Goldman employees eye 2026 401(k) limits as IRS raises caps

Goldman bankers who max out savings early, or split pay across employers, now have a bigger 401(k) decision to make: the 2026 cap is $24,500, with higher catch-up room for some older workers.

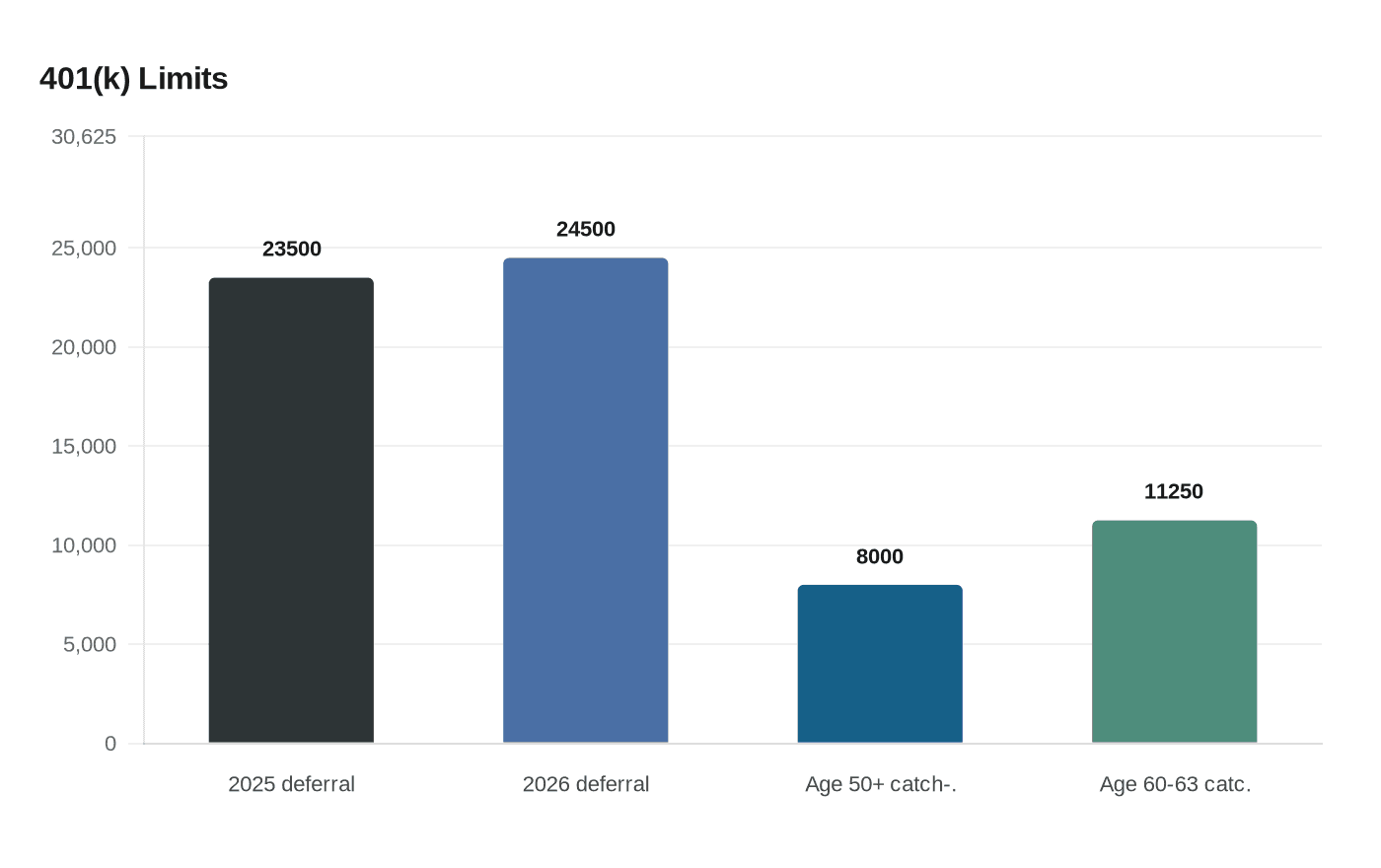

A strong year at Goldman can make the 401(k) ceiling feel less like a retirement footnote and more like a live compensation decision. For 2026, the Internal Revenue Service raised the elective deferral limit for traditional and safe harbor 401(k) plans to $24,500, up from $23,500, giving employees one more lever to shift bonus season pay into tax-advantaged savings.

That matters in a pay mix where Goldman Sachs says compensation may include salary, discretionary compensation and certain local allowances. The firm reported 2025 net revenues of $58.3 billion and earnings per share of $51.32, a reminder that even small changes in deferral timing can affect real money for analysts, associates, vice presidents and managing directors who are trying to balance current cash with long-term wealth.

The IRS also lifted the catch-up contribution limit to $8,000 for workers age 50 and older in 2026, which means many employees can shelter up to $32,500 a year if their plan allows the maximum. For people age 60, 61, 62 or 63, the limit is even higher: $11,250. That creates a narrow but meaningful window for senior Goldman employees who want to accelerate retirement savings while compensation is still at its peak.

The practical wrinkle is that the headline number is not always the number on the plan screen. The IRS says employees should aggregate elective deferrals across plans, which matters for anyone who changes jobs during the year or has multiple sources of compensation. It also says highly compensated employees, managers or owners may face deferral limits because of nondiscrimination testing. In other words, Goldman employees cannot assume the federal cap is the only ceiling that matters; the employer plan itself can constrain how much gets saved.

Goldman says on its careers benefits page that it provides financial wellness and retirement resources, and its Ayco business offers financial planning and wealth management for executives, employees and individuals. That makes the 401(k) cap more than a generic benefit line item. For people who are already thinking about deferred compensation, bonus timing and exit opportunities, the decision to front-load contributions or preserve room for catch-up dollars can change the after-tax value of a year’s pay.

The IRS announced the 2026 limits in November 2025 in Notice 2025-67, and the rules serve as a blunt reminder that retirement saving has a calendar. For Goldman employees, missing the cap is one of the few ways to leave tax-advantaged money on the table.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?