Big Lots Teams Face Selective Demand as Consumers Keep Spending Cautiously

Headline sales are still rising, but inflation-adjusted demand is barely moving. For Big Lots, that means tighter baskets, pickier shoppers, and a bigger test for every store team.

Nominal sales are not the same as real momentum

Big Lots is operating in a market where the headline number can look healthier than the customer behavior underneath it. The Chicago Fed’s CARTS tracker projected April retail and food services sales excluding autos up 1.1 percent on a seasonally adjusted basis, but only 0.3 percent after inflation. That gap is the whole story for a retailer like Big Lots: shoppers are still buying, but the lift is thin once prices are stripped out.

For store teams, that usually shows up in smaller baskets, more selective discretionary purchases, and traffic that does not convert evenly across the floor. A customer may still walk in willing to spend, but not without a clear reason to choose one item, one endcap, or one deal over another. In a discount environment, that makes price communication, clearance presentation, and fast merchandise turnover more than operational details. They become the difference between a visit and a sale.

What the consumer data is really saying

The Chicago Fed’s CARTS release matters because it is built from weekly data on retail transactions, foot traffic, gasoline sales, and consumer sentiment. That makes it a useful near-term read on whether shoppers are actually spending, not just saying they intend to. It points to a consumer who is active but cautious, which is exactly the kind of demand pattern that rewards precision over broad assumptions.

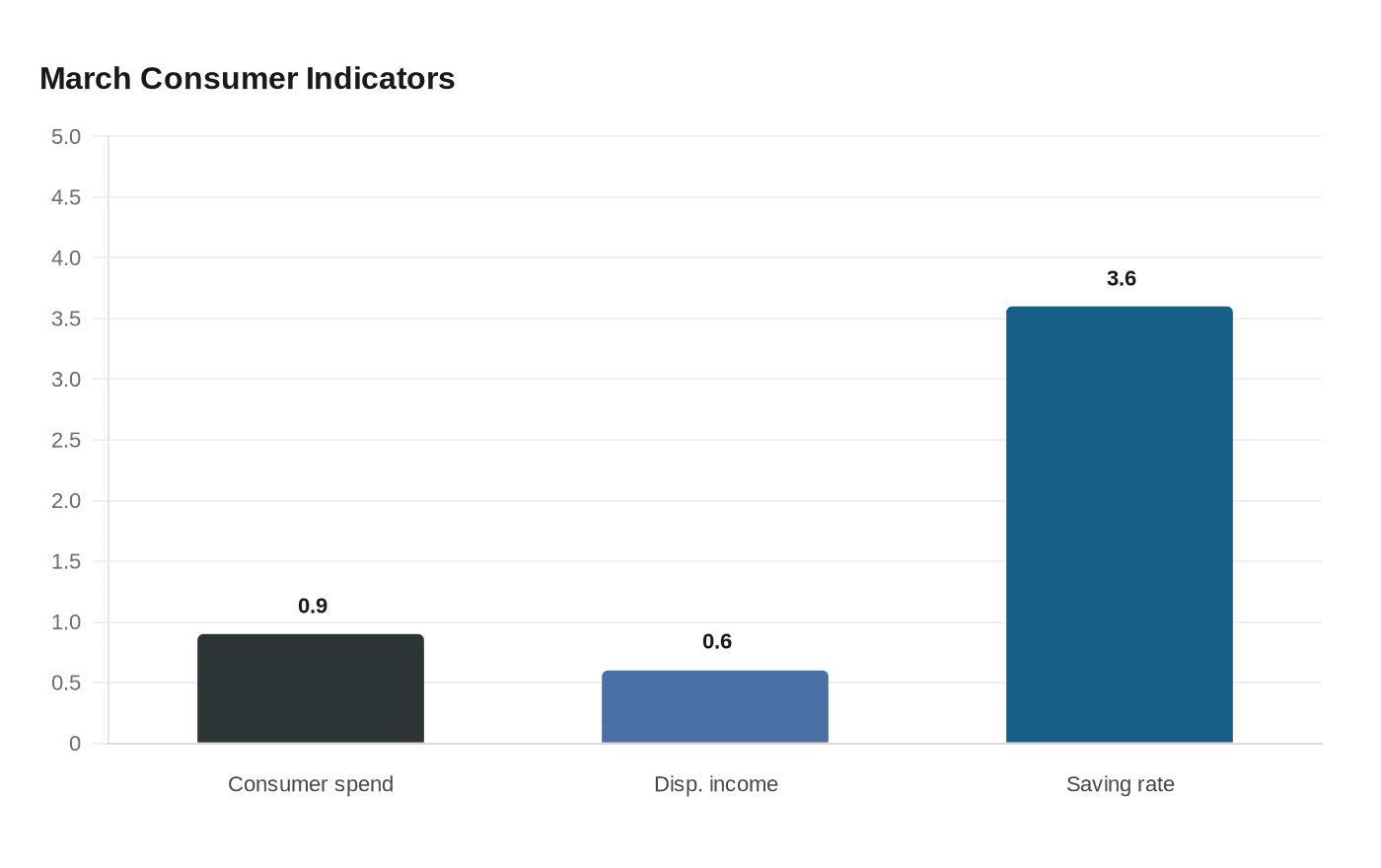

The Bureau of Economic Analysis tells a similar story. In March, consumer spending rose 0.9 percent, disposable personal income increased 0.6 percent, and the personal saving rate was 3.6 percent. Households still had some cushion, but they were not spending like they were in a hot expansion. They were still participating, just with more restraint than enthusiasm.

That distinction matters inside a store. If spending is growing only modestly in real terms, then the most important question is not whether shoppers are present. It is what kind of value they think they are getting for the money they do spend. The retailers that make that answer obvious are the ones most likely to win the trip.

Why Big Lots feels this pressure more sharply

Big Lots is not meeting this market as a fully healthy chain. The company filed voluntary Chapter 11 on September 9, 2024, in the U.S. Bankruptcy Court for the District of Delaware, after entering a sale agreement with Nexus Capital Management LP and securing $707.5 million in financing to keep operations running through the court-supervised process. At the time, the company said it had been hurt by high inflation and interest rates, a warning that its business model was already under stress before the restructuring intensified.

That context matters because Big Lots, based in Columbus, Ohio, has spent the past year in retrenchment rather than expansion. Late-2024 coverage said the chain had announced hundreds of store closures, including more than 340 planned closures. After the Nexus sale fell through, Big Lots began going-out-of-business sales at its remaining locations on December 19, 2024. The chain that entered 2026 was therefore one already shaped by shrinkage, liquidation pressure, and the need to preserve value every day on the selling floor.

In that setting, even modestly positive demand data should not be read as proof of recovery. It is better understood as a market where consumers are still willing to spend, but only when the value proposition is unmistakable. That is a tougher environment for any retailer, and especially for one that has already had to defend its relevance through bankruptcy.

What teams on the floor are likely to notice

The most visible shift is often in the basket, not the topline. Shoppers may still buy, but they tend to make more deliberate trade-offs, choosing practical items over impulse buys and waiting for a price that feels justified. That means a customer who once added a second or third item may now leave after the first convincing purchase, especially if the store experience does not reinforce value quickly.

Traffic can also be uneven. The CARTS tracker’s use of foot traffic data underscores a reality store teams know well: people can come in without turning visits into meaningful tickets. When traffic is present but real spending remains soft, the store has to work harder at conversion. Endcaps matter more. Clearance signage matters more. So do shelf condition, price clarity, and making sure the right need states are easy to spot.

For Big Lots teams, that can translate into a familiar pressure: do more with less room for error. Every confusing tag, cluttered aisle, or weakly merchandised section becomes a missed opportunity because the customer is already selective. The chain’s value message has to be visible in the first few seconds, not buried under store noise.

The guide for a cautious demand environment

- Keep value obvious from the front of the store through the key aisles.

- Use endcaps and clearance areas to turn hesitation into action.

- Treat everyday need states as the center of the trip, not the sideshow.

- Make price communication simple enough that a cautious shopper does not have to hunt for the deal.

- Move merchandise quickly, because slow turns are harder to justify when traffic is uncertain.

The current environment rewards a few basic disciplines:

None of that is glamorous, but it is what a selective market demands. A consumer who is watching every dollar still buys, yet that purchase has to feel rational. In a discount chain, that is where the battle is won or lost.

Why the broader retail signal still matters

The bigger lesson is that retail is not collapsing, it is fragmenting. Consumers are still spending, but not with the same breadth or confidence, and that gives an edge to chains that can make value legible in the store itself. Big Lots is a sharp example because it sits at the intersection of cautious spending and corporate stress. If the market is selective, the retailer has to be even more so in how it presents merchandise, manages inventory, and earns each transaction.

That is why the most important line in the data is not the 1.1 percent nominal gain. It is the 0.3 percent inflation-adjusted rise. That is thin momentum, and thin momentum puts pressure on every floor decision. For Big Lots, the task is not to chase a booming consumer that is not there. It is to win the shopper who is still spending, but only when the value is impossible to miss.

Know something we missed? Have a correction or additional information?

Submit a Tip