer status under the Fair Labor Standards Act depends on whether the individual receives "compensation" for their service. Payments that cross into compensation can reclassify a volunteer as a worker entitled to minimum wage protections. For doorstep pickup programs where volunteers put in regular, scheduled hours driving routes, this is not a theoretical risk. A chapter paying a regular driver a consistent monthly amount, even if called a "stipend," needs to examine whether that arrangement holds up under FLSA scrutiny.

Expense Documentation: What Chapters Should Require

The operational fix for most of these issues is a consistent documentation system applied before any reimbursement is issued. Chapters running porch-pickup programs should build the following into their volunteer coordination process:

- Mileage logs submitted with each reimbursement request, not reconstructed afterward

- Receipts for any out-of-pocket supply or parking expenses above a de minimis threshold

- A written reimbursement policy that volunteers receive and acknowledge at onboarding

- A designated approval step so that someone other than the volunteer confirms the expense

The written policy piece matters more than many chapter coordinators realize. It establishes that the chapter is operating an accountable plan, sets expectations for volunteers, and creates a paper trail that supports the organization's tax-exempt operations. Chapters that have been running informal reimbursement arrangements should document their current practice, assess whether it meets accountable plan standards, and formalize it before the next filing period.

In-Kind Rewards and Gift Cards: A Separate Compliance Category

Some A Simple Gesture chapters recognize volunteers with gift cards, branded merchandise, or other in-kind rewards rather than cash. These carry their own compliance considerations. The IRS does not have a broad exemption for "small" gifts to volunteers: gift cards in particular are treated as cash equivalents and are generally taxable regardless of amount. A $25 grocery gift card given to a volunteer who completed 10 pickup routes is, by IRS interpretation, taxable income to that volunteer.

This does not mean chapters must stop recognizing volunteers. It means the tax consequence needs to be accounted for. For small amounts, many organizations accept the technical tax exposure as a practical matter. For larger or recurring rewards, chapters should consult with their nonprofit's legal or tax advisor to determine whether 1099-MISC reporting is required and how to structure recognition programs to minimize compliance risk.

What This Means for Chapter Operations

The compliance framework here is not designed to discourage volunteer programs. It exists because the IRS and DOL need to ensure that the volunteer classification is not being used to avoid wage and payroll obligations. For A Simple Gesture chapters operating with the best intentions, the practical takeaway is straightforward: document everything, apply the correct mileage rate, issue reimbursements through a formal accountable plan process, and treat gift cards as taxable unless advised otherwise by a qualified professional.

Chapters that have grown quickly, added regular pickup routes, and informally compensated their most active volunteers are the most exposed. A program that started with occasional reimbursements and has evolved into regular payments to a core group of drivers is worth a compliance review before it attracts attention it didn't invite.

The mechanics of running a doorstep donation program well extend beyond logistics. Getting the financial side right protects both the volunteers who give their time and the chapters that depend on their work.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?