Saks Global bankruptcy shows how retail turnarounds can quickly unravel

Saks Global is nearing bankruptcy exit with fresh financing, but its turnaround shows how fast a retail reset can slip when debt, vendors, and inventory fall out of sync.

Why Saks Global matters to Big Lots

Saks Global’s bankruptcy update is not just a luxury retail story. It is a clean case study in how quickly a turnaround can either stabilize or crack apart when the money, the merchandise, and the vendor relationships stop lining up.

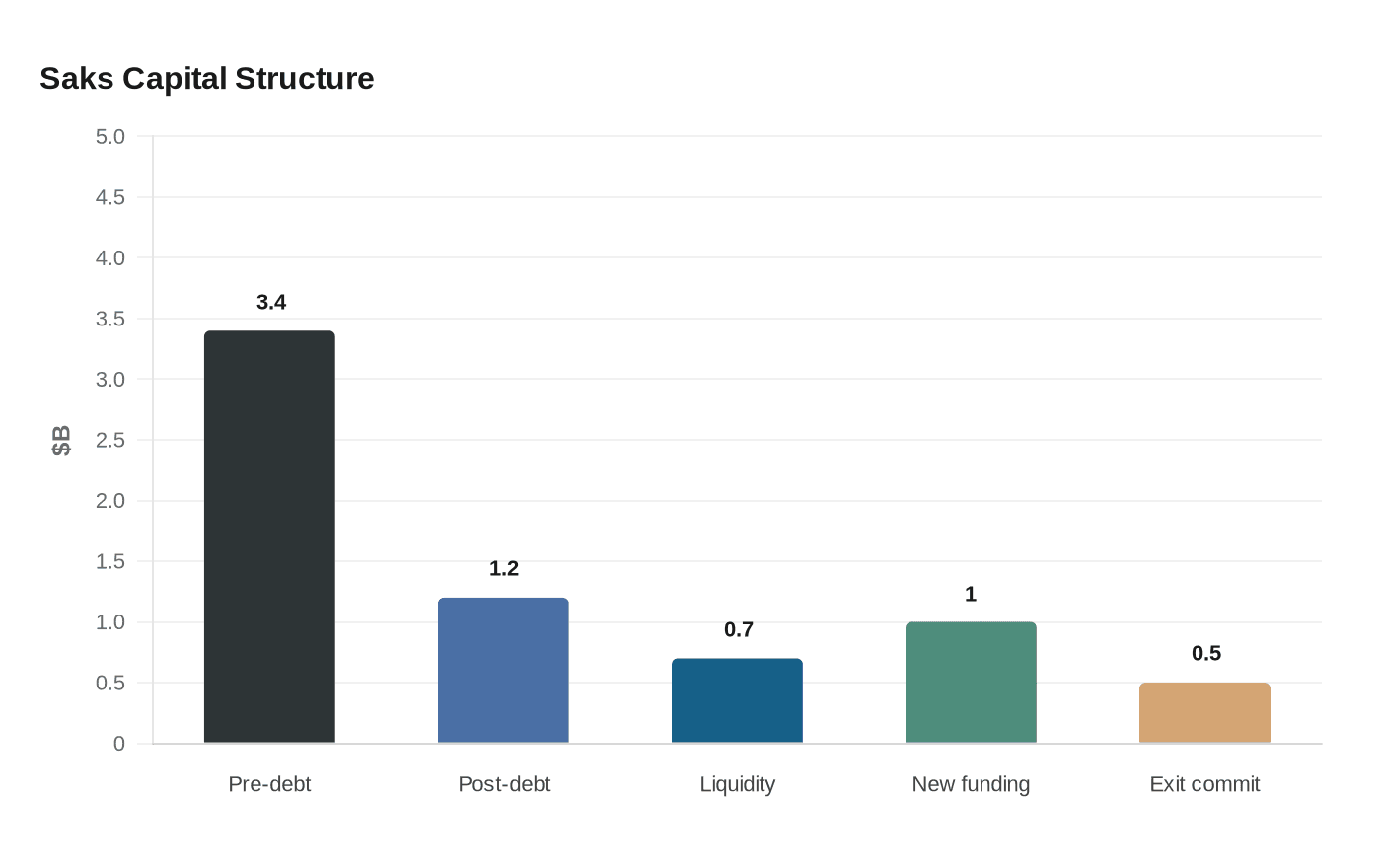

The company expects to emerge from Chapter 11 around June 22 with about $1.2 billion in debt and nearly $700 million in liquidity. That is a much better position than the roughly $3.4 billion in pre-restructuring debt it disclosed, but it is still a reminder that survival in retail depends on more than a headline-grabbing deal. If suppliers do not trust the business, product flow slows. If product flow slows, shelves go empty. If shelves go empty, the turnaround story starts to unravel.

How Saks got here

Saks Global was formed in late 2024 in a $2.7 billion combination of Saks Fifth Avenue and Neiman Marcus Group, a deal meant to create a stronger luxury player. Instead, the first year turned into a stress test almost immediately. The company said its disclosure statement was approved on May 1, 2026, clearing the way to solicit votes on the plan and move toward confirmation and emergence this summer.

The reorganization plan is blunt about who gets protected and who gets pushed out. It would hand control to senior lenders and wipe out existing equity. Saks Global says the plan is backed by $1 billion in new financing during bankruptcy and an additional $500 million commitment upon exit, along with a $20 million litigation trust for junior creditors. The company is also forecasting roughly 7% annual revenue growth from fiscal 2027 to 2030 and a return to profitability by fiscal 2029, but that future depends on the operation functioning cleanly after a messy reset.

That is the core lesson for any retailer trying to talk its way through a turnaround. Financing is not a back-office detail. It determines whether vendors ship on time, whether inventory arrives in the right mix, and whether leadership can keep promising a stable plan without running into the same cash crunch again.

What Big Lots employees should watch on the floor

For Big Lots workers, the practical signal is simple: watch the product, not the talking points. When a retailer is healthy, replenishment feels steady, assortments make sense, and vendors continue shipping without drama. When financing gets tight, the warning signs usually show up first in the store, not in the earnings deck.

The most telling signals are often operational:

- Shrinking variety in core categories

- Repeated stockouts in high-traffic departments

- Slower replenishment after big sales periods

- More aggressive markdowns to move aging inventory

- Sudden changes in assortment strategy without a clear supply plan

Those shifts can point to stress in the company’s vendor confidence or cash flow. A retailer can announce a reset, a merger benefit, or a brand refresh, but if the shelves do not stay full, the turnaround is already losing ground. Saks Global’s own case shows how quickly that happens when the business is still working through merchandise problems and brand resets while trying to promise a profitable future.

Why Big Lots is the sharper warning

Big Lots already lived through the downside of a retail unwind. The company and its subsidiaries filed for Chapter 11 on September 9, 2024, in the U.S. Bankruptcy Court for the District of Delaware after warning of substantial doubt about its ability to continue. At filing, it operated more than 1,300 stores across 48 states, reported about $4.7 billion in fiscal 2023 revenue, and had more than 27,000 employees.

The first sale process was supposed to transfer substantially all assets to an affiliate of Nexus Capital Management, but that effort fell apart. Going-out-of-business sales followed, and later Gordon Brothers Retail Partners completed a going-concern purchase on January 3, 2025. Variety Wholesalers, Inc. was set to operate some stores, and Gordon Brothers said the deal preserved hundreds of stores and prevented thousands of layoffs.

Even that outcome, though better than a total shutdown, shows how quickly the ground can shift when a turnaround loses financing support and the sale process breaks. Big Lots eventually saw its Chapter 11 cases converted to Chapter 7 effective November 10, 2025, a stark ending that underscored the difference between a temporary rescue and a durable operating plan.

The anatomy of a retail turnaround

Saks Global and Big Lots sit in very different parts of retail, but the mechanics are the same. A turnaround works when there is enough cash to keep inventory moving, enough vendor confidence to maintain supply, and enough leadership discipline to avoid promising a recovery the business cannot fund. When one of those pieces slips, the whole structure gets fragile fast.

That is why the Saks Global filing matters to Big Lots workers and managers alike. A company can claim it is on the road to profitability, but if debt is still heavy, product flow is shaky, or vendors begin to doubt payment, the store-level consequences show up almost immediately. Empty shelves, shifting assortments, erratic allocations, and forced markdowns are not just merchandising issues. They are signs that the turnaround is losing its grip.

For Big Lots, the lesson is not about luxury retail drama. It is about recognizing the operational signals that separate a real recovery from a temporary reprieve. When financing is strong enough, the product arrives, the floor stays stocked, and the plan has room to work. When it is not, the turnaround can unravel long before the company says so.

Know something we missed? Have a correction or additional information?

Submit a Tip