Costco’s high ROIC delivers returns rivaling Brown-Forman despite slower earnings growth

Costco's warehouse discipline is driving shareholder returns that can match Brown-Forman's, even as the two companies grow earnings in very different ways.

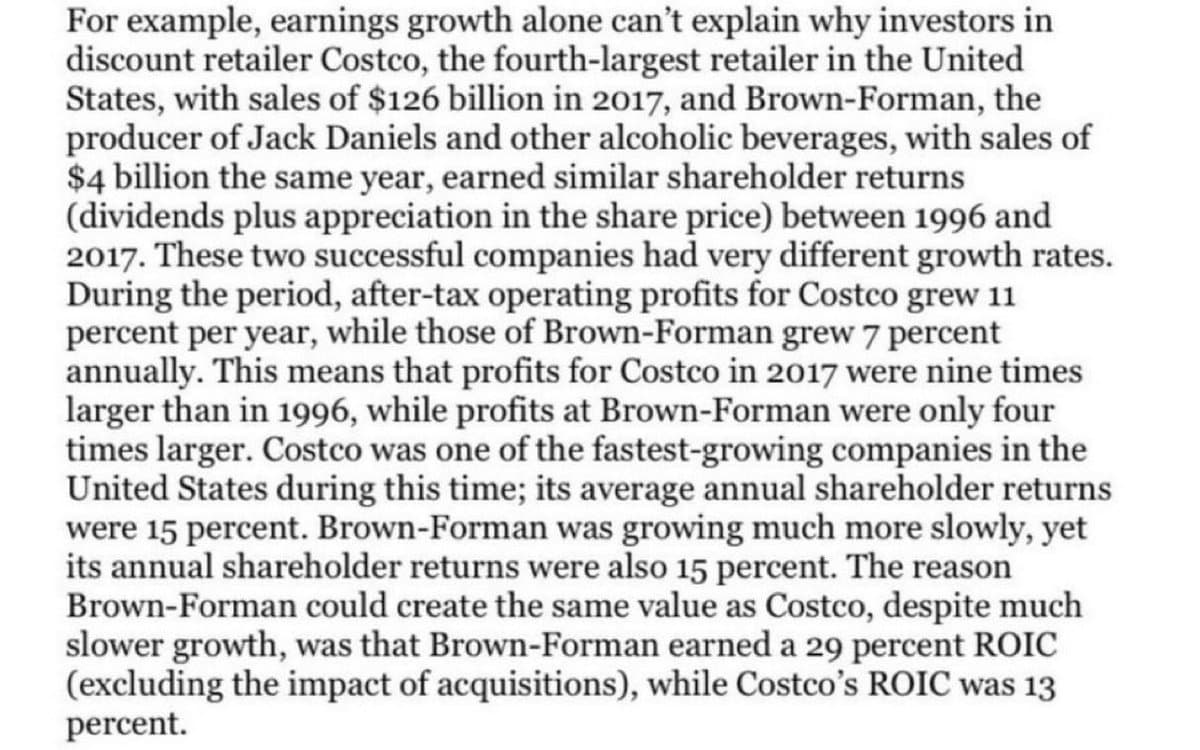

Costco’s warehouse model keeps turning into shareholder cash because it is built to move inventory fast, collect memberships reliably, and put capital to work with unusual discipline. That is why the chain’s returns can look comparable to Brown-Forman’s even when the earnings path is very different, and why the story matters to the people inside the warehouses who make the system run.

Why return on capital matters on the floor

Return on invested capital is not just a boardroom metric at Costco. In a business built on high volume and rapid inventory turnover, the way pallets move, trucks unload, and members keep renewing feeds directly into how efficiently the company uses every dollar of capital. Costco Investor Relations says the model is centered on low prices, a limited selection, high sales volume, and rapid inventory turnover, supported by membership fees, efficient distribution, and reduced costs.

For warehouse workers, that means the operating culture is built around speed, consistency, and low waste. Every stocked endcap, every clean receiving cycle, and every accurate replenishment helps the company squeeze more output from the same footprint, which is the kind of discipline that supports high ROIC over time.

Costco’s fiscal 2025 numbers show the machine still compounding

Costco Wholesale Corporation closed fiscal 2025 on August 31, 2025, with net sales of $269.9 billion, up 8.1% from the prior year. Net income rose to $8.099 billion, or $18.21 per diluted share, while comparable sales for the full year increased 5.9% reported and 7.6% adjusted. E-commerce sales climbed even faster, up 15.6% reported and 16.1% adjusted.

The footprint behind those results is large and still expanding. Costco said it operated 914 warehouses at fiscal year-end, including 629 in the U.S. and Puerto Rico. Membership remains a core advantage, with renewal rates of 92.3% in the U.S. and Canada and 89.8% worldwide, numbers that matter because recurring membership revenue gives the company a steadier base than a typical retailer.

For workers, those figures point to a business with durable traffic and repeat demand. A warehouse that keeps members coming back does not just help the balance sheet. It also supports a steady flow of replenishment, which shapes schedules, receiving work, merchandising pressure, and the daily pace on the floor.

Why Brown-Forman is the useful contrast

Brown-Forman offers the other side of the comparison. Its fiscal 2025 ended on April 30, 2025, and its fourth quarter showed net sales down 7% to $894 million. The company said operating income fell 45% and diluted earnings per share fell 45%, a drop tied to persistent weakness in the U.S. spirits market.

That contrast matters because it shows how differently shareholder returns can be created. Brown-Forman’s business is more exposed to shifting consumer demand and product mix pressure, while Costco’s model leans on recurring memberships, fast turns, and an operating system that keeps capital moving. The result is that investors can end up rewarding capital efficiency and compounding economics, not just faster earnings growth.

Dividends tell a second story about capital allocation

Costco’s dividend history shows a company that has favored a steady payout policy but has also used special dividends when it had room to return more cash. One of the clearest examples is the $15 special dividend paid in January 2024, which stands out as a sign of confidence in the company’s cash generation and balance-sheet discipline.

Brown-Forman takes a more regular quarterly approach. Its dividend history shows total dividends paid in 2025 of $0.9105 per Class A share. That difference in style helps explain how two companies can deliver very different capital-return profiles and still produce comparable shareholder outcomes over time.

For Costco employees, the bigger takeaway is not the dividend itself. It is the fact that the company’s operating model generates enough cash to support both reinvestment and return of capital, which is one reason the business can keep leaning into expansion without abandoning its low-price formula.

What the market is rewarding

The market has clearly noticed Costco’s compounding habit. One recent market summary put the company’s five-year total shareholder return at about 192% and its all-time gain at 8,860.75% as of June 23, 2026. Those numbers reflect more than just a strong stock chart. They point to a business that has repeatedly converted operational discipline into financial performance.

That is the deeper lesson for anyone working inside a Costco warehouse. High ROIC is not an abstract Wall Street term when the company’s whole model depends on fast turns, loyal members, efficient distribution, and careful capital allocation. It is the financial result of the same habits that shape everyday work on the floor, and it is why Costco’s returns can rival companies with very different earnings patterns.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?