Fed holds rates steady as Goldman Sachs braces for higher borrowing costs

The Fed left rates unchanged, but its projections pointed to a tougher path ahead, sending Treasury yields higher and forcing Goldman desks to price in more borrowing pain.

Goldman Sachs traders and bankers got a hawkish hold, not a neutral pause. The Federal Reserve left its benchmark rate unchanged on June 17, but its updated projections pointed to higher borrowing costs later this year, a signal that mattered more for rates, credit and financing teams than the headline decision itself.

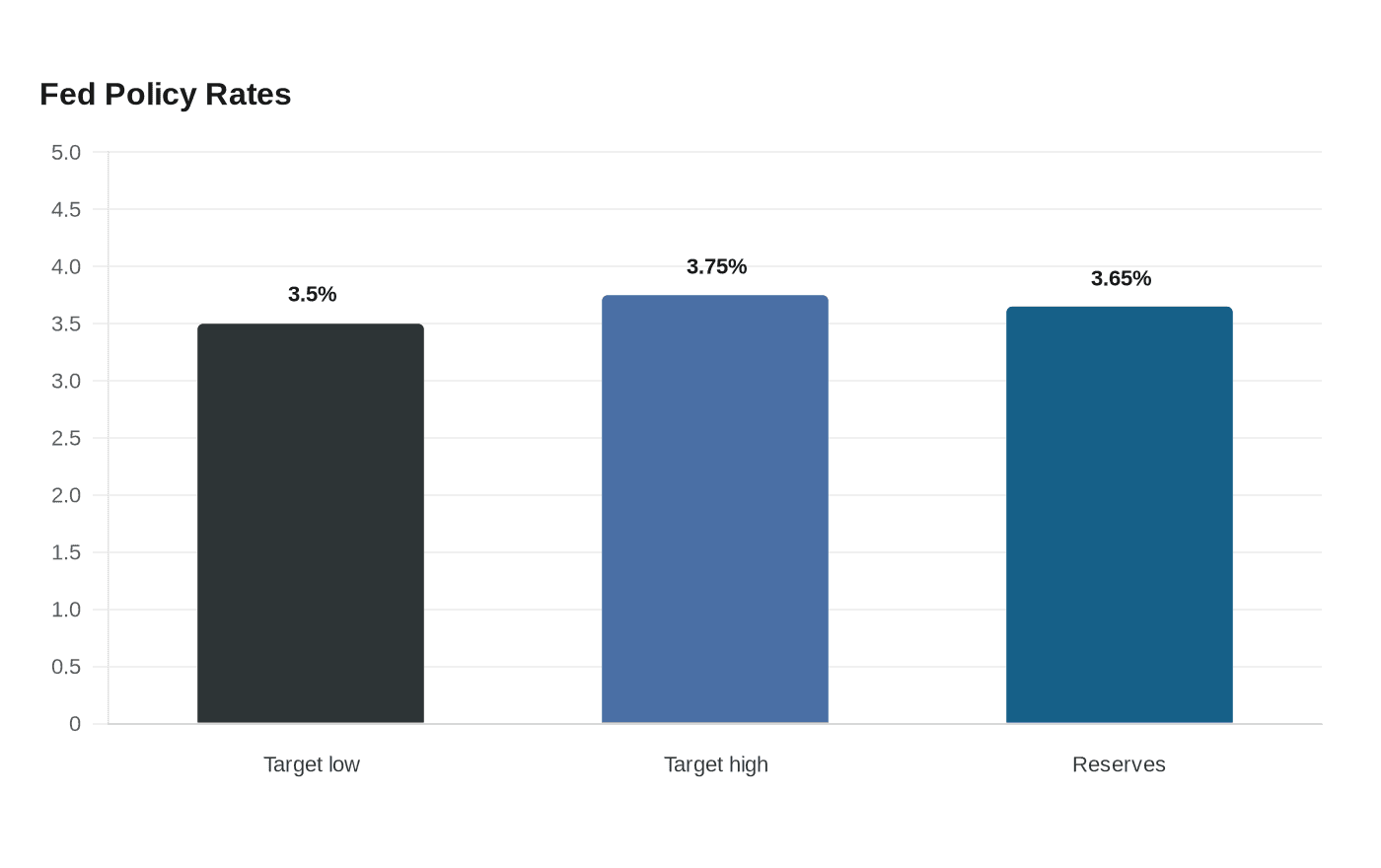

The Federal Open Market Committee voted 12-0 to keep the federal funds target range at 3.50% to 3.75%, and the Board of Governors unanimously held the interest rate paid on reserve balances at 3.65%, effective June 18. But the Fed’s Summary of Economic Projections, covering 2026, 2027, 2028 and the longer run, showed policymakers leaning toward a tighter path ahead, with nearly half seeing the possibility of a rate hike in 2026.

Markets took that as a warning. The 2-year Treasury note climbed to its highest level in more than a year, the 2-year yield rose nearly 11 basis points to 4.153%, and the 10-year yield added 4 basis points to 4.469%. Stocks faded as well, with the S&P 500 down 0.6%, the Nasdaq Composite off 0.7% and the Dow Jones Industrial Average lower by 160 points.

For Goldman employees, the message lands quickly in day-to-day work. A hold does not feel benign if the market reads the forward path as more restrictive. That shifts the math on M&A financing, leveraged finance pricing, structured hedging and client conversations around cash, duration and risk. It also changes the tone inside equity syndicate, rates and credit, where a stronger-for-longer backdrop can tighten conditions before the Fed actually moves again.

Goldman had already moved in that direction. On June 8, the bank pushed out its rate-cut forecast, saying it expected the Fed to leave rates unchanged through 2026 and delay cuts until 2027, citing stronger economic activity and job growth after a robust payrolls report. The June 17 decision and projections reinforced that call, rather than challenging it.

That is the real story for the firm’s analysts, associates and managing directors: the cost of capital is still doing the work of restraint, even without a rate move. In a market like this, the people who can translate Fed language into funding pressure, valuation risk and client positioning will have the clearest edge.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?