Goldman lifts Nvidia forecasts as AI demand drives outlook higher

Goldman’s bigger Nvidia call puts more pressure and prestige on the bank’s AI coverage teams, from research to tech banking to sales.

Goldman Sachs’ higher Nvidia numbers do more than lift a price target. They push more status, more client demand and more internal leverage toward the people inside Goldman who cover semiconductors, cloud spending and the AI trade, especially equity research, tech banking and the sales staff trying to keep clients in the name. James Schneider reiterated a Buy rating and a $250 price target on May 7, while Goldman’s updated CY2026 and CY2027 earnings estimates sat 14% and 34% above Street consensus.

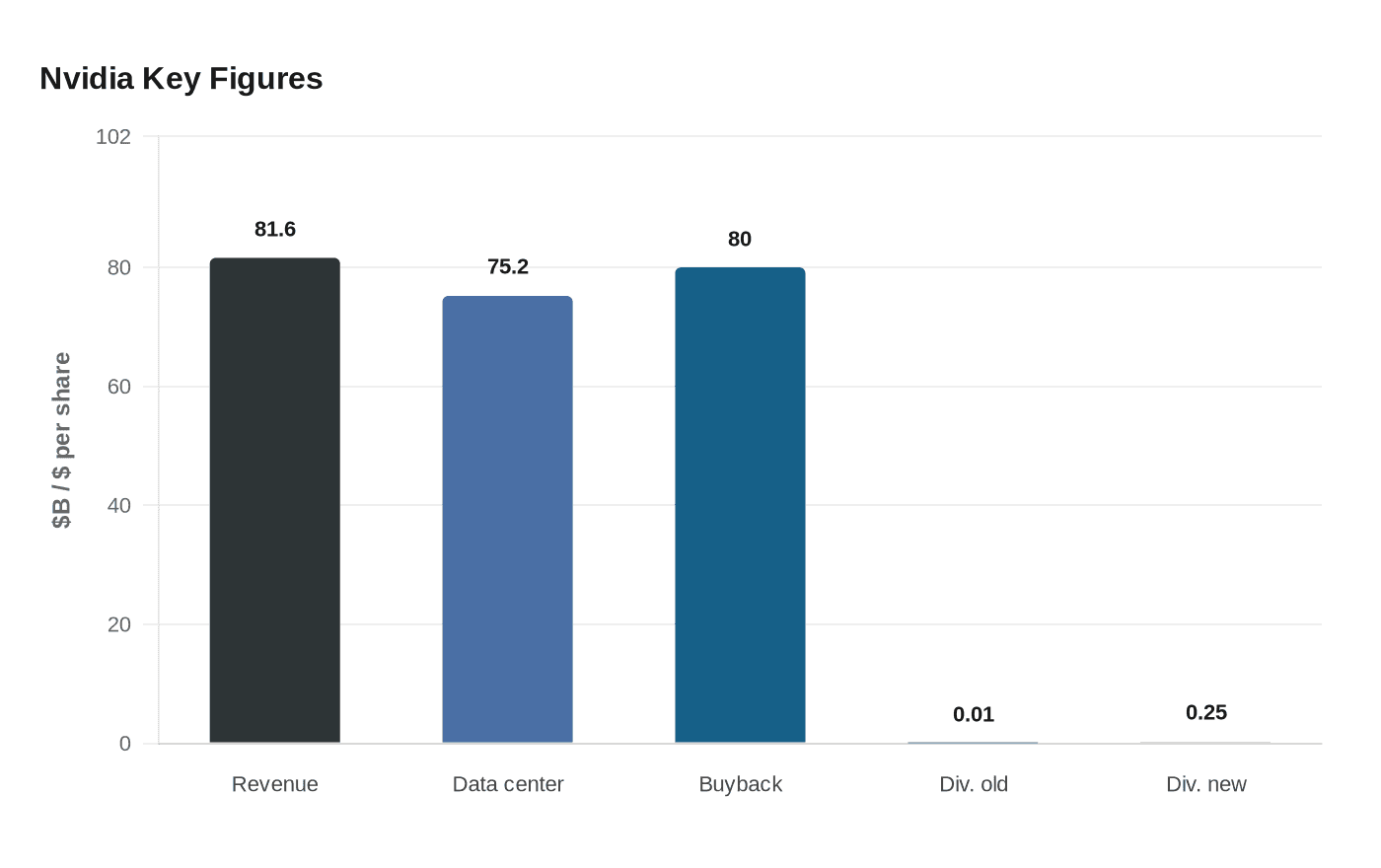

That view looked even more aggressive after Nvidia reported record first-quarter fiscal 2027 revenue of $81.6 billion on May 20, up 85% from a year earlier. Data-center revenue hit $75.2 billion, up 92%, while the company authorized another $80 billion in share repurchases and lifted its quarterly dividend from $0.01 to $0.25 a share. On the call, Jensen Huang said demand had “gone parabolic” and tied the surge to agentic AI, adding that Nvidia was the only platform running every frontier AI model, including work from Anthropic, OpenAI, SpaceXAI, Meta and Google’s Gemini.

For Goldman, the question was not whether Nvidia was still beating estimates. It was how far the runway extended. The bank said Nvidia’s $1 trillion cumulative AI revenue roadmap, which covers Blackwell, Blackwell Ultra and Rubin through calendar 2027, may be conservative because it leaves out Rubin Ultra, Vera CPU racks and inference configurations. Goldman also pointed to stronger supply-chain signals from Taiwan Semiconductor Manufacturing Co. Ltd. and SK hynix, plus higher 2026 capex plans from U.S. hyperscalers, as support for a continued bullish case.

There is a workplace read-through here that matters inside Goldman. When one stock keeps driving the AI narrative, the teams closest to it tend to get the most visibility. Equity research has to keep refreshing the model, defending the call and explaining why the trade still has room. Tech bankers and semiconductor specialists get more chances to pitch financing, coverage and M&A around the same theme. Sales and trading staff, meanwhile, have to keep persuading clients that the surge is not already crowded. In a firm where promotion paths, client access and bonus outcomes are shaped by who is closest to the action, Nvidia’s momentum is becoming more than a market story. It is a workload story.

Know something we missed? Have a correction or additional information?

Submit a Tip