Goldman links Fed outlook and megacap tech earnings to AI trade

Goldman is telling clients to watch two gauges at once: whether megacap AI earnings keep lifting markets and whether the Fed keeps rates high enough to dent the trade.

Goldman’s AI trade playbook now runs through the Fed

Goldman Sachs is pitching a simple but consequential read on the market: AI optimism still has power, but higher-for-longer rates can blunt it fast. The firm’s May 1 podcast, “Riding the AI Wave: Megacap Tech and the Fed,” links a divisive FOMC meeting with the earnings power of the biggest technology companies, turning two of the most common client questions into one conversation.

That framing matters because the market is increasingly concentrated in a handful of names. Goldman says the seven biggest tech companies now make up more than 30% of the S&P 500’s market capitalization and roughly one quarter of the index’s earnings. When those companies report strong numbers, they can keep the AI trade alive even if the rest of the market is less convincing.

Why Goldman is bundling rates and AI into one client discussion

The podcast features Anshul Sehgal, Goldman Sachs Global Banking & Markets’ global co-head of Fixed Income, Currency and Commodities, in conversation with Chris Hussey. Goldman is not presenting the Fed as an isolated macro story or megacap earnings as a standalone equity story. It is treating them as one trade, one that cuts across rates, stocks, derivatives, and financing.

For people inside Goldman, that combination is practical. A less hawkish or more patient Fed can support duration-sensitive assets, while strong megacap earnings can keep momentum behind AI-related positioning. Put together, those forces shape how clients think about portfolio concentration, hedging, and where to place risk when the tape is being driven by a few huge balance sheets and a still-uncertain policy path.

The AI build-out is no longer a theme, it is a capex cycle

Goldman’s same-day AI research gives the podcast more weight. The firm says baseline aggregate AI capex estimates are about $7.6 trillion between 2026 and 2031 across compute, data centers, and power. It also says the largest hyperscale cloud computing companies are expected to spend more than half a trillion dollars on capital expenditures in 2026 alone.

That scale helps explain why Goldman is so focused on earnings delivery from the megacaps. AI is not being treated as a vague narrative or a conference-room buzzword. It is being framed as a multiyear infrastructure build-out with real consequences for power demand, data-center spending, vendor selection, financing needs, and the companies that can fund the race from operating cash flow.

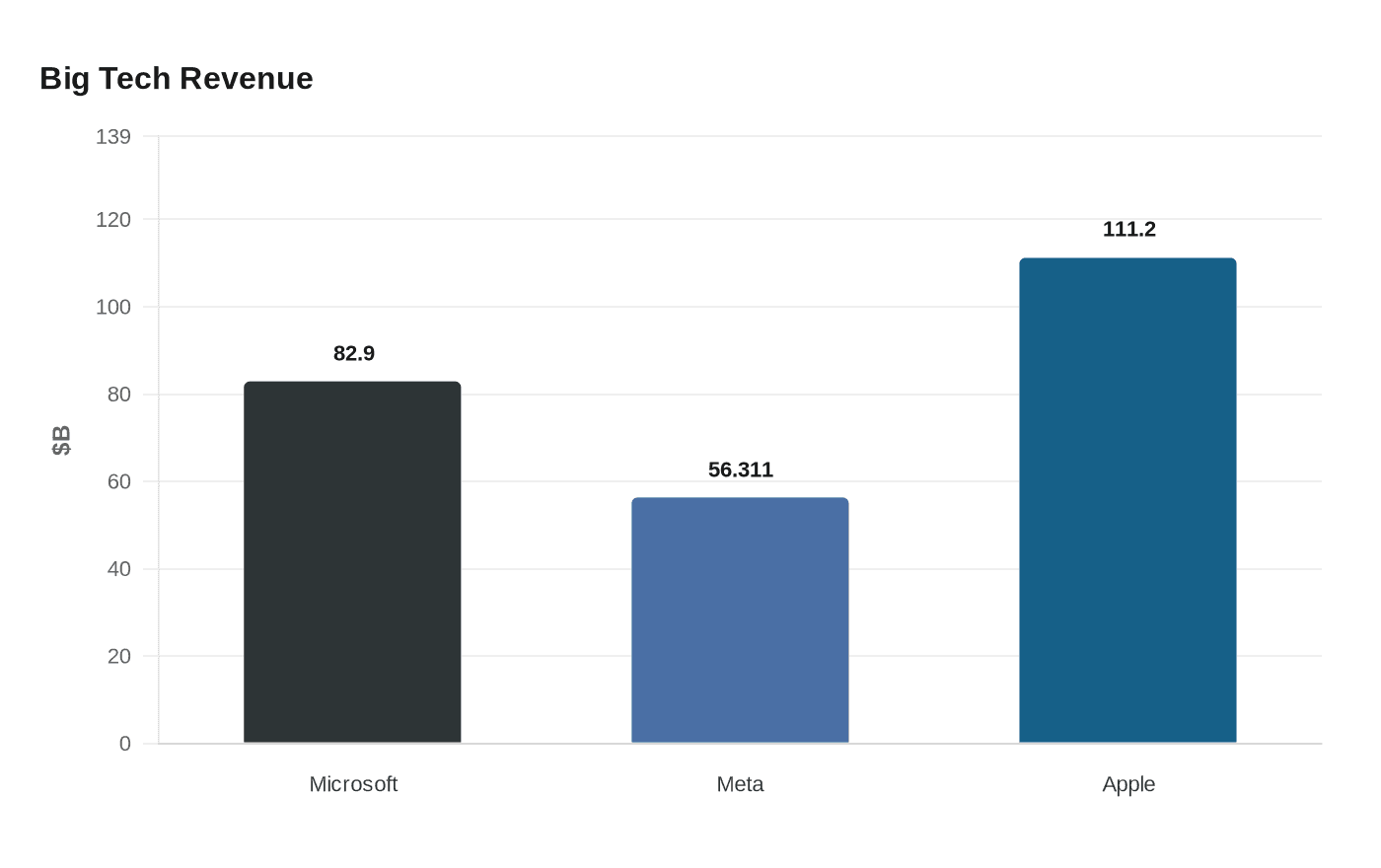

The earnings prints backing up the story

The timing of the podcast matters because it landed alongside fresh results from the very companies driving the trade. Microsoft reported April 29 revenue of $82.9 billion, up 18%, and said its AI business surpassed an annual revenue run rate of $37 billion, up 123% from a year earlier. That is the kind of number that keeps clients engaged, because it shows AI revenue is starting to show up in hard financials, not just in product demos or capex plans.

Meta added to the evidence on April 29, reporting revenue of $56.311 billion and capital expenditures of $19.84 billion. Mark Zuckerberg called it a “milestone quarter,” and the company said it released its first model from Meta Superintelligence Labs. Apple followed on April 30 with quarterly revenue of $111.2 billion and an additional $100 billion share-repurchase authorization, another sign that mega-cap balance-sheet strength still gives these companies room to support investors even as they invest heavily.

Alphabet also announced first-quarter 2026 results on April 29, reinforcing the same point: the biggest technology companies are not just beneficiaries of the AI trade, they are the engine behind it. For Goldman clients, that means earnings season is functioning as a referendum on whether AI can keep carrying index-level performance.

The Fed is the other half of the trade

Goldman is pairing that earnings momentum with a policy question that is still unsettled. The Federal Reserve’s April 28-29, 2026 FOMC meeting ended with a statement, and the minutes are scheduled for release on May 20, 2026. Goldman’s podcast note centers on what that divisive meeting could mean for policy from here, which is a direct way of saying the next move is not cleanly priced.

That matters because a stubborn Fed can work against the most crowded parts of the AI trade. If rates stay elevated, duration-sensitive assets and richly valued growth names can lose some of their support. If policy turns more patient, the market gets a better backdrop for the kind of long-duration earnings growth investors have been rewarding in the megacaps.

How this lands inside Goldman’s own client conversations

For analysts, associates, VPs, and managing directors, this is the sort of market setup that spills into daily work quickly. It changes what goes into morning prep, how coverage teams frame client calls, and how traders think about positioning across rates and equities. It also affects the tone of internal discussions, because one macro headline can now move everything from equity indices to hedge ratios to financing demand for AI infrastructure.

The significance goes beyond one podcast. Goldman’s 2026 S&P 500 outlook, updated as of April 24, calls for the index to rise 6% to a year-end target of 7,600, built on 12% earnings-per-share growth in 2026. The firm also says AI investment should keep rising this year even as capex growth slows. That gives employees a clear internal script: clients are being asked to believe in earnings, capex discipline, and policy patience at the same time.

Why Sehgal is becoming a recurring voice on the macro tape

This is also part of a pattern. In a January 29 podcast, Sehgal and Hussey discussed whether investors needed a new barbell strategy, and Goldman has used Sehgal repeatedly in conversations about portfolio structure and market positioning. That makes him a familiar voice for clients who want a rates-and-credit view that reaches beyond a single headline.

For Goldman, the value of that format is obvious. A single conversation can bridge the firm’s markets franchise, its AI research, and the questions clients keep asking about concentration risk and policy. For employees, it is a reminder that the AI trade is no longer just a technology story. It is now a market structure story, a rates story, and a test of whether the biggest companies can keep delivering fast enough to justify the index being carried by so few names.

The message from Goldman is straightforward: if megacap earnings keep validating AI spending and the Fed does not tighten the screws further, the trade can keep running. If either leg weakens, the market’s most important narrative gets harder to defend.

Know something we missed? Have a correction or additional information?

Submit a Tip