Goldman Sachs cuts US recession odds as growth outlook holds up

Goldman’s lower recession call points to steadier deal flow, a less defensive hiring market and better odds for bankers chasing promotion in a softer-landing year.

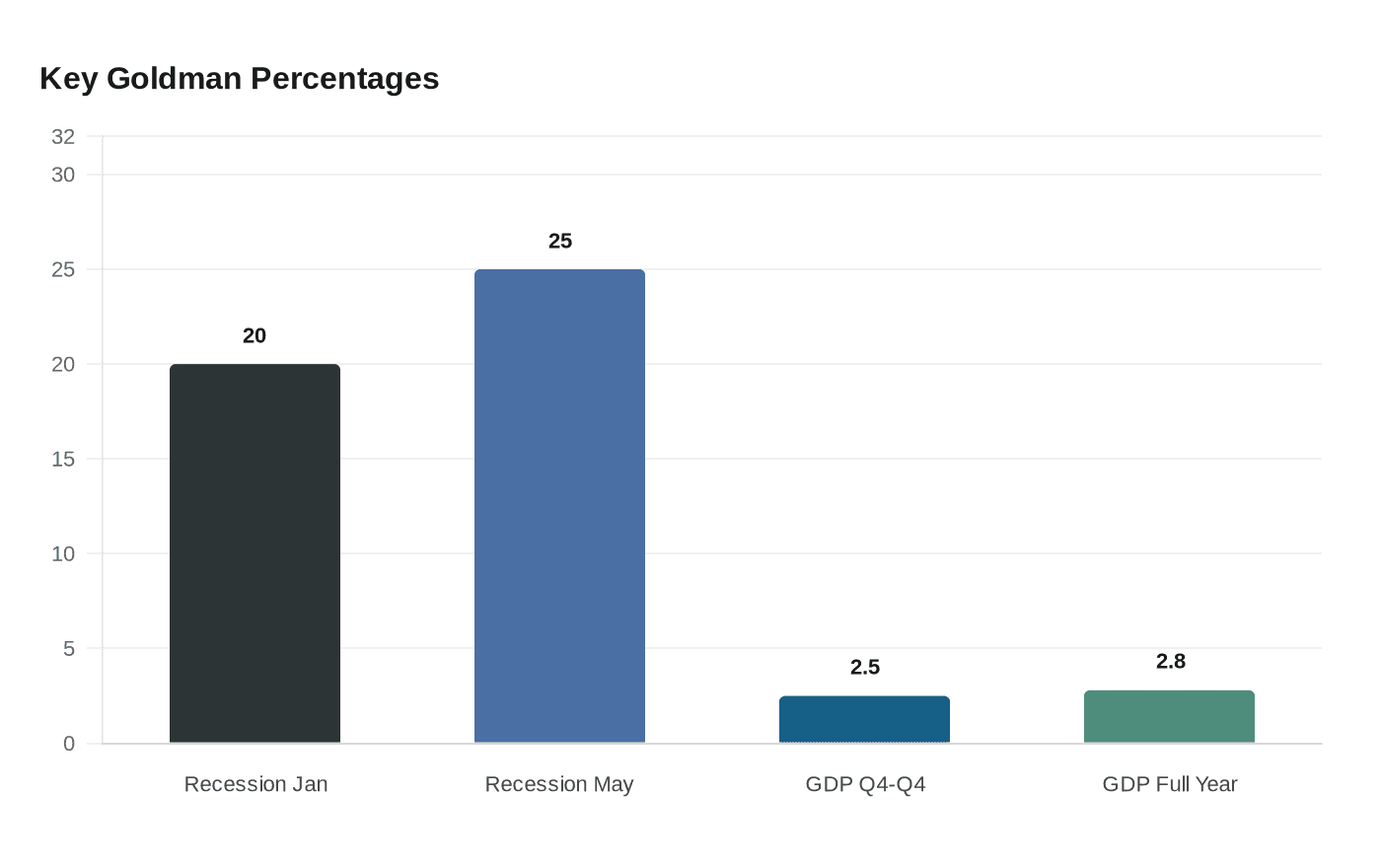

Goldman Sachs is telling its people to plan for a better 2026 than many feared. The firm cut its 12-month US recession probability to 20% in January, then trimmed it again to 25% on May 11 as economic activity held up, payrolls still grew and financial conditions eased back below pre-war levels. For bankers, that matters immediately: a softer landing usually means fewer frozen mandates, less panic staffing and a better shot at keeping client pipelines moving through the summer bonus season.

The shift starts with the numbers Goldman’s economists are now leaning on. In January, Jan Hatzius and David Mericle said US GDP could grow 2.5% on a fourth-quarter-to-fourth-quarter basis, or 2.8% for the full year, with core PCE inflation falling to 2.1% by December. By May, the case for a broad slowdown looked less urgent, even with Iran-related risk hanging over markets. Goldman said private domestic final sales were growing at a 2.5% real annualized rate, April nonfarm payrolls rose by 115,000 and the unemployment rate was 4.3%.

That combination is more reassuring for the desks that live and die by risk appetite. M&A bankers, equity capital markets teams and credit sales people do better when clients believe the economy is still expanding and recession calls are being pushed back, even modestly. A 20% or 25% recession probability is not a victory lap, but it is enough to keep CFOs talking about transactions instead of retreating into balance-sheet defense. It also matters for recruiting: analysts and associates weighing exits will read a firmer growth outlook as a sign that deal flow, not layoffs, is more likely to define the year.

The softer-landing view does not mean every desk is equally well positioned. Goldman’s own consumer research said the conflict in the Middle East was still squeezing households, especially lower-income ones, and it cut forecast growth in discretionary cash inflow to 3.7% from 5.1% at the start of the year. Brent crude was around $100 a barrel in early May, up from $61 at the end of 2025, and Goldman sees it averaging $90 in the fourth quarter. That keeps pressure on consumer, retail and discretionary coverage, even as macro and commodities teams benefit from the volatility.

For employees thinking about comp and promotion, the more important signal is that Goldman is no longer talking like a firm bracing for an abrupt downturn. If growth holds up, the firm can justify a less defensive stance on headcount, preserve more optionality in bonus pools and keep mid-level performers on a clearer path to managing director. The message underneath the forecast revision is simple: recession risk is lower, but the real differentiator inside Goldman will be which desks turn a still-shaky labor market and uneven consumer squeeze into actual revenue.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?