Fitch turns negative on Goldman Sachs BDC amid credit worries

Fitch's negative outlook puts Goldman Sachs BDC's underwriting, marks and workout culture under a brighter spotlight as non-accruals rise.

Fitch’s negative outlook on Goldman Sachs BDC has turned a routine ratings action into a test of Goldman’s private-credit machine, where deal teams, risk officers and workout staff are now being judged on whether stressed loans are an isolated cleanup job or a deeper underwriting problem.

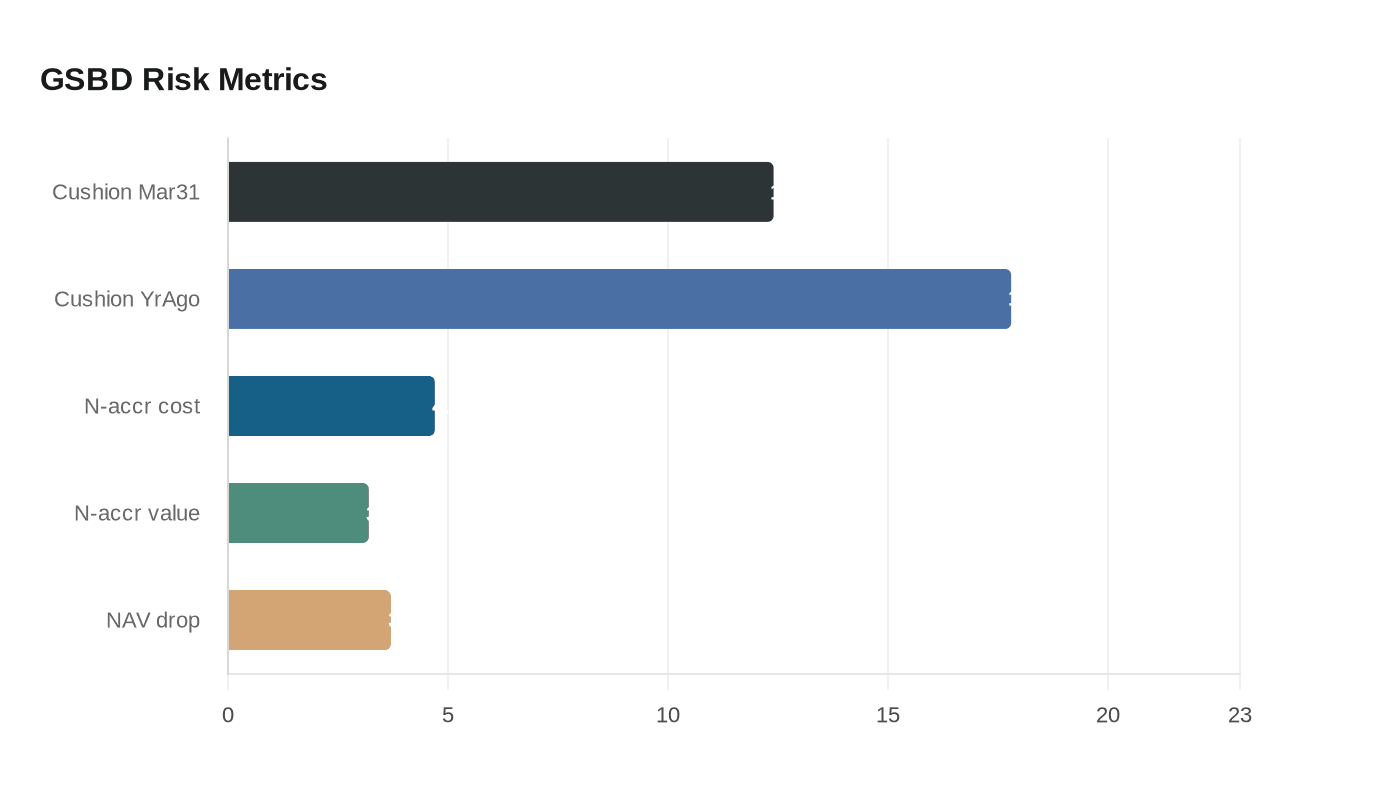

Fitch affirmed Goldman Sachs BDC’s long-term issuer default rating at BBB- and its senior secured debt at BBB on May 15, but shifted the outlook to negative after pointing to higher leverage, elevated non-accruals, realized losses and continued payment-in-kind income. The agency said GSBD’s gross leverage rose to 1.40x at March 31 from 1.33x at year-end 2025, while its asset coverage cushion fell to 12.4% from 17.8% a year earlier. Fitch also said non-accruals reached 4.7% at cost and 3.2% of the debt portfolio at value, with further deterioration potentially leading to a one-notch downgrade.

That matters inside Goldman because private credit careers are built on the promise that credit selection, surveillance and recovery work can stay ahead of stress. When a fund like GSBD shows a thinner cushion, higher leverage and a rising pile of loans not paying cash, the pressure moves from the portfolio to the people whose names are attached to it. It also lands at a moment when underlying borrowers are facing more strain from software and AI disruption, which makes old underwriting assumptions harder to defend.

GSBD’s first-quarter results showed the stress in the numbers. Net investment income per share was $0.22, adjusted net investment income per share was also $0.22, and net asset value fell 3.7% to $12.17 from $12.64 at Dec. 31, 2025. The fund said it had $3.8038 billion of total investments and unfunded commitments across 173 portfolio companies in 40 industries, with 11 companies on non-accrual at March 31. Two first-lien, senior secured positions, One GI LLC and 3SI Security Systems, were placed on non-accrual during the quarter.

Goldman has argued that GSBD is only a small slice of its overall private-credit assets and that the volatility is concentrated in older positions rather than newer originations. The firm said the older loans account for more than 99.5% of total non-accruals at cost, which is a reminder that the current fight is as much about legacy cleanup as it is about fresh underwriting. GSAM’s Private Credit Group is responsible for sourcing, due diligence, structuring, monitoring and servicing the investments, so the pressure runs through every step of the process.

The firm kept moving on capital returns even as the ratings outlook worsened. GSBD announced a second-quarter 2026 base dividend of $0.32 per share on May 7, and its board approved a new 10b5-1 repurchase program authorizing up to $75 million on May 6. Goldman Sachs itself kept its A rating and positive outlook unchanged, but GSBD’s warning is a public reminder that private credit is being watched far more closely now, and that the consequences of stress can travel straight into bonus pools, promotion tracks and the credibility of the franchise.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?