Goldman Sachs explains how investment banking careers fit its core business

Goldman’s careers map shows investment banking is not just deal pitching. It is a full-stack business of advising, financing, operations, and engineering tied to $53.5 billion in revenue.

Investment banking at Goldman is the operating system, not a side business

Goldman Sachs is using its investment banking careers page as something closer to an internal map than a recruiting brochure. The message is plain: the division exists to advise corporations, financial institutions, entrepreneurs, asset managers, and governments on their most important transactions, and to do it as part of a broader firm that still treats Global Banking & Markets as one of its two core franchises. That matters inside the building because the work is not framed as slide-making for its own sake. It is framed as building durable client relationships, executing across the full transaction cycle, and helping Goldman act as a trusted advisor, financier, and risk manager when the stakes are highest.

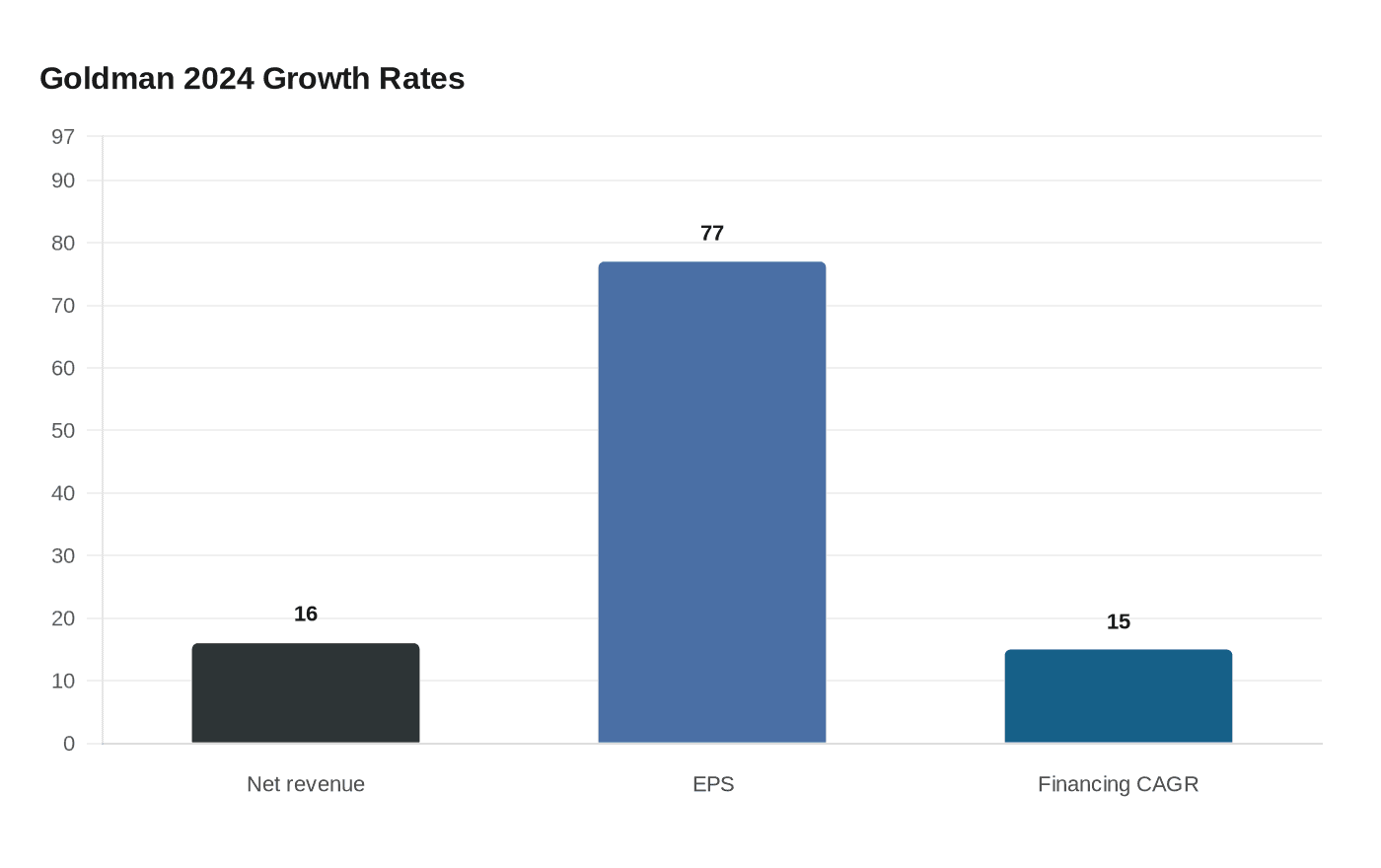

That framing is not abstract. Goldman said in its 2024 annual report that net revenues rose 16% year over year to $53.5 billion, earnings per share climbed 77% to $40.54, and return on equity improved to 12.7%. In other words, the careers page sits inside a business that is still central to how the firm makes money, and Goldman’s own numbers give the page weight. For analysts and associates, the real takeaway is that career progression is tied to whether you can help the franchise move from idea to execution without dropping the thread.

How the division is actually organized

Goldman divides classic investment banking by industry and geography, which is a familiar structure for anyone who has sat through staffing conversations or watched coverage teams split by sector. The point is not just administrative. It is how the firm keeps clients close, builds repetition in a sector, and creates a path for junior bankers to accumulate judgment in a specific market while still learning the broader mechanics of the bank.

The Mergers & Acquisitions Group sits alongside that coverage model and handles the deals that are most visible, most political, and often most fragile. Goldman says the team works on activism and raid defense, sponsor transactions, cross-border M&A, structured M&A, and strategic M&A. It also says the firm has maintained its position as the leading M&A advisor in investment banking and describes M&A as helping business leaders drive transformation and optimize value. For employees, that signals where the pressure and the prestige often concentrate: in the transactions where speed, discretion, and judgment can matter as much as modeling.

The Financing Group is the other half of the execution engine. Goldman says it includes all capital markets departments and works with FICC and Equities. Its capital-solutions platform covers financing, origination, structuring, and risk management, with products spanning equity capital markets, investment-grade debt, fund financing, leveraged finance, structured finance, and real estate finance. The firm also says its business sits at the fulcrum of the convergence of public and private markets, which is a useful way of saying the financing side is increasingly where companies, sponsors, and asset managers go when the old public-market and private-market boundaries blur.

Why financing is more than a support act

The financing franchise is not just there to follow M&A mandates after the fact. Goldman’s 2024 annual report said more durable FICC financing and Equities financing net revenues grew at a 15% compounded annual growth rate since 2019, reaching a record $9.1 billion in 2024. That figure matters because it shows the funding, risk transfer, and market access side of the house is not a minor attachment to advisory work. It is a meaningful profit center in its own right, and one that often determines whether a transaction can get done on acceptable terms.

Goldman’s broader 2024 shareholder letter said GBM is advising clients on transformational strategic transactions, providing access to financing to fund growth and innovation, and helping manage volatility by intermediating risk. Those three verbs, advising, financing, and managing volatility, are the real connective tissue of the business. A junior banker who understands that chain is more valuable than one who only knows how to format a deck. So is an associate who can see when a client’s need has shifted from pure advice to a financing structure that protects timing, certainty, or balance-sheet flexibility.

The hidden leverage sits in operations and engineering

Goldman’s careers materials are unusually direct about the parts of the firm that often stay invisible to outsiders. Operations, the company says, supports every agreed trade, new product launch, new market entry, and completed transaction. Engineering sits at the critical center of the business. That language is important because it tells you where the actual bottlenecks are. A bank can have the best bankers in the world, but if a trade cannot be processed, a market cannot be entered, or a transaction cannot clear internal controls and systems, the client experience breaks down fast.

For workers, that creates a more realistic picture of mobility inside Goldman. Skills travel best when they are tied to execution: product knowledge, risk awareness, process discipline, data fluency, and the ability to work across teams that do not report to the same line manager. The bankers who move well inside the firm are usually the ones who understand how operations keeps the machine moving and how engineering extends what the franchise can do. That is especially true in a business where the firm says it has more than 46,000 people globally and operates in more than 60 cities worldwide. At that scale, the strongest careers often come from learning how to route work across the institution, not from staying inside one narrow desk.

What this means for analysts, associates, and future senior leaders

The careers page is also a clue to how Goldman wants junior talent to mature. A first-year analyst may start in coverage, M&A, or financing, but the broader goal is the same: learn how to connect client strategy, capital structure, market conditions, and internal execution. If you can do that, you become useful across mandates, which is the real currency in a place where staffing and exposure shape advancement.

The page also suggests why Goldman keeps emphasizing interconnected franchises. Global Banking & Markets and Asset & Wealth Management are presented as two world-class, linked businesses, while GBM itself contains investment banking, FICC, and equities. That structure gives the firm more ways to bring a client through the door and more ways to keep that client inside the ecosystem once the first mandate is over. For employees, the upside is obvious: more touchpoints, more routes to exposure, and more chances to build a reputation beyond one transaction. The downside is just as real: more complexity, more coordination, and fewer excuses for not understanding how your work affects the next desk over.

The cleanest reading of Goldman’s message is that investment banking careers are only partly about the bank you see in pitch books. The real business is a chain of advisory, capital formation, risk transfer, operations, and technology, all pointed at the same client problem. At Goldman, that chain is the product, and the people who learn to move through it are the ones most likely to move with it.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?