Dollar General’s spendwell offers workers faster pay and cash access

Spendwell can speed up pay by two days, add cash at Dollar General, and help workers bridge bill gaps, but fees, eligibility, and overdraft rules still matter.

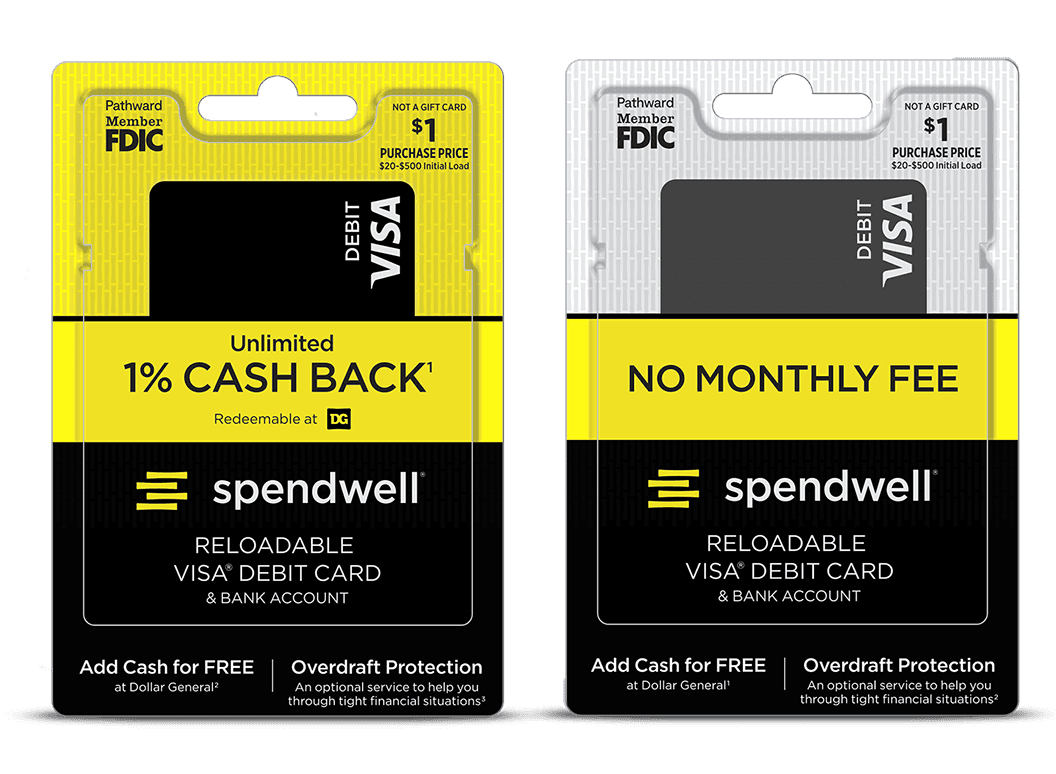

Dollar General’s Spendwell is built for a very specific workplace problem: paychecks that do not always arrive when bills do. The reloadable Visa debit card and bank account can help workers get paid faster, load cash in the store, and keep money moving without leaning on payday lenders or overdraft surprises. That makes it more than a perk. For employees living paycheck to paycheck, it is a cash-flow tool.

Why this matters on the store floor

The appeal starts with timing. Retail workers often juggle rent, gas, childcare, medicine, and repair bills on schedules that do not care when payroll lands. Spendwell’s pitch is simple: make the money easier to reach, easier to split, and easier to use before a late fee or a bounced payment turns into a larger problem.

That pressure is not abstract. The FDIC says 4.2% of U.S. households, about 5.6 million households, were unbanked in 2023. Its most recent household survey was conducted in June 2023 and collected responses from almost 30,000 households, part of a biennial survey the agency has run since 2009. In plain terms, there is a real slice of the workforce that either cannot rely on a traditional bank relationship or does not want to.

What Spendwell actually offers

Dollar General says Spendwell is a reloadable Visa debit card and bank account established by Pathward, N.A., Member FDIC. The company says funds are FDIC-insured subject to applicable limitations and restrictions, which matters because workers need to know what protection they actually have and where the fine print begins.

The practical features are the ones that fit day-to-day life in a discount retail job. Cash can be added at any Dollar General store through Barcode Reload from the mobile app, which gives employees and customers a way to put money onto the account without a separate bank branch trip. Early direct deposit can arrive up to two days sooner, a feature that can help when a bill is due before the normal payday. The account also includes online bill pay, 24/7 customer service, subaccounts, and the ability to send money to other Spendwell accountholders.

Just as important, Dollar General says there is a no monthly fee option. That does not mean the account is free of costs. The company says different account types exist and some features carry charges, so workers need to read the fee structure before assuming a low-friction banking fix. Optional overdraft protection is available only to eligible accountholders, which is useful in theory but not a blanket safety net.

Where it helps, and where it can fall short

For a worker trying to keep the lights on, Spendwell’s best use case is cash-flow control, not financial transformation. Early direct deposit can reduce the gap between earning money and accessing it. Subaccounts can help separate gas money from grocery money or a utility payment from everyday spending. Barcode Reload can also be useful for employees who still deal in cash or who want a simple way to move money into an account while at work.

The upside is real, but so are the limits. Optional overdraft protection can soften a mistake, but it is still a feature tied to eligibility, not a guarantee against shortfalls. The no monthly fee option may help workers avoid the drag of account maintenance charges, yet fees can still appear elsewhere in the product. That is why this kind of tool should be judged on whether it meaningfully improves the timing of money, not just whether it sounds employee-friendly.

For workers trying to avoid payday loans, the value is in the bridge. Earned wage access and related payroll tools exist because income and expenses do not line up neatly. The Consumer Financial Protection Bureau has said that this mismatch is the reason such tools exist. Kansas City Fed researchers have said earned wage access grew in popularity during the COVID-19 pandemic and high inflation, while also warning that fees, costs, and reliance remain concerns.

How Spendwell fits Dollar General’s broader pay-access push

Spendwell is not the only financial-services tool Dollar General is putting in front of workers. The company’s careers page also promotes Legion Instant Pay and Money Network, including language about access to a portion of pay after each shift. That tells you something about the way the company is thinking about retention and payroll: not just wages, but access to wages.

Dollar General first announced Spendwell in March 2022 as part of a broader enhanced financial-services rollout. That rollout also included a buy-now, pay-later test with Sezzle and card reward payment options. Taken together, the effort looks less like a standalone banking side project and more like an attempt to wrap payroll, spending, and short-term cash access into the same employee ecosystem.

The fine print workers should not skip

A product like this can help, but only if workers know what they are signing up for. The account’s different versions matter, the fee schedule matters, and the eligibility rules for overdraft protection matter. The fact that funds are FDIC-insured is meaningful, but only within the limitations and restrictions that apply to the account.

Dollar General is also running a limited $20 statement-credit offer for qualifying new accounts opened or starter cards purchased between April 1, 2026 and June 30, 2026. That kind of incentive can make enrollment easier, but it should not be the reason to choose an account. The real question is whether the card and account help smooth the week-to-week crunch that comes with retail pay.

What that says about work at Dollar General

The company’s own employee materials say it is committed to employee growth through training, internal promotion, tuition reimbursement, and financial support when disaster strikes. Its employee assistance foundation says it can help regular full- and part-time workers facing hardships beyond their control. That is an admission, however indirect, that a lot of workers need more than a paycheck to stay stable.

Spendwell fits that reality. It will not replace a raise, and it will not fix thin staffing or low wages. But for workers trying to keep cash moving between shifts, bills, and emergencies, it can be a practical buffer, especially if the fees stay low and the access works the way the company says it does.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?